What You Need to Know

Markets posted a strong first quarter, though it was a rollercoaster ride. The path forward will likely stay turbulent, with bank turmoil likely tightening credit conditions and the Fed still wrestling with inflation. Markets, the economy and investment strategies will be unsettled, making research and sound portfolio design keys to avoid overreacting to minutiae and staying focused on navigating the landscape.

Key Takeaways

- In the second half of 2023, investors will likely face a theme of “resistance,” with equity valuations elevated, earnings facing headwinds and the Fed trying to cool off the job market. By 2024, we think resistance will give way to “normalization.”

- Equity markets have been largely driven by the 10 biggest stocks; looking beyond the biggest equity names has been a sound strategy after prior market peaks. In our view, quality should be a key emphasis, with low-volatility stocks potentially versatile equity exposure for risk-averse investors.

- Bond yields are high, setting up returns that could bolster many investors’ portfolios—high yield is a particularly powerful example. In municipal bonds, higher yields and credit spreads, combined with favorable technical conditions, create an attractive entry point.

For Investors, the Market Theme Is “Resistance”

The second quarter was a strong one for risk assets, following a similar pattern as the first quarter: “known unknowns” were resolved, fueling late rallies. This time, the known unknown was the debt-ceiling crisis—once it was worked out, a strong June pushed the S&P 500 into bull market territory.

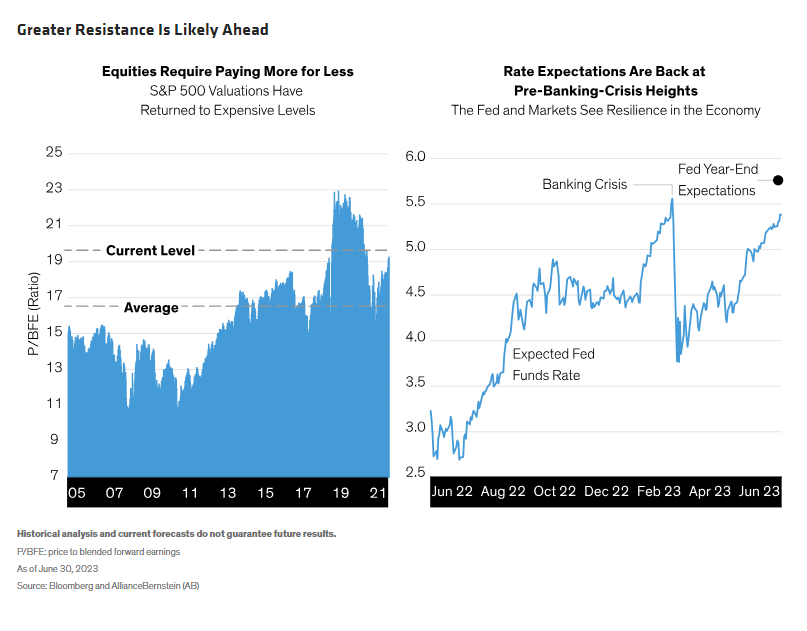

What comes next? As we see it, investors face the second of three themes—resolution, resistance and normalization—through the end of 2023. The resistance stems from S&P 500 valuations that are at the very high end of their historical range (Display, left) and earnings will likely face pressure as economic growth recedes. Inflation should continue to fall but is still well above the Fed’s target.

Then there’s the job market. The Federal Reserve’s primary emphasis has been getting it under control, but it remains very strong. As a result, markets have priced in expectations that interest rates will stay higher for longer (Display, right) and—if anything—that the Fed will likely hike rates one or two more times before they’re finished with this cycle.

How should investors approach this period of resistance?

Looking Beyond the Equity Market’s “Big 10”

We expect equity returns to be somewhat limited moving forward compared with recent experience. Expansion in price-to-earnings multiples has been the biggest market driver since its October 2022 lows, and valuations already price in the positive effect of lower interest rates ahead. With economic growth slowing, corporate earnings will likely face headwinds.

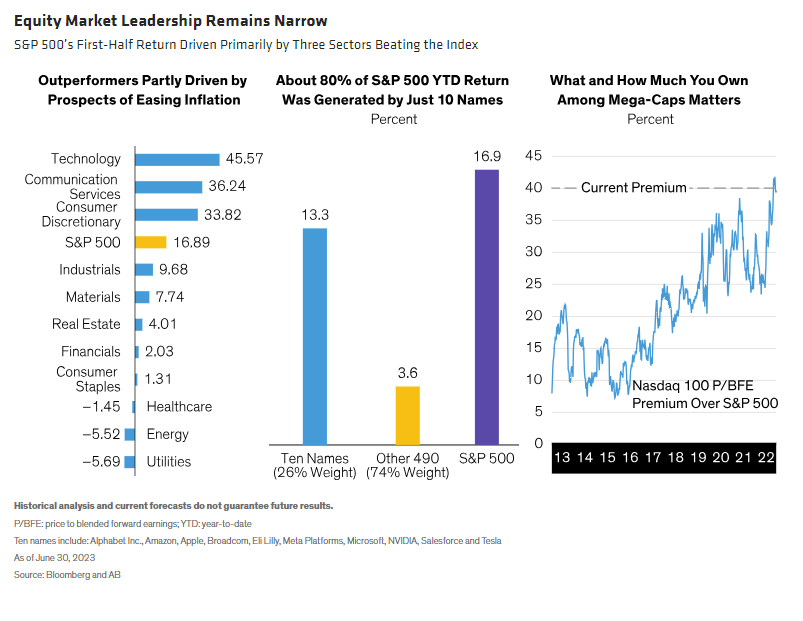

But there are many layers to the equity story. High valuations have largely stemmed from a surge in three sectors (Display, left). Zooming in to the issuer level, 10 of the S&P 500’s biggest stocks have delivered about 80% of 2023 returns through midyear (Display, middle). With broad indices highly concentrated and with many mega-caps expensive (Display, right), it’s worth noting that looking beyond the biggest equity names has been a sound strategy at past market peaks.

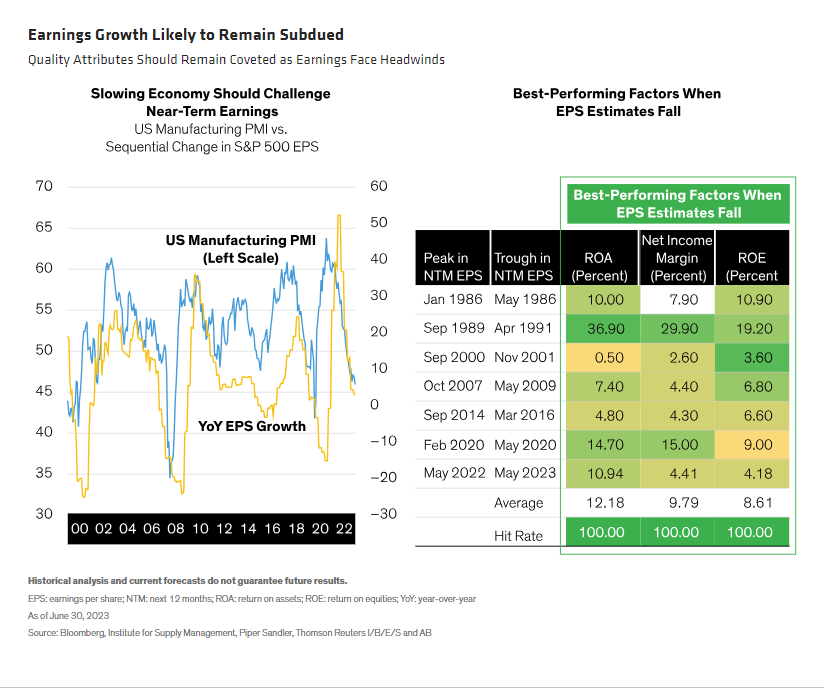

Where should investors look for opportunities? With corporate earnings challenged by a slowing economy (Display, left), quality will be a key attribute to emphasize when selecting equity issuers. In the past, when earnings per share have peaked and then declined, quality factors such as return on assets, net income margin and return on equity have fared best (Display, right).

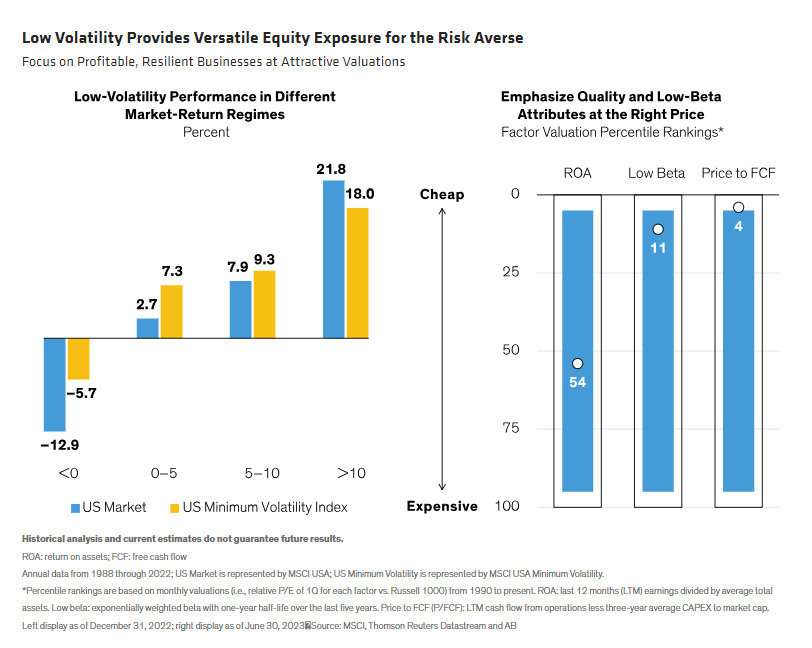

Stocks with high betas to the market have led in 2023, but we don’t think that will last, pointing to low-volatility stocks as versatile equity exposure for risk-averse investors in a subdued return environment (Display, left). Focusing on quality and low-beta attributes at the right price (Display, right) seems sensible. We expect the recovery in small-cap growth equities to continue; despite the strong showing so far, the entry point still seems attractive. An added benefit: good top-line visibility for growth stocks.

The Fixed-Income World: Poised for a Strong Showing

Investors should also look beyond the next handful of months and ready themselves for the market’s coming third theme: normalization. As we move into 2024, growth and inflation will likely revert to their historical experiences, and central bank chatter about rate cuts will follow. This will likely push bond yields down and could leave fixed income as the star of the show.

For starters, bond yields are high—everything from the 10-year Treasury all the way to high yield, bolstering the return potential of many portfolios. However, if the macro environment unfolds as we expect over the coming 12–18 months, those expected returns will very likely be front-loaded, not spread out over the years ahead. So this leaves a strong opportunity, but it won’t wait.

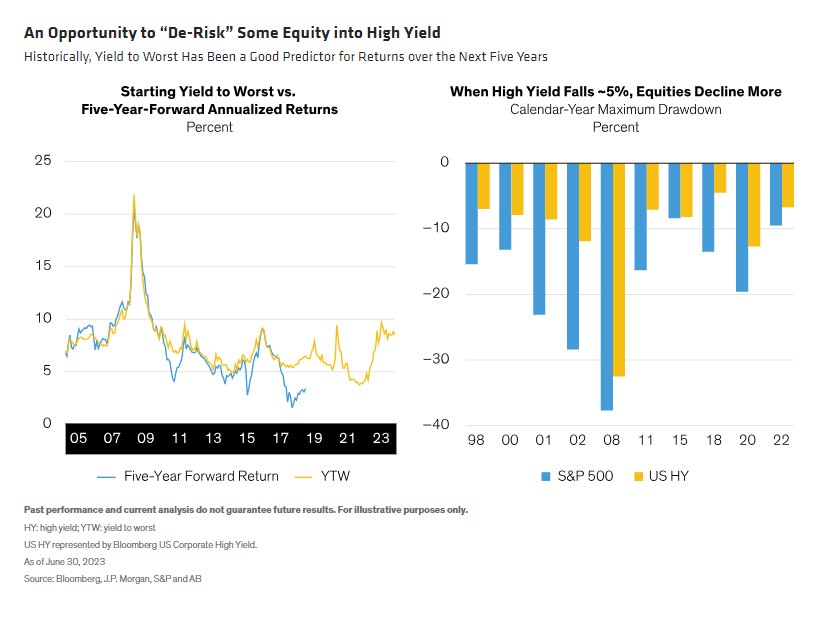

High yield is a good example of an opportunity to de-risk some equity exposure. Yields have historically translated closely into annualized returns over the ensuing five years (Display, left). At midyear, yields stood at a very attractive 8.5%. What’s more, high-yield downturns have typically been less than those for stocks (Display, right). Fundamental credit conditions have started to moderate, though they’re starting from a strong point.

An Attractive Entry Point for Municipal Bonds

In the tax-exempt bond arena, municipal returns remained volatile, though they did finish the first half of 2023 on positive ground. So far this year, municipal credit, particularly BBB-rated and high-yield bonds, have benefited the most. So has duration, or interest-rate exposure, with longer-maturity bonds outperforming those with nearer maturity dates.

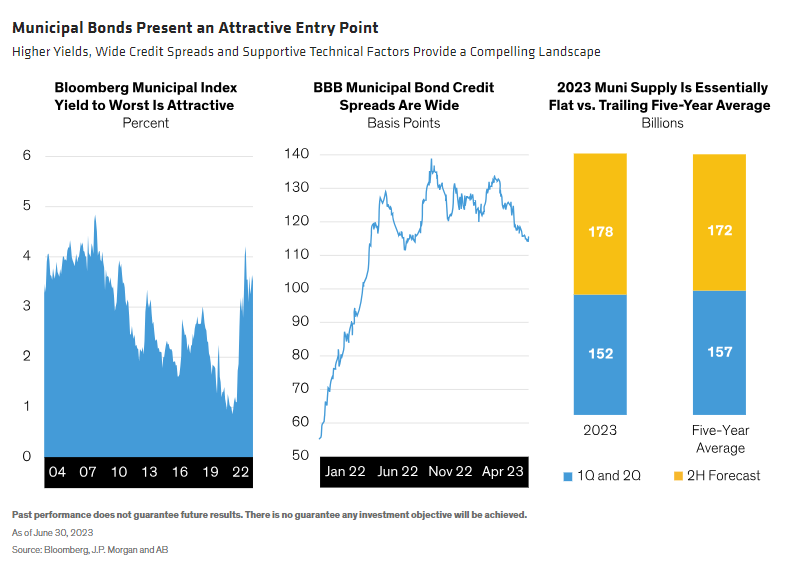

Higher yields (Display, left) and sizable credit spreads (Display, middle) combine with favorable technical conditions (Display, right) to create what we see as an attractive entry point. On the technical front, the supply of municipal bond issues has been essentially unchanged so far this year from the previous five-year average—a situation we expect to continue. Combined with pent-up demand in growing money-market assets, the supply-demand picture is promising right now.

As investor flows return to the muni market, we see the potential for outperformance, particularly in credit. Yields on BBB-rated and high-yield municipal bonds, adjusted for their tax advantages, are compelling versus taxable bond counterparts in light of munis’ much lower historical default rates. High starting yields and potential declines in credit spreads equal a strong opportunity, in our view.

The Big Picture

Our view is that inflation rates and economic growth will generally move toward their long-term trends as the resistance phase in markets ultimately gives way to the normalization phase. Prevailing yields are likely to fall as that process happens—a view shared by the Fed and the rest of the market.

Current conditions call for caution in making portfolio decisions, but investors who wait for a “better time” to tap into potential could face a sizable opportunity cost. That should be factored into investment choices as well. Because investors have diverse objectives and preferences, the big question is: What’s the right portfolio construction for me now?

The views expressed herein do not constitute research, investment advice, or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© AllianceBernstein

Read more commentaries by AllianceBernstein