The Long View

The dynamics of fiscal and monetary policy are now entering a new phase. Due to the emergence of negative Net National Saving (NNS), the law of diminishing returns can no longer fully capture the harmful effect of debt on economic growth. This new analytical framework indicates that the pronounced downward trend in the growth rate of the standard of living, evident since the 1970’s, is likely to persist. A redefinition of the monetary base and world dollar liquidity (WDL) is needed to capture the pure impact of central bank actions on business conditions. These new monetary measures, which are more restrictive than the old standards, indicate that the Federal Reserve is on the path to reducing inflation to the policy objective.

The aggregate production function, an important economic concept, combines technology with the three production factors (land, labor, and capital) to determine real economic growth. From this function, we derive the law of diminishing returns. This law reveals that the overuse of any factor of production will eventually result in lower output, which is a physical concept. An initial increase in a production factor will increase output, however continued inputs of the same factor will result in no new output and its continued overuse will eventually result in declining output. As such, overuse of one of the factors of production leads to diminishing marginal revenue product, or the amount of output gained for each marginal increase in a given factor of production.

For more than a decade, scholars including Quarterly Review and Outlook First Quarter 2024 Reinhardt, Reinhardt and Rogoff have found that the overuse of debt impedes economic growth when gross government debt as a percentage of GDP generally exceeds 80-90%. While increased indebtedness boosts the economy in the short run, its overuse and the law of diminishing returns prevail over time, thus increasing the use of debt becomes disinflationary. Now, with debt standing at a more harmful stage, in terms of impeding economic growth, another powerful economic factor that has been adding restraint is negative NNS. Based on the circular flow, which is GDI = GDP = Output of Goods and Services, net physical investment (I) = NNS. Therefore, if NNS is negative, then I is negative, meaning that the capital stock will not increase. This will lead to economic stagnation. An often made presumption is that technology will bail out the economy. Technology boosts economic growth by increasing capital stock and making labor and natural resources more productive. This presumption is rendered moot if NNS is negative. The lack of NNS substantiates Fed Chair Powell's statemant that "fiscal policy is not sustainable." During periods of negative NNS, ceteris paribus (all other things being equal), a growth standstill would reinforce disinflationary conditions, pending the actions of the Federal Reserve. The Fed could accelerate money growth, resulting in faster inflation while not eliminating the problem of negative NNS. In this case, prices and nominal GDP would rise for a short period of time, but the Fed’s actions would not boost the trend rate of growth in real GDP. The burden of higher inflation would fall most significantly on modest and moderate-income households, thereby worsening the income and wealth divides.

Richard Cantillon, who died in 1734, or 42 years before Adam Smith's Wealth of Nations, wrote that this would result from rapid money growth and thus was quite prescient. In the March FOMC announcement, the Fed reconfirmed a solid resolve to hit its 2% inflation target, a tacit confirmation that the Fed understands what Cantillon did three centuries ago.

A Modernized Monetary Base

The monetary base (MB), derived from the consolidated balance sheet of the Fed and the Treasury, has an asset, or source side, and a liability, or use side, comprised of total reserves (TR) and currency. First quarter increases in MB and TR, based on the historical approach, suggests that the Fed shifted away from restraint with inflation above their target. Former Board Member Kevin Warsh said in March the Fed was "goosing" the economy. With the passage of time and more historical observations, a greater understanding of how monetary policy works requires a reinterpretation of these long-existing monetary terms. Based on this alternative view, Fed restraint intensified in the first quarter.

The objective of the MB was to create an exogenous variable that is not determined within an economic model but plays a role in determining the values of the endogenous variables. The MB was conceptualized by economists Karl Brunner (1916-1989) and Alan Meltzer (1928-2017) in the 1960s. James Tobin (1918-2002) developed a virtually identical concept called "outside money." The MB and outside money contain endogenous variables, but their volatility has become considerably greater over the past six to seven decades, creating the need for a variable capable of capturing appropriately the Fed's influence on the economy, absent feedback effects. The exogenous component of the asset side of Fed's balance sheet is the SOMA (System Open Market Account). Securities held outright at the Fed is what we define as permanent reserves (PR). PR reflects assets that have longer term maturities. They differ from the Fed’s endogenous assets that provide transitory reserves (TR) and are mainly used to offset swings in operating factors like the Treasury General Account, currency in circulation or changes in Fed’s loans made over the Discount Window. While Fed assets rose as TR increased more than PR declined in the first quarter, the decline in PR will in time lead to a further contraction of monetary and credit growth and reinforce the Fed’s restraint imposed of the prior two years.

A Modernized World Dollar Liquidity (MWDL) Measure

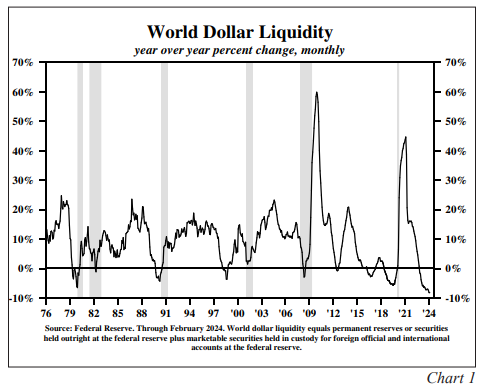

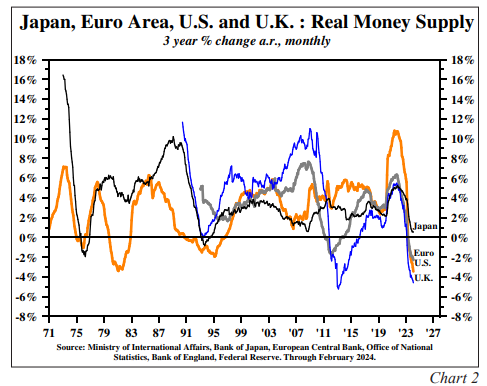

Four decades ago, Dr. Rod McKnew argued that since the dollar is the world's reserve currency, the Fed is also the world's central banker. To reflect that, he created the concept of WDL, which he defined as the MB plus marketable securities held in custody for foreign official and international accounts at the Federal Reserve. PR should replace MB in this definition. Chart 1 illustrates the outstanding track record of this MWDL, which decelerated sharply before all the recessions since 1976. The year-over-year change in MWDL went negative in all recessions except the one in 2000-01. MWDL has dropped by a record 9% in the twelve months ending February 2024, indicating the Fed’s restraint is intensifying on global markets. For instance, real money growth is negative in the Euro Area and the United Kingdom, and Japan is experiencing the slowest growth in twelve years (Chart 2). Combined with Japan's recently adopted tighter central bank policy, the risk is that Japanese money growth could turn negative. The record contraction in MWDL will exert additional restraint on a global economy where the Euro Area, the UK, and Japan are in either technical or quasi-recessions, and China is in deflation.

Concluding Thoughts

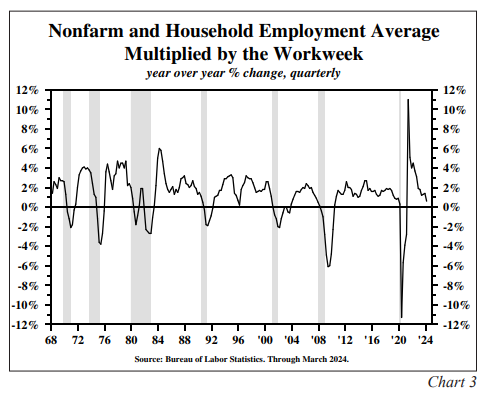

The consensus forecast believes the economy is buoyant, supported by robust labor markets and a resilient consumer. In dating business cycles, the National Bureau of Economic Research (NBER) gives equal weight to nonfarm payroll employment and household employment since the two series often diverge as they do now, with payroll up and household down. Following the approach of the NBER, we created a series that takes the average of payroll and household measures weighted by the weekly hours worked from the payroll survey. Aggregate hours worked for this new indicator increased 0.6% in the first quarter versus a year ago, down from increases of 1.4% in 2023 and 0.9% in 2019 (Chart 3).

Some contend fiscal policy will dominate monetary policy in the post-Covid economy. Due to the outlook for many years of large budget deficits, this view means that monetary policy actions will be incapable of containing inflation at a pace close to the Fed’s target. But, unless the Fed abandons its inflation mandate, for which the Fed Chair recently said there is "no wiggle room," the vast deficits will have the perverse impact of restraining growth and dis-inflate the economy as negative NNS prevails.

The contractionary effects of monetary policy and the de-facto negative NNS policy stance of fiscal policy will serve to place increasing downward pressure on inflation and growth. A sharp 7% rate of decline in vehicle sales In the first quarter is a sign that the deflationary trend in big ticket consumer goods prices is more likely to gather speed than reverse. The inflation rate will likely undershoot the Fed's target, and the unemployment rate will move higher than anticipated by the Fed. Inflation and unemployment are lagging indicators, and much of their cyclicality occurs after, not before, recessions end. This declining inflation environment will continue to bring down inflationary expectations and long-term Treasury bond yields.

DISCLOSURES

Hoisington Investment Management Company (HIMCo) is a federally registered investment adviser located in Austin, Texas, and is not affiliated with any parent company. The information in this market commentary is intended for financial professionals, institutional investors, and consultants only. Retail investors or the general public should speak with their financial representative. Information herein has been obtained from sources believed to be reliable, but HIMCo does not warrant its completeness or accuracy; opinions and estimates constitute our judgment as of this date and are subject to change without notice. This memorandum expresses the views of the authors as of the date indicated and such views are subject to change without notice. HIMCo has no duty or obligation to update the information contained herein. This material is intended as market commentary only and should not be used for any other purposes, including making investment decisions. Certain information contained herein concerning economic data is based on or derived from information provided by independent third-party sources. Charts and graphs provided herein are for illustrative purposes only. This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of HIMCo.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Hoisington Investment Management

Read more commentaries by Hoisington Investment Management