Executive summary:

- There are some tentative signs of improvement in China’s beleaguered property market, but consumer confidence remains very low.

- We estimate that the 10% tariff the U.S. recently implemented on Chinese imports could create a 0.3-percentage-point drag on China’s GDP growth.

- Our outlook for Chinese equities in 2025 is marginally positive.

- Consumer behavior and the evolution of China’s trading relationship with the U.S. are likely to be the main forces that shape how the year unfolds

2025 is beginning in much the same manner as 2024, with investors focused on whether the Chinese government is going to implement new stimulus measures. This year, however, there are two new developments: the release of the DeepSeek AI (artificial intelligence) model and the initiation of U.S. tariffs on Chinese exports. Amid this backdrop, we believe investors should focus on consumer behavior, the government’s reaction to economic conditions, and the evolution of the U.S.-China relationship.

Property transactions tentatively improving

The property sector remains the key drag on China’s economy—developers are still under pressure, while consumers are cautious on buying property. However, we are seeing tentative green shoots in recent transaction data for secondary homes, suggesting that all the supportive measures put in place through 2024 might be starting to bear some fruit.

However, it is important to highlight that it is not all improvement on the consumer front. Consumer confidence is still very depressed and is close to the lows of the last four years. Additionally, the economy continues to flirt with deflation, which could become a significant headwind if deflation expectations become entrenched. This would lead to consumers delaying the purchase of major goods due to anticipated further price declines.

Policy reaction to tariffs remains unclear

As we head further into the year, the focus will be on the National People’s Congress meeting in March, where the government will announce its economic growth target for the year as well as any new policy measures. In our view, if an economic growth target of around 4.5% is announced, it will likely have to be accompanied by a more meaningful stimulus measure.

Another key watchpoint for Chinese policy will be the reaction to the 10% tariff rate put in place by the U.S. on Feb. 4. So far, China has responded by placing tariffs on $14 billion of U.S. imports, included coal, crude oil, liquified natural gas (LNG), and farm machinery. These tariffs went into effect on Feb. 10.

It’s important to note that while the 10% U.S. tariff rate on Chinese products is lower than many had feared, we estimate it will still create a drag on GDP (gross domestic product) growth of around 0.3 percentage points. The U.S. is set to complete its trade policy review by April 1, and we expect that China will be quite constrained in retaliation before that period is released.

AI advances have been impressive, but chips likely remain a constraint

There has been a lot of focus on AI developments in China, with Chinese startup DeepSeek reporting that it has achieved significant gains at a small cost. In the same week that DeepSeek made its announcement, there were three announcements from other companies in the country (Bytedance, Moonshot and Alibaba), all of which illustrated impressive improvements. This reflects the high level of competition that occurs in China—as proof, one can simply look at the rapid innovation and reduction in costs that Chinese electric vehicles have seen over the last four years.

Moving forward, we are likely to see more focus on efficiency from Chinese AI developers. However, further improvements to both capabilities and scale will likely prove challenging, given the export embargoes that the U.S. has put on major chip manufacturers. Reflecting these concerns, the founder of DeepSeek recently noted in an interview that the main challenge for the company is not funding but securing the necessary computing power (i.e., chips).

What are the potential market implications?

At Russell Investments, we use a cycle, valuation, and sentiment framework to guide our investment decision-making process. Using this framework, our outlook for Chinese equities is marginally positive.

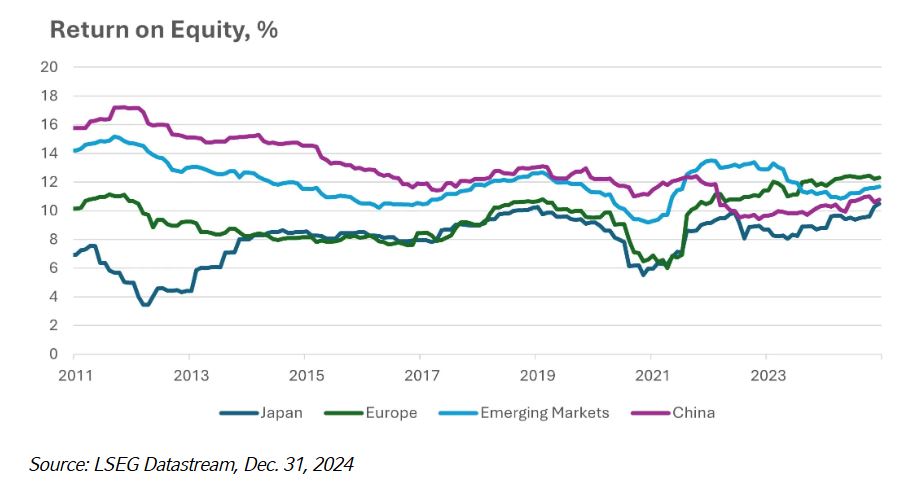

Starting with the business cycle, whilst there is quite a bit of uncertainty around the economic outlook, Chinese companies have continued improving their return on equity (as shown in the chart below). Analysts are looking for about 9% EPS (earnings-per-share) growth through 2025, which seems achievable if the economy can achieve GDP growth of around 4.5% and corporates see some margin expansion.

From our vantage point, valuations for Chinese equities continue to look reasonable, both on an absolute basis and relative to other emerging markets. Forward multiples are at an undemanding 10 times, while the so-called PEG ratio (or price-to-earnings-to-growth ratio—i.e., the earnings multiple divided by the long-term growth estimate) is at the 15th percentile relative to history.

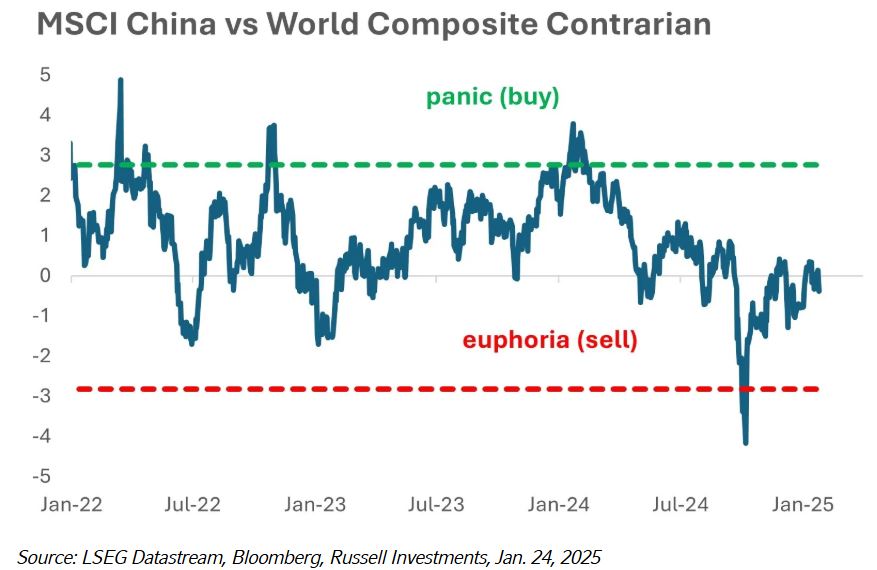

Our sentiment measure is currently very neutral right now, after having been overbought in the second half of 2024 on expectations of further stimulus. This will be a key watchpoint through this year, especially as the market digests geopolitical and policy developments.

Finally, it is worth touching on the Chinese yuan. Given the potential headwinds of tariffs, we think it is likely that we might see a bit more downward pressure on the yuan through this year. Conceptually, this has two benefits for China—the first being that it helps with alleviating some of the hit to competitiveness.

The second, and less obvious, benefit is that it could provide some upward pressure to imported prices—which could potentially help push the economy away from deflation. However, this pressure is likely to be limited and controlled, given China is also in the process of trying to internationalize the yuan—and therefore does not desire big swings in currencies.

The bottom line

The Year of the Snake is shaping up to be an interesting year for China. Market expectations are fairly subdued at this point, which presents some potential asymmetry—especially if chatter around the potential for additional stimulus picks up again.

Ultimately, we expect that consumer behavior and the evolution of the U.S.-China trading environment will be the main forces that drive how 2025 unfolds. We will continue to keep you updated as the year progresses.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Russell Investments

Read more commentaries by Russell Investments