Executive summary:

- Our research estimates that the proposed slate of U.S tariffs on key trading partners would result in a 60-to-80 basis-point (bps) increase in cost structures across most sectors of the global economy.

- During 2018-19, when the U.S. imposed tariffs on steel and aluminum products from most other countries—in addition to a wider array of tariffs on Chinese products—REITs and infrastructure were generally the strongest-performing asset classes.

- If the current proposed tariffs are implemented, our model indicates that the U.S. energy, materials, industrials, and consumer discretionary sectors are likely to be the most impacted—and the U.S. financials and communications sectors the least impacted.

U.S. trade policy remains highly fluid, with the government announcing several tariff proposals since President Donald Trump took office last month. As of this writing, the Trump administration has implemented a 10% tariff on imports from China and announced plans to enact a 25% tariff on all imported steel and aluminum products in early March. In addition, the U.S. may move forward with an earlier plan—which was put on pause last week—to tax all Canadian (excluding energy) and Mexican imports at a 25% rate beginning next month. Finally, the U.S. administration is also reportedly looking at the imposition of reciprocal tariffs (i.e., imposing the same tariffs on imports that U.S. exports face) to all U.S. trading partners.

Amid uncertainty over the potential market and economic impacts of these tariffs, our strategist team at Russell Investments has developed a model that allows us to input a wide range of different tariff scenarios—for example, a 25% U.S. tariff on Canadian imports, or blanket U.S. tariffs on all steel imports—to see what the potential impacts would be on cost structures for both U.S. and global businesses.

How could today’s proposed tariffs impact the global economy?

If the current slate of proposed U.S. tariffs is implemented, our model estimates a 60-to-80 bps increase in cost structures across most sectors of the global economy. We also think it’s very likely that companies will pass on this increase to customers in full, as has been the case in previous tariff episodes. To this end, we anticipate that core U.S. consumer prices—as measured by the PCE price index—would rise by about 70-80 bps.

These estimates are based on a number of inputs, as well as observations from how markets and economies reacted to the implementation of U.S. tariffs during the first Trump administration. Let’s take a deeper look.

Market impacts from U.S. tariffs during the first Trump administration

During President Trump’s first term in office, the U.S. implemented tariffs on steel and aluminum products from most other countries from 2018-19, as well as a wider array of tariffs on Chinese products. During this time, there was a notable decrease in correlations between different equity regions—which makes sense, given that the economic impacts of the tariffs varied by country.

Of particular note, both REITs (real estate investment trusts) and infrastructure performed well during this period, primarily due to the lower tariff risk and some discount rate movements.

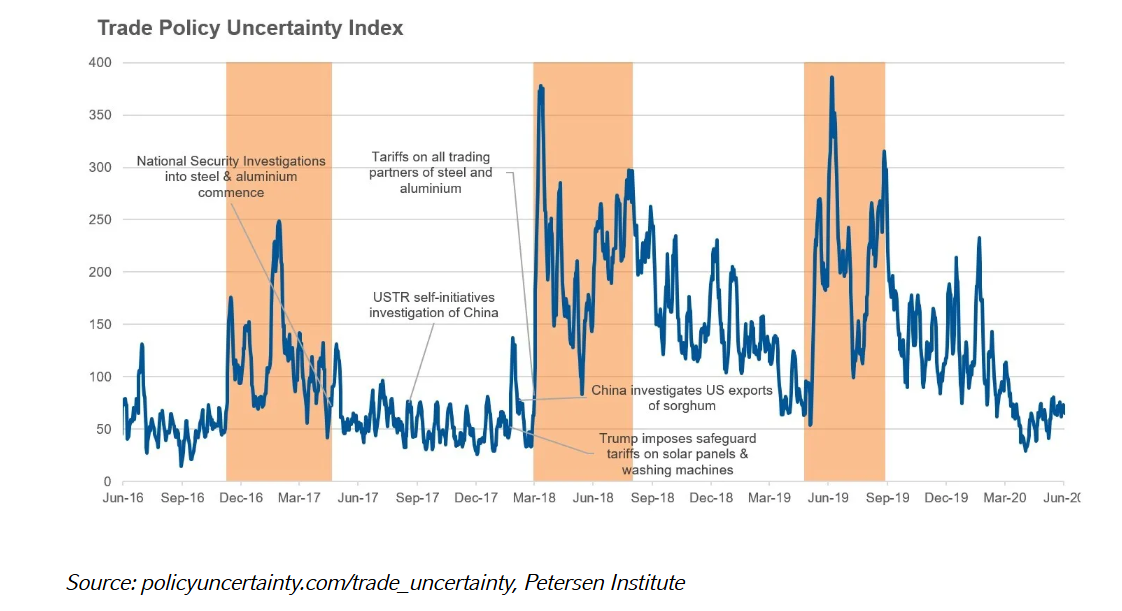

Trade policy uncertainty index

A good measure of the uncertainty around U.S. tariffs during the first Trump administration can be demonstrated by looking at the so-called Trade Policy Uncertainty Index. This index crawled online news articles for words that suggested uncertainty in trade policy during this time.

As the chart shows, the index identified three main periods of elevated trade uncertainty from 2016-2020. The first was the period following Donald Trump’s initial presidential election victory, in November 2016, through his first few months in the White House in early 2017. During this time, worries over potential U.S. tariffs mounted, but no policy actions were taken.

The second period, from roughly March through August 2018, is when the Trump administration finished its investigations into Chinese trade practices and announced a flurry of tariffs, with many targeting Chinese goods. The third period occurred the following year, in 2019, when the U.S. administration implemented another round of tariffs on key trading partners. Of these three periods, the second and third are the most important from an economic perspective, since that’s when the tariffs were actually implemented.

So, how did asset classes perform during both times?

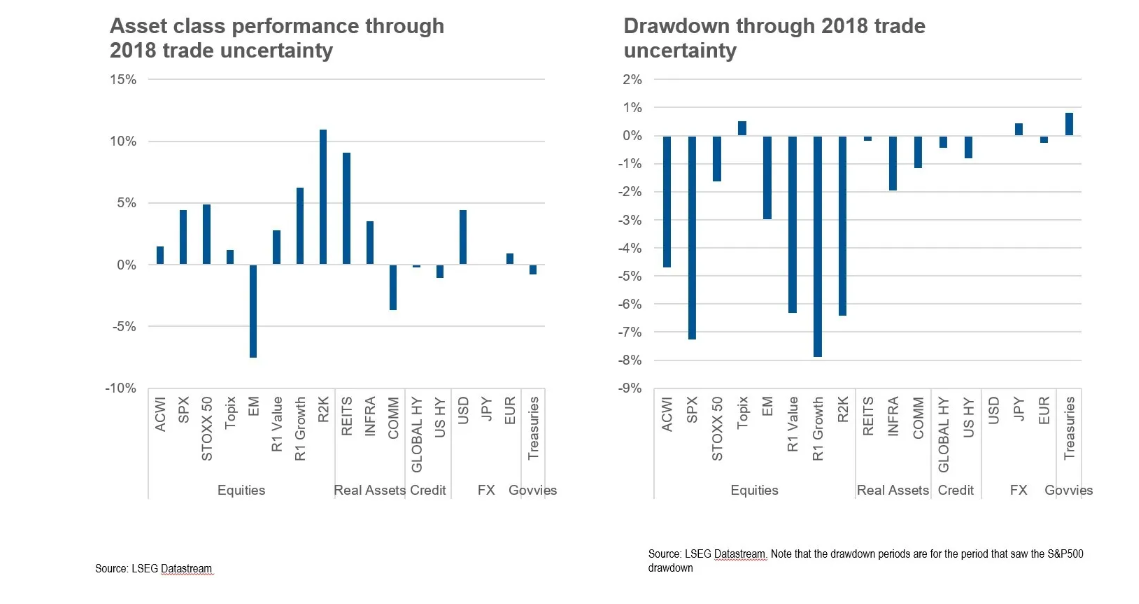

In the image below, the chart on the left shows how equities, real assets, bonds, foreign exchange, and government bonds performed from Feb. 28 to Aug. 1, 2018.

One of the main things that jumps out is the struggles of emerging-market equities, which is understandable given that China makes up roughly a quarter of the MSCI Emerging Markets Index. On the flip side, the Russell 2000 Index of small cap stocks surged by over 10% during this time frame, with REITs also gaining by nearly as much.

The righthand side of the chart shows the performance of the same asset classes during the peak drawdown of the U.S. equity market in 2018—from March 9 to April 2—as measured by the S&P 500 Index. Once again, REITs and, to a lesser extent, infrastructure experienced far less of a decline than other assets during this timeframe.

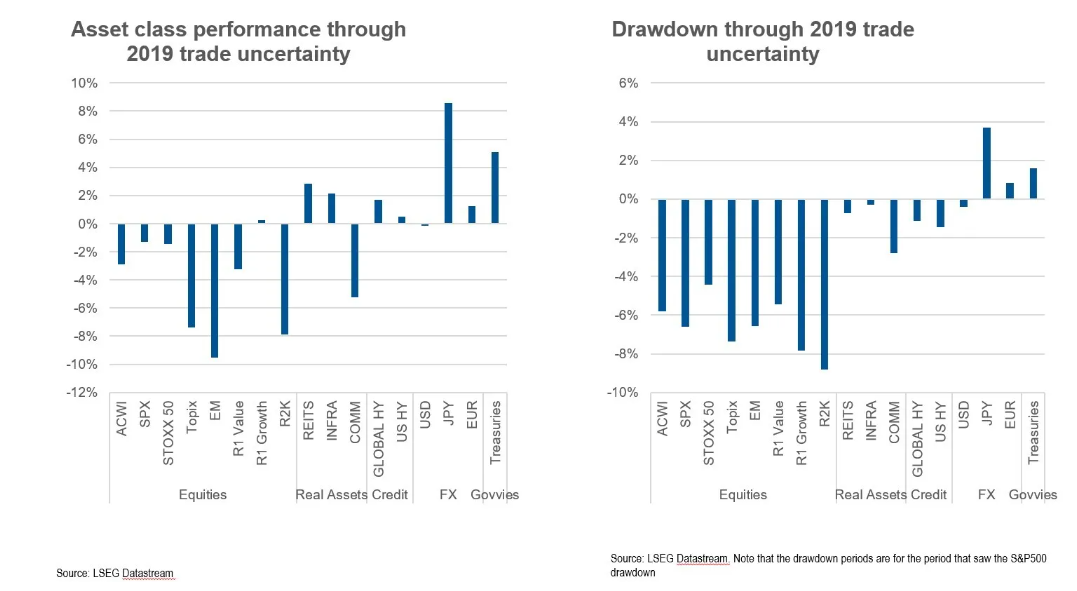

What about in 2019? This time, there was more of a classic risk-off tone, with equity markets declining while perceived safe-havens like U.S. Treasuries and the Japanese yen did well. Yet again, REITs and infrastructure performed strongly.

Estimating the input costs of tariffs

Next, let’s look at how we constructed our model for tariff input costs. We use data from the U.S. Bureau of Economic Analysis to see what inputs are used for each sector in the economy. The second step is to then look at the import reliance of each of these inputs. With these two steps, we then can apply tariff assumptions by country and, if necessary, product line. Product line is an important ability in cases like Canada, where the Trump administration carved out a lower tariff rate on energy resources.

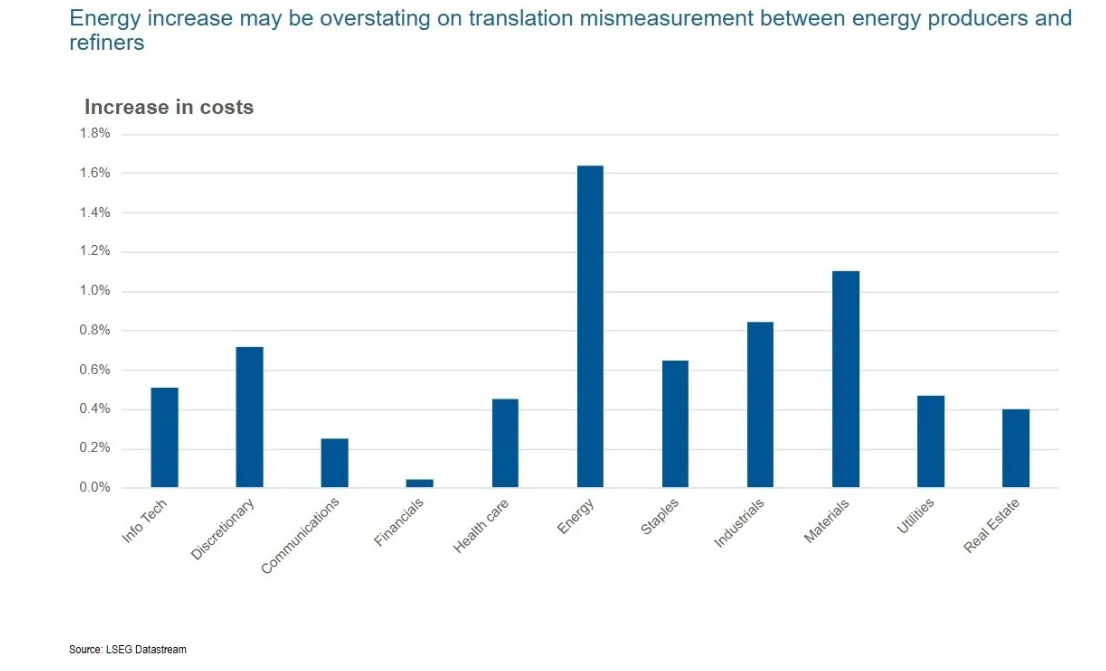

The result is the below chart, which estimates the increase in input costs across U.S. equity sectors. There’s an average overall increase of roughly 80 bps for U.S. sectors, with energy, materials, industrials, and consumer discretionary impacted the most. On the other side of the coin, the financials and communications sectors are estimated to be the least impacted. If we drill down further, motor vehicles, electrical equipment, and transportation in particular are the most impacted.

Chart: Estimated increase in input costs across U.S. equity sectors

The bottom line

Our research indicates that the latest proposed slate of U.S. tariffs are likely to result in a modest increase in cost structure for global organizations. As U.S. trade policy continues to evolve, we’ll monitor the latest developments and share updates from our model accordingly.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Russell Investments

Read more commentaries by Russell Investments