In recent years, the global healthcare sector has seen rapid growth and generally strong performance. But its pay practices leave something to be desired, in our view—too often rewarding executives even if their company fares poorly. We think this issue deserves a closer look by investors.

Having engaged* with more than 100 healthcare firms on compensation-related issues, we’ve found misaligned pay incentives to be pervasive. Many companies reward executives even when they fail to create value for customers and shareholders. In our view, only when executives do well by their customers and shareholders should they do well themselves.

The Plague of Poor Pay Incentives

Poorly designed pay incentives abound—from early-stage IPOs to established healthcare companies across subindustries.

For example, many large pharmaceutical and medical device companies adjust litigation and compliance expenses out of executive compensation calculations. This can result in generous bonuses even in years when stakeholders are adversely affected by legal settlements and penalties that detract from financial performance. Companies sometimes characterize litigation expenses as legacy concerns, since the alleged damages occurred in the past—or as one-offs, despite multiple occurrences.

We think investors should be particularly wary of these tactics when practiced by firms with recurring product-quality and safety issues. Our view on this is simple. If executives can be rewarded for selling legacy products, then they should also be accountable for managing the legal risks.

IPOs, too, may create poor incentives. New research from Yale Law School reveals that early-stage biotech firms frequently partake in a practice called pre-IPO option discounting. This involves awarding options to insiders shortly before an IPO, with an exercise price well below the expected IPO price. This risky practice can create an immediate windfall for insiders, without any meaningful performance conditions or approval from public investors.

In a sample of more than 100 newly public biotech companies, researchers found that more than two-thirds of these firms awarded discounted options to insiders. On average, recipients enjoyed a discount of 48% off the IPO price.

Of course, there must be incentives to develop new therapies, and we’re in favor of well-structured option grants. But we think pre-IPO option discounting warrants closer scrutiny from investors, as it may create a day-one jackpot for executives but dilution down the road for public investors.

A Three-Step Prescription for Incentivizing Executives

While there’s no miracle cure for a broken compensation program, we’ve identified three core themes that can help signal an effective pay program.

-

Profitable innovation: Executive awards often work best when linked to multiyear financial and strategic goals. These can include operating profit and return on invested capital, as well as employee satisfaction and retention metrics. We also look for clear incentives to innovate, with potential touchstones including patents and FDA approvals.

-

Equity alignment: A significant equity stake can provide a powerful incentive to healthcare executives. When the company does well, management should also do well, and vice versa. For this reason, we keep a close eye on the equity/cash mix of executive pay packages, as well as the length of vesting periods, the robustness of share-ownership guidelines and the presence of clawback provisions.

-

Value-based care: Ultimately, healthcare companies should provide value to customers, shareholders and the healthcare system as a whole—with pay packages structured accordingly. Beyond improved patient outcomes and lower cost of care, key metrics may include net promoter scores or hospital star ratings.

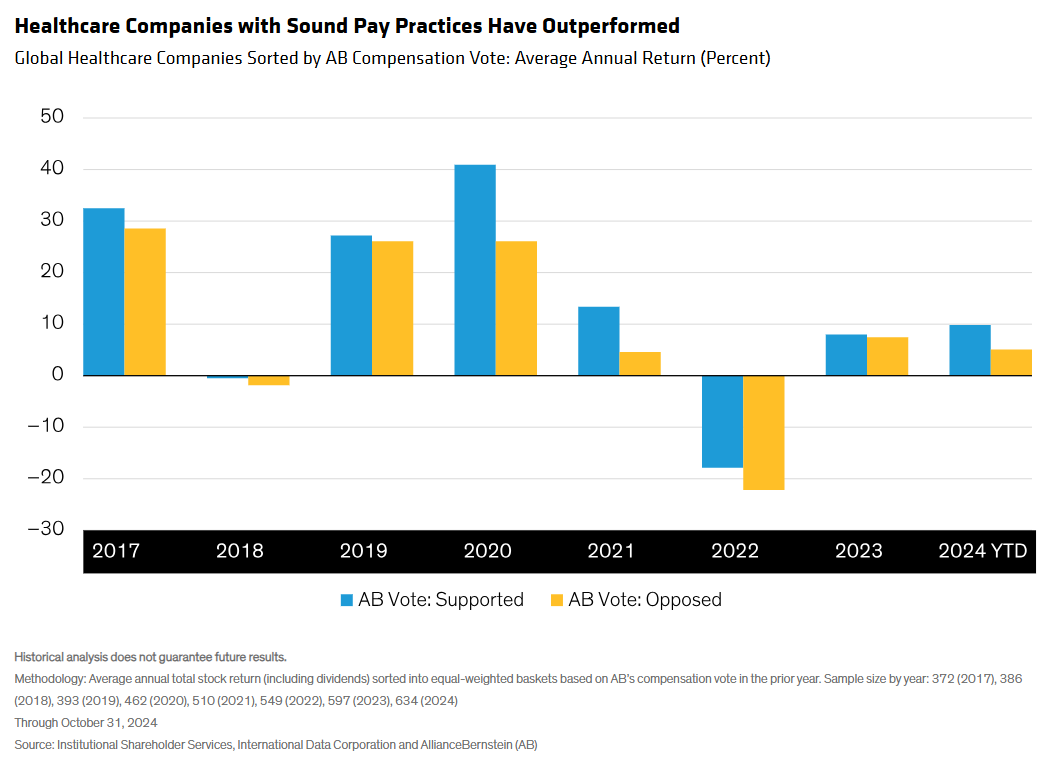

Strong Incentives Precede Strong Performance

Historically, companies with sound incentive structures have outperformed those with misaligned incentives. That’s why, when we determine that a company’s compensation structure fails to adequately incentivize long-term performance, we vote against it—something we’ve done more often than not. We believe that avoiding such companies may boost potential return.

In fact, our latest proxy voting study indicates that properly structured compensation packages have historically been a leading indicator of outperformance. Since 2017, global healthcare companies with compensation practices that we support (sound incentive structures) have posted higher average returns in the following calendar year than those we don’t support (misaligned incentives) (Display). This holds true when controlling for subindustry.

Assessing a company’s executive compensation structure is only one component of fundamental analysis, but in the case of healthcare investing, it has material implications. Healthcare executives effective in improving health outcomes deserve to be rewarded for their leadership, but it’s up to investors to verify.

Active managers can help weed out companies that favor insiders over investors while prioritizing firms with shareholder-friendly pay practices. Over time, we believe that companies with sound pay practices may deliver better long-term outcomes for patients and investors alike.

*AB engages issuers where it believes the engagement is in the best interest of its clients.

The authors would like to thank Landon Shea, Investment Stewardship Associate, and Peter Højsteen-Ljungbeck, ESG Data Research Analyst, for their contributions to this piece.

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein