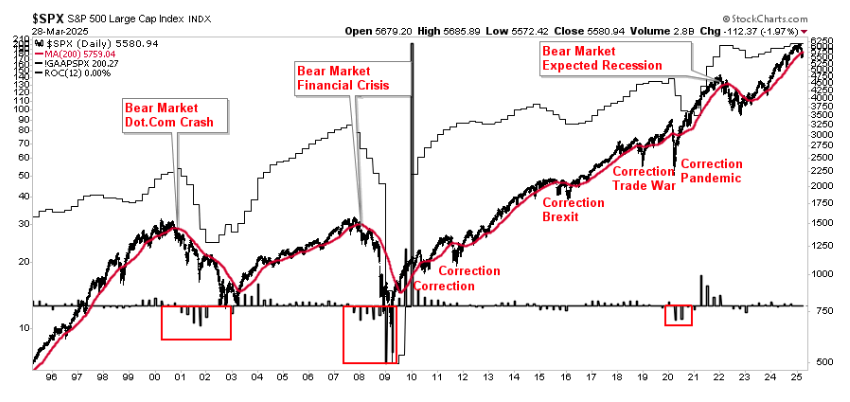

Last week, we noted that “nothing good happens below the 200-DMA,” and the tariff-induced market crash this past week confirmed that statement. However, we also noted that over the last 30 years, previous failures at the 200-DMA have also often been buying opportunities. That is unless some “event” of magnitude creates a massive shift in analysts’ estimates.

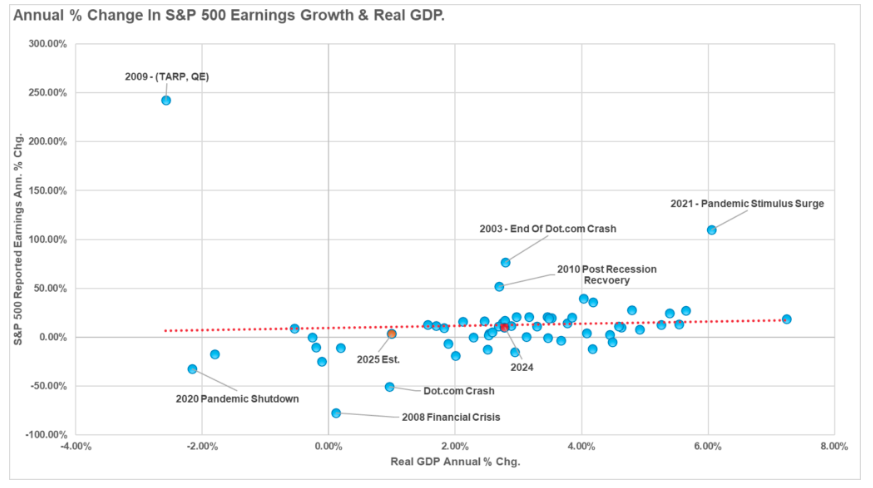

“For this chart, I label “bear markets” as periods when the market fails the 200-DMA and repeatedly fails subsequent retests of that moving average. If the market fails at the 200-DMA and recovers shortly thereafter, it is considered a “correction.” As shown, during the first two “bear markets,” earnings fell sharply as the economy slowed and a recession took hold. Outside the brief “Covid” pandemic, earnings remain well anchored to ongoing economic growth. If the current failure at the 200-DMA is the beginning of a deeper market correction, we should see earnings estimates beginning to fall more quickly.”

The question is whether the “tariffs” are an event that causes a massive negative revision to earnings and/or the onset of a credit-related crisis or recession. The answer to that question is critically important to today’s analysis: Was last week’s market crash a buying or selling opportunity?

The answer to that question is complex as we work with many unknowns.

- How will consumers respond to the impact of tariffs on their consumption?

- How will the companies respond to the impact of tariffs on their production and investment?

-

But also, how will companies respond to the change in consumer demand?

- Most importantly, and the only thing that matters, is the impact on corporate earnings.

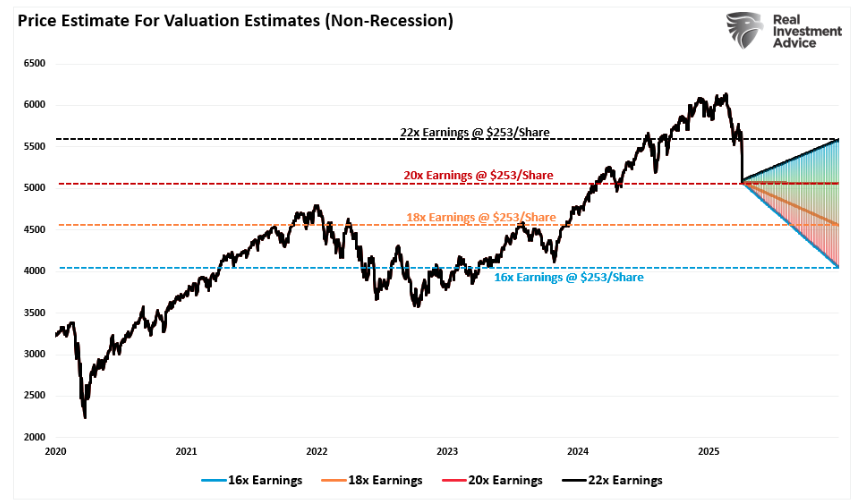

There is undoubtedly a very bearish case to be made from the overly draconian tariffs imposed by the Trump administration. The impact of higher costs on goods and services will lead to demand destruction by producers and consumers, leading to drastically lower economic growth rates. That impact should not be dismissed, as it has everything to do with earnings and whether or not the market crash is near its end. We can model out a couple of assumptions.

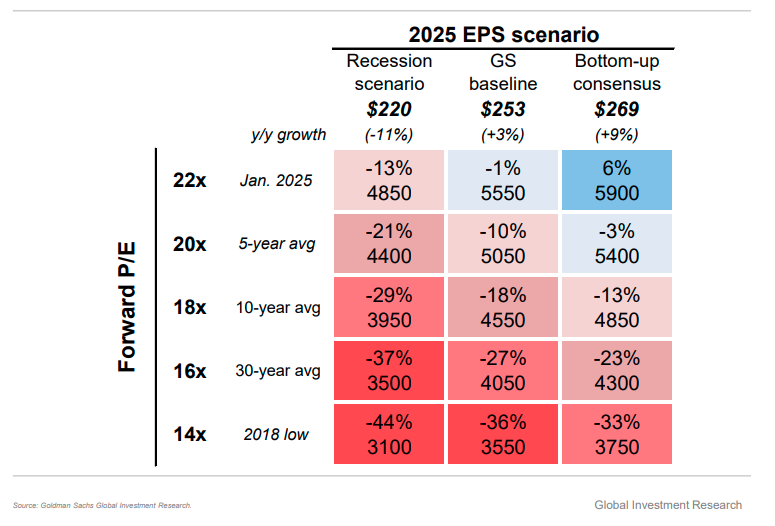

Let’s assume that Wall Street analysts are correct. In response to the tariffs, they revised their earnings estimates downward. For example, Goldman Sachs reduced its S&P 500 earnings growth forecast from 7% to 3% for 2025, citing the adverse effects of increased tariffs on economic growth and corporate profitability. As we know, economic growth rates and earnings have a very high correlation. If Wall Street analysts are correct, a slow-growth economic environment of 1% this year would allow earnings to grow near their long-term trend.

However, note the periods when earnings deviate from underlying economic activity. Those periods are due to pre- or post-recession earnings fluctuations. Therefore, assuming the market crash is a warning of an impending recession, we might consider 2020 as a model for potential outcomes. Given we are shutting down the economy, we can assume a -1% real GDP growth rate and a 4% decline in earnings.

So, what does that mean for the market and investors?

Given the range of outcomes (both recession and non-recession), we can apply a multiple to the market to discover where the price equilibrium may exist following the market crash. As noted by Goldman Sachs last week, the range of potential outcomes is extensive and heavily depends on the market’s valuation assumptions.

Using Goldman’s baseline expectations, we can model the range of outcomes for the rest of this year. It is worth noting that last week’s market crash has already reduced valuations significantly from their previous level. There is undoubtedly downside risk over the rest of this year if the market demands multiples closer to their 10 and 30-year averages. However, even if that is the case, substantial rallies will likely occur on the way lower.

Given the magnitude of the recent decline, the potential for a reversal rally has risen dramatically.

Market Crash Sets Up Extremes

Nothing in the market is ever guaranteed. However, much like going to Las Vegas and playing a hand of blackjack, there are times when the probabilities of a positive outcome significantly outweigh the possibilities of a negative one. If you understand the basics of blackjack, if you are holding a hand that equates to 20 points, that is a hand worth betting on. The reason is that the “possibility” of the dealer getting 21 without busting is fairly low. However, it does happen.

The same rules apply to investing. There are times when the probabilities of something happening outweigh the possibilities. Following last week’s market crash, the “probability” of at least a near-term rally outweighs the possibility of a further decline. Does that mean it is guaranteed to happen? No. But, several indicators have historically tilted the odds in the investor’s favor.

[Reader’s note: All of the following analysis is updated weekly in the Market Statistics Section of the #BullBearReport]

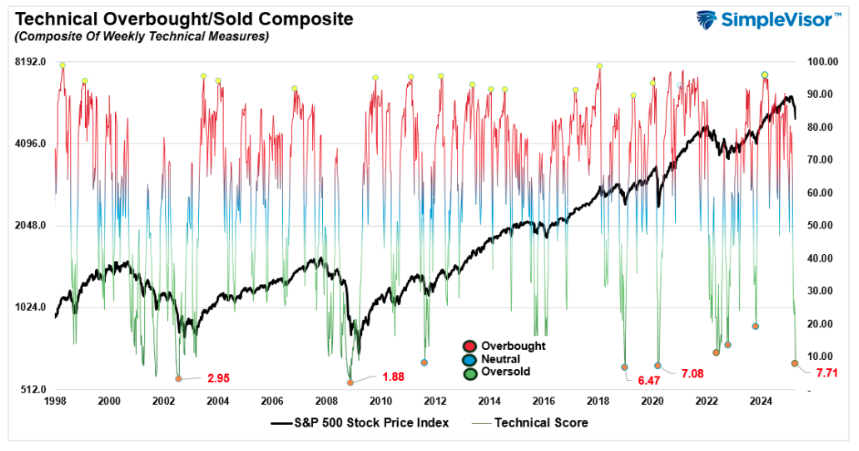

We will begin with the technical composite, comprised of several indicators that measure relative strength, momentum, and deviation from moving averages. The analysis is based on weekly price data, so reading extremes are far more critical to analytical outcomes. Last Friday, the technical composite registered a reading of just 7.71. That reading eclipses levels seen during the 2022 market correction and is near levels seen during the 2020 pandemic shutdown and the 2018 “Fed Taper Tantrum.” The only readings that exceeded current levels were during the 2000 “Dot.com” crash and the 2008 “Financial Crisis.”

Whether or not the current market crash is the beginning of a larger corrective cycle, such low readings have, without failure, marked the near-term low of a market correction. While the market has previously continued its corrective process after such low readings, such did not occur without a meaningful reversal rally first..

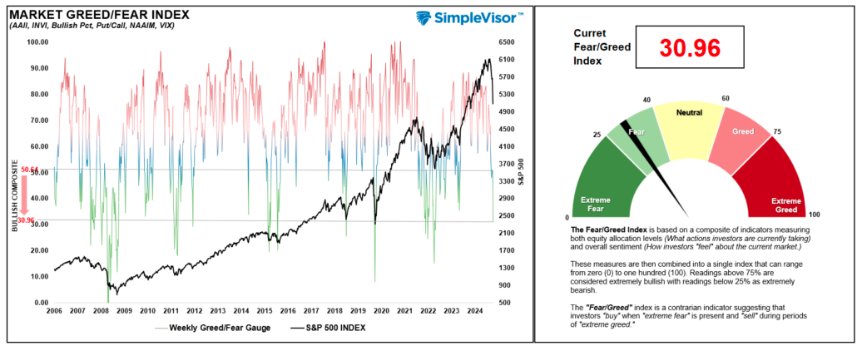

The very low sentiment and allocation measures readings also confirm the technical gauge. The fear/greed index combines weekly measures of retail and professional allocations, investor sentiment, volatility, and market breadth into a single reading to determine when investors are excessively “greedy” or “fearful.” While current readings are not as negative as seen during the 2020 correction or 2008 bear market, current readings are at levels that have also previously confirmed near-term market lows and reflexive rallies. When these readings are combined with the technical readings above, investors are provided with a higher degree of confidence versus non-confirmed readings.

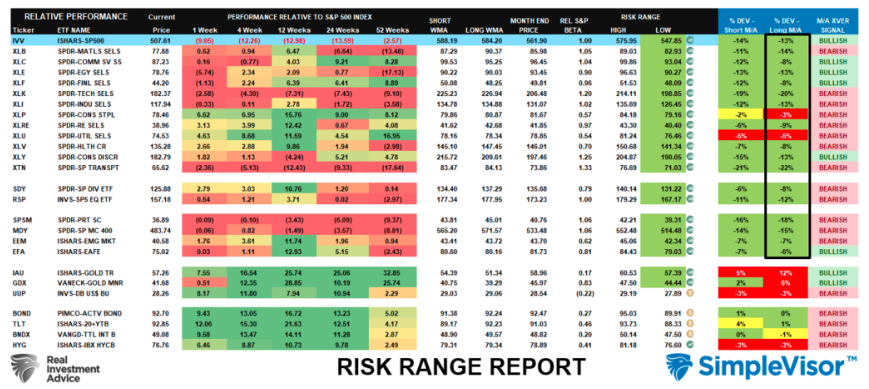

Lastly, the weekly “Risk Range Report” details three critical factors investors should know. The first is that the recent market crash has pushed every major market and sector well below normal monthly tolerances. Only during market crash events do you see such uniformity of extremes across all markets. Secondly, the deviations from longer-term moving averages have reached double digits. Such deep deviations across many sectors and markets are also unusual and historically precede bullish reversions to the mean.

However, the last column is crucial.

Currently, most markets and sectors are in bearish moving average crossovers, suggesting a larger corrective cycle is in process.

That part of the analysis is most critical to investors. With the markets deeply “offside” in sentiment and positioning due to the recent decline, investors should anticipate a short-term reversal. However, we should expect another decline before it’s “time to buy.”

Hope In The Fear

Our view is that the probabilities of a near-term rally outweigh the possibilities of a continued, uninterrupted decline. We can use technical analysis to create a “roadmap” of what such a reflexive rally might look like. In other words, there is “hope in the fear.”

Any sizeable reflexive rally will reverse the profoundly negative sentiment about the current market environment. That reversal from bearish to bullish will help propel the market in the near term. Investors will want to use that rally to reduce portfolio volatility until a more durable market bottom is identified. Bottoms are rarely formed during the initial decline. Furthermore, the markets are triggering weekly sell signals. This suggests that even though the market may rally, we can not call an end to the corrective cycle yet.

Lastly, the markets are simultaneously three standard deviations below long-term moving averages and challenging rising trend lines. Such oversold conditions typically precede short-term rallies to allow investors to reduce exposure to equities. The target for a tradeable rally is between 5500 and 5700. While the rally could be more significant, we will use those levels to begin risk reductions.

Our primary focus on this process will be:

- Reduce current positions by 1/4 to 1/2 of their current target weights.

- Increase cash levels

- Raise stop loss levels on long-term positions.

- Sell positions that have technically violated previous support levels or exceeded risk tolerances.

- Add to positions that are positioned to benefit from further market stress.

Following those actions, we will continue to monitor and adjust the portfolio accordingly. At some point, the valuation reversion will be complete, allowing us to reconfigure portfolio allocations for a more bullish environment. When that event occurs, we will change our portfolio allocations. That will include:

-

Reducing fixed income in exchange for dividends.

- Shift remaining income allocations to corporate bonds rather than Treasury bonds,

- Overweight equity allocations with a tilt toward undervaluation.

However, the last point is also an essential lesson in this analysis. Investors often forget that market corrections are constructive. The revaluation process realigns market dynamics to a more favorable state. For example, the largest Mega-capitalization companies, which have been under the most pressure over the last two months, now trade at the cheapest valuation level relative to the S&P over the previous 10 years.

However, the fear of further losses leads us to “sell bottoms” rather than “buy low.”

We focus on factors such as investor sentiment, technical analysis, and the fundamentals to guide us during periods of elevated fear. We are not suggesting this set of tools will allow you to buy the exact bottom or sell the top. But they offer better alternatives than just “raw emotions.”

It won’t take much for the market to find a reason to rally. That could happen as soon as next week. If the market rallies, we suggest reverting to the basic principles to navigate what we suspect will be more volatile this year. However, at some point, just as we saw in 2022, the market will bottom. Like then, you won’t want to believe the market is bottoming; your fear of buying will be overwhelming, but that will be the point you must step in.

Buying near market lows is incredibly difficult. While we likely aren’t there yet, we will be there sooner than you imagine.

As such, when you want to “sell everything,” ask yourself if this is the point where you should “buy” instead.

I hope this helps.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by Real Asset Strategies