KEY POINTS

Navigating Uncertainty as Trade Tensions Rise and Market Volatility Grows

-

Tariffs Intensify: The rollout of the Trump administration’s retaliatory tariffs escalate global trade tensions across all sectors and industries.

-

Markets in Turmoil: Increased volatility is likely to persist as policy uncertainty rises. Investors should look through drawdowns for strategic opportunities to invest across asset classes.

-

US Economy Softening: The US economy shows early signs of slowing growth which are being amplified by tariff policies.

-

Focus on Quality: Focus on credit selectivity and resilient sectors, use alternatives and less liquid investments to provide hedging and diversification from tariff and policy headwinds. Be cautious of blind pool risk in private markets, especially where company input costs may be rising.

-

Stay Disciplined: Maintain investment discipline despite short-term volatility. Staying invested typically delivers better long-term results than attempting to time the market.

Typically, our quarterly review reflects on the prior quarter’s market and economic trends while offering forward-looking insights. However, recent developments demand more immediate focus.

The global economy now stands at a crossroads, exacerbated by the recent escalation of tariff policies from the Trump administration. The implications extend beyond short-term market volatility; these tariffs fundamentally challenge decades of globalization and established business practices. Companies reliant on international trade, supply chains, and global markets face significant structural risks.

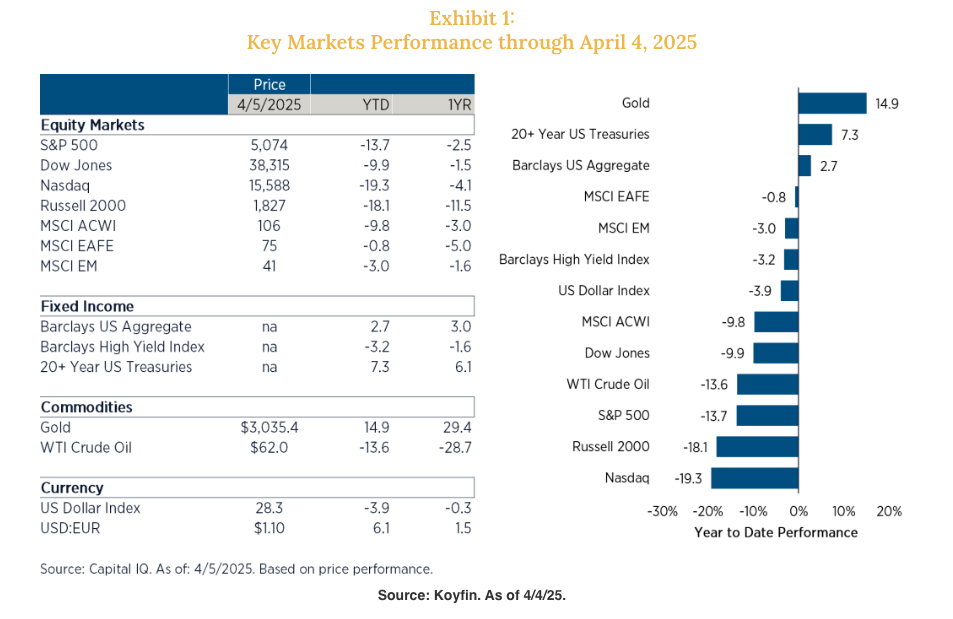

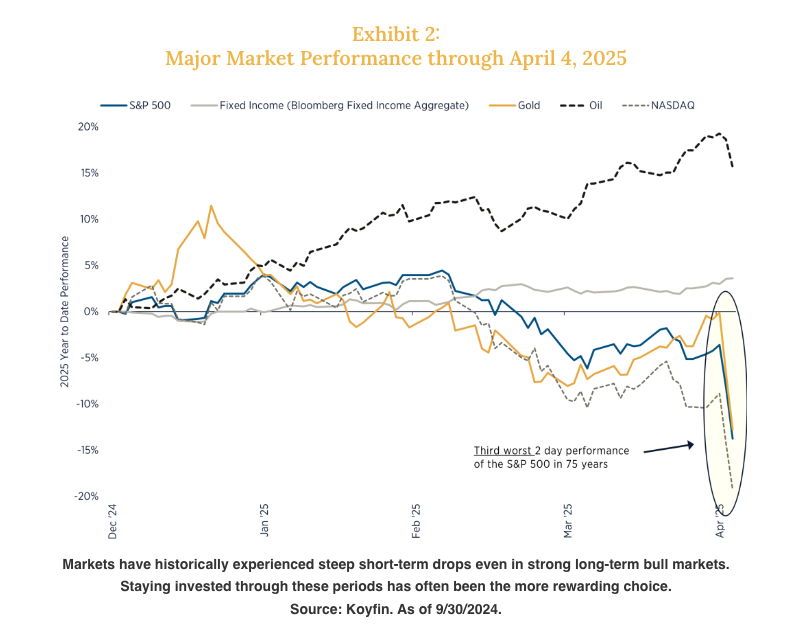

The Trump administration’s announcement of aggressive tariff policies has significantly shifted market sentiment, and our own outlook, from optimism to cautious anxiety. Markets reacted swiftly and sharply to these developments, with the two-day performance following Trump’s “Liberation Day” announcement ranking among the worst in S&P 500 history. This dramatic pullback places the reaction alongside other major historical events that triggered steep short-term losses, highlighting the lack of investor confidence in the face of unpredictable policy shifts.

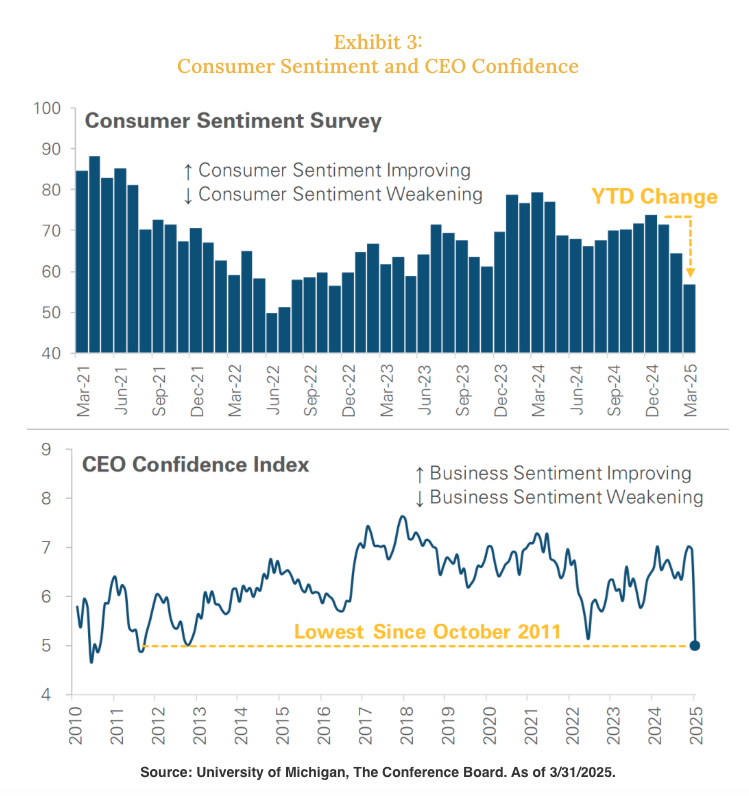

Indicators such as declining industrial production, falling CEO confidence, and moderating consumer spending growth underscore a broader economic slowdown, further amplified by these escalating trade conflicts. While job growth remains healthy and housing activity is improving, consumer spending is slowing. As we’ve noted previously, the U.S. consumer has been the key driver of U.S. economic outperformance.

The new wave of tariffs will likely weaken this pillar of strength, compounding the risk of a broader economic slowdown. Additionally, there is now growing concern around the magnitude of tariff-related disruptions to corporate earnings, particularly in sectors such as technology, industrials, and consumer discretionary, which have high exposure to global supply chains.

Given these conditions, investors should consider proactively reviewing their portfolios to ensure adequate diversification. At the same time investors should be looking at markets and knee-jerk moments of volatility as an opportunity capitalize on dislocations and put capital to work. For those without additional dry powder we suggest working with your advisor to review your asset allocation in more detail.

Market volatility is likely here to stay, at least in the short term. However, it’s important to remain steadfast—history repeatedly demonstrates that consistent investment, even through turbulent markets, generally outperforms reactive timing strategies. For instance, markets typically experience a drawdown of 5% or more at least once each year, yet historically, markets have delivered positive returns approximately 75% of the time in the 12 months following a bear market bottom.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Disclosures

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance is no guarantee of future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

A word on risk

All investments carry a certain degree of risk, including possible loss of principal, and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-U.S. investments involve risks such as currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. This report should not be regarded by the recipients as a substitute for the exercise of their own judgment. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group