Fisher Investments recently wrote an interesting article asking whether corporate stock buybacks affect markets. Here is their conclusion:

“Yes and no? Stocks move on supply and demand. Stock buybacks, where a company buys and takes shares off the market, theoretically reduce supply. They can also raise earnings per share, thus rewarding shareholders. So, all else equal and on paper, stock buybacks are bullish. But reality, as always, is more complicated. Buybacks are just one factor affecting supply. There are others, and demand matters, too. They may not reduce supply if they merely offset secondary issuances, like employee stock awards. Often, buybacks merely ‘sterilize’ new issuance. Other negative (or less bullish) fundamental factors might matter more in pricing, lowering demand even as supply shrinks. So buybacks are a factor, but not the factor.“

While the statement is mostly correct, I am unsure they looked at the actual impact that corporate stock buybacks have on the market. We have discussed this topic and the past misstatements of corporate stock buybacks. Here is a listing for more background.

- They are not a return of capital to shareholders; dividends are.

- Corporate stock buybacks are the worst use of cash.

-

It is a benefit that almost entirely benefits corporate insiders.

But, without rehashing the many problems of corporate stock buybacks, let’s focus on these transactions’ impact on the overall market.

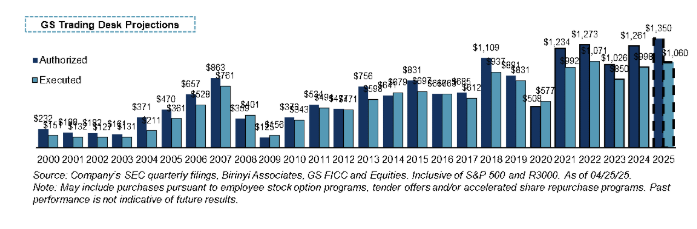

As of May 2025, corporate stock buyback authorizations are on track to eclipse $1.35 trillion this year, with more than $1 trillion executed. This will exceed any other year in the market since the turn of the century. Such should be unsurprising with Apple (AAPL) announcing an additional $100 billion and Google adding another $70 billion to their programs (those two programs will account for 12% of the total alone).

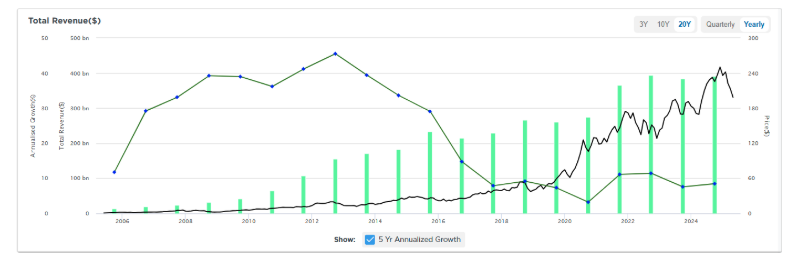

The data should lead one to question why corporate stock buybacks have grown steadily since the turn of the century. Such is particularly the case when the overreliance on buybacks at non-accretive valuations to boost stock prices has become commonplace. Such a statement undermines the fallacy that corporate stock buybacks are solely a return of capital to shareholders. For example, Apple’s $110 billion buyback plan in 2024 raised questions among some investors about whether the company focused too much on immediate stock price increases rather than on investments that could drive long-term value. That statement should not be overlooked, given that 5-year annualized revenue growth has been flat since 2018. (Chart courtesy of SimpleVisor.com)

If corporate stock buybacks are not a significant factor in increasing stock prices, why do companies engage in them so heavily? Why not just let market dynamics carry the load? The reason is simplistic to understand.

“Corporate executives give several reasons for stock buybacks but none of them has close to the explanatory power of this simple truth: Stock-based instruments make up the majority of their pay and in the short-term buybacks drive up stock prices.” – Financial Times.

So, how much of a factor are buybacks?

Are Buybacks An Important Factor

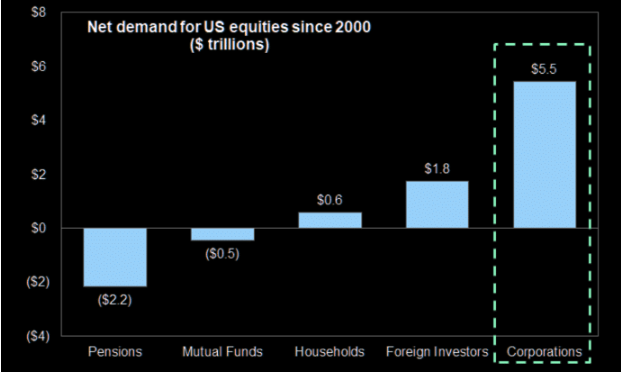

It is a pretty easy task to see whether or not corporate stock buybacks influence stock prices. As we penned last year, the impact of buybacks extends beyond individual companies. Since 2000, net corporate buybacks have accounted for 100% of the equity market’s net asset purchases—a reflection of the diminished participation from pensions, mutual funds, and individual investors:

-

Net Flow: +$5.2 trillion

-

Pensions & Mutual Funds: –$2.7 trillion

-

Households & Foreign Investors: +$2.4 trillion

-

Corporations (Buybacks): +$5.5 trillion

In other words, without corporate stock buybacks, the stock market would be roughly 30% lower today.

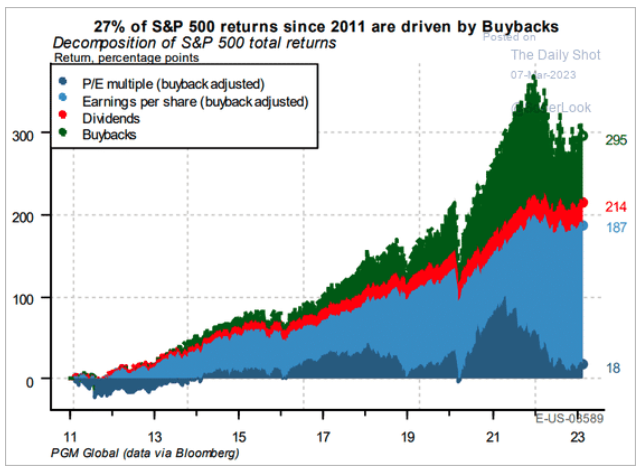

“The chart below via Pavilion Global Markets shows the impact stock buybacks have had on the market over the last decade. The decomposition of returns for the S&P 500 breaks down as follows:“

- 6.1% from multiple expansions (21% at Peak),

- 57.3% from earnings (31.4% at Peak),

- 9.1% from dividends (7.1% at Peak), and

- 27% from share buybacks (40.5% at Peak)

Yes, buybacks are that important.

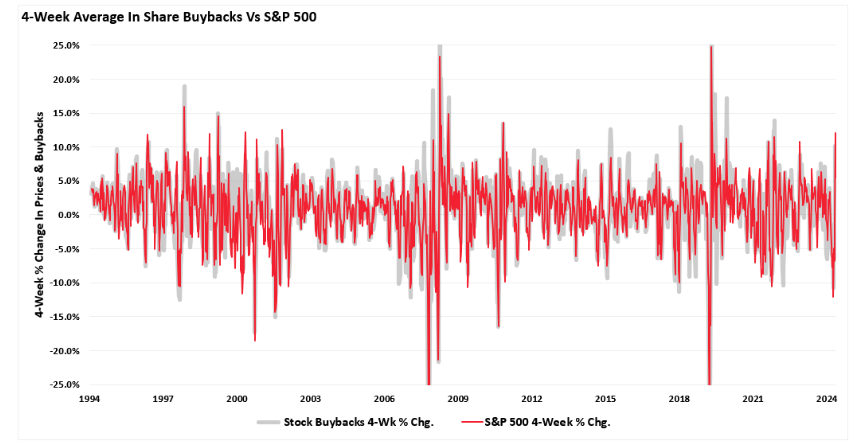

However, to Fisher’s question directly, there is more than just a minor correlation between corporate stock buybacks and the market. The chart below overlays the 4-week change in stock buybacks versus the 4-week change in the S&P 500 index. It is worth noting that before 1982, the SEC considered share buybacks an illegal form of market manipulation. (In 1982, the SEC adopted Rule 10b-18, which provided “safe harbor” from “liability of market manipulation. In other words, the SEC recognizes that buybacks manipulate the financial markets but provided a “shield” to corporations.)

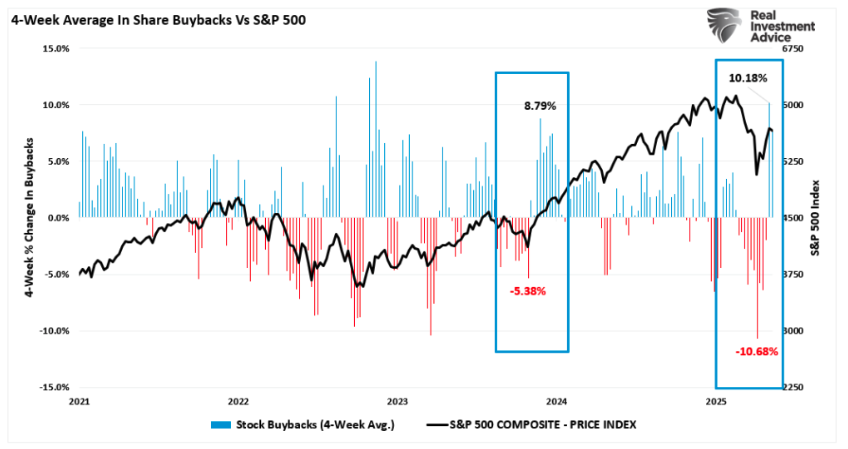

The chart above is complex due to the large amount of data. The chart below is from 2021 to present, where changes to buybacks (increase or decrease) significantly impact changes to stock prices. It is worth noting that the nearly 20% decline in April was exacerbated by the sharp reversal in buyback activity and vice versa.

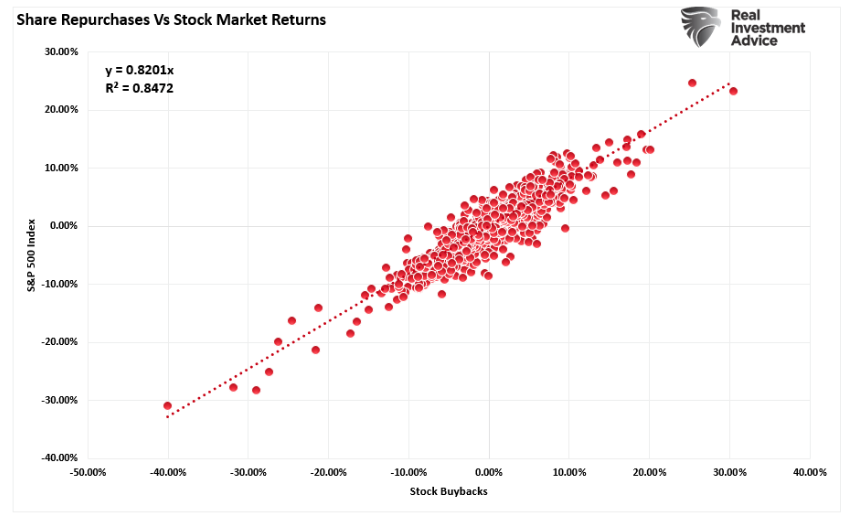

While Fisher suggests that buybacks have little to do with market movements, a high correlation exists between the 4-week percentage change in buybacks and the stock market. More importantly, since the act of share repurchases provides a buyer for those shares, the .85 correlation between the two suggests this is more than just a casual relationship.

But yes, Fisher is correct, other factors support higher asset prices.

Buybacks Affect More Than Just Prices

In 2023, Jason Zweig penned an article for the WSJ stating:

“Over the past five years, according to S&P Dow Jones Indices, big U.S. companies have spent $3.9 trillion repurchasing their own stock. Buybacks are neither bad nor good. They are simply a tool. Just as you can use a hammer either to build a house or knock one down, buybacks are useful in the right corporate hands and dangerous in the wrong ones.“ – Jason Zweig, WSJ

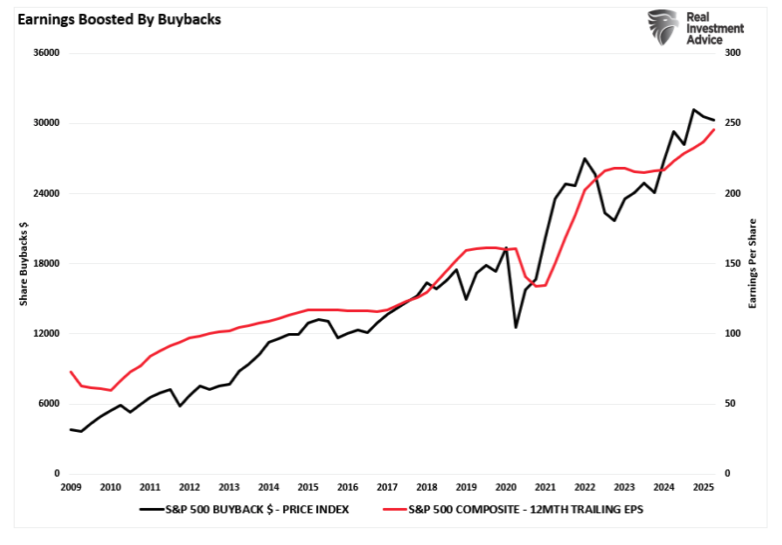

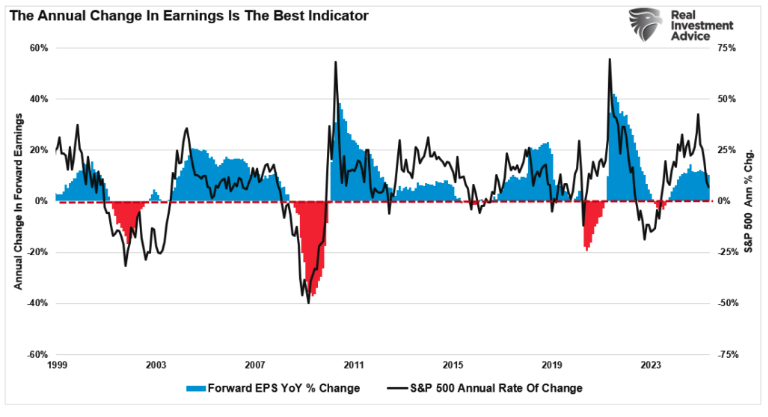

That is a fair statement. The impact of share buybacks is vital to manufacturing earnings growth since we measure earnings on a per-share basis. In other words, if you reduce the number of shares outstanding, corporate earnings “per share” improve, as shown below.

As discussed previously, the annual rate of change in earnings growth is one of the best predictors of forward stock market returns.

However, investors must be cautious about understanding the impact of buybacks on earnings when investing in companies. As Warren Buffett noted:

Finally, an important warning: Even the operating earnings figure we favor can easily be manipulated by managers who wish to do so. Such tampering is often considered sophisticated by CEOs, directors and their advisors. Reporters and analysts embrace its existence as well. Beating ‘expectations’ is heralded as a managerial triumph. That activity is disgusting. It requires no talent to manipulate numbers: Only a deep desire to deceive is required. ‘Bold, imaginative accounting,’ as a CEO once described his deception to me, has become one of the shames of capitalism.“

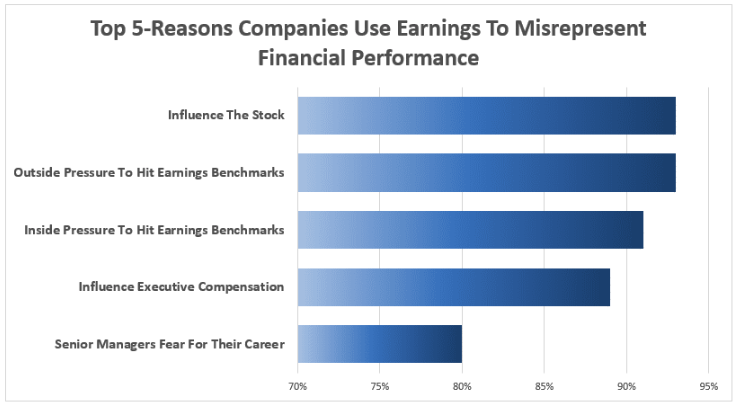

Why would CEO’s want to manipulate earnings? Unsurprisingly, a WSJ survey of CFOs found that 93% pointed to “influence on stock price” and “outside pressure” as the reasons for manipulating earnings figures.

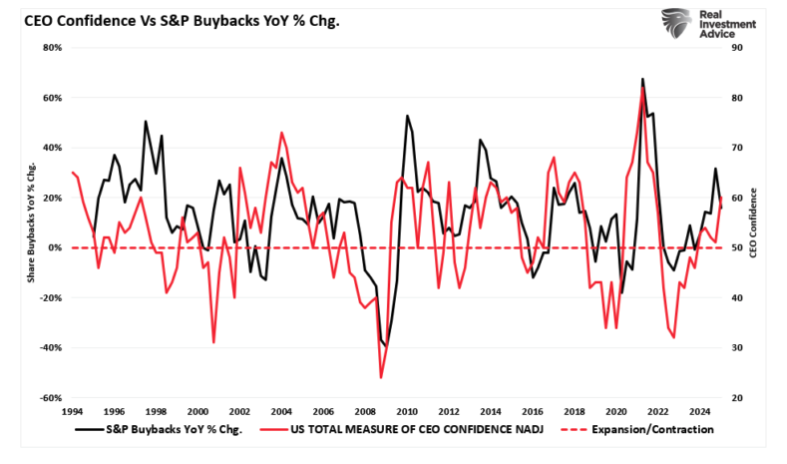

Of course, one misnomer is that corporate CEOs execute buybacks when they believe the stock is undervalued. However, the reality is quite the opposite, and they tend to execute share repurchases when their current optimism is elevated. When share prices decline, and buybacks could be done at accretive prices, there is little incentive to do so.

Conclusion

The evidence is clear: corporate stock buybacks are not a marginal force in markets—they are central to the mechanics of price inflation. When buybacks account for the entire net demand for equities over the last two decades, it’s hard to argue they’re simply “a” factor. They aren’t just reducing supply on paper—they are the demand. Without them, equity valuations would look very different.

But what’s more concerning is the why. Despite the popular narrative that buybacks return capital to shareholders, the data and behavior of corporate management tell a different story. Buybacks overwhelmingly inflate earnings per share and boost short-term stock prices, which are tied directly to executive compensation. That incentive skews the timing and intent of buyback programs away from long-term value creation and toward short-term financial engineering.

To Fisher’s credit, markets are complex. Demand, sentiment, interest rates, and macroeconomic factors all matter. However, dismissing buybacks as one variable among many overlooks just how much they dominate equity flows. Their influence is measurable, intentional, and reinforced by corporate leadership’s financial incentives.

The question for investors is not whether buybacks matter—they do. The question is whether they’re being used to create real value or mask its absence.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Real Investment Advice

Read more commentaries by Real Investment Advice