On the M&A front, Ambarella (AMBA) shares jumped over 19% on June 24 on news of exploring a potential exit. The company represents an attractive target for firms seeking automotive and drone application expansion in computer vision. For reference, over 50% of ROBO constituents are small- and mid-caps, which are increasingly attractive partners or acquisitions to larger players. Both ROBO and THNQ include AMBA.

Global Industrial Reshoring & Infrastructure Buildout

We also covered global reshoring efforts, particularly across data centers and industrial sectors for sovereign independence. Since then, we’ve seen over $100B in semiconductor and data center commitments emerge, alongside new European collaborations from ROBO constituents.

At NVIDIA’s Paris GTC conference, several key partnerships materialized:

Schneider Electric (SBGSY) announced a collaboration with NVIDIA to develop AI-ready infrastructure. This collaboration will target power, cooling, and high-density rack systems for next-generation AI factories across Europe. SGBSY is included in ROBO.

Nebius Group (NBIS) delivered the first NVIDIA Blackwell general availability in Europe, offering B200 capacity on-demand through their self-service platform and NVIDIA DGX Cloud. NBIS is included in THNQ.

Supermicro (SMCI) launched European support for their complete NVIDIA AI Factory Stack, expanding manufacturing capabilities across the region. SMCI is included in THNQ.

Innovation & Valuation Opportunities in Established Robotics Companies

Speaking of Europe, long-time ROBO member Hexagon (HXGBY) perfectly illustrates our third webcast theme. The company, which describes itself as one that “measures the world and shapes the future,” recently surprised the industry with a major announcement. Known historically for precision measurement tools in industrial applications, the company unveiled its newest product:AEON, a wheeled humanoid robot.

Image Source: Hexagon Robotics

Catch the official launch:

Sweden-based HXGBY is projected to generate over $6 billion in revenue and $1 billion in profit for 2025. The company’s three largest business segments include: manufacturing intelligence (36% of revenue), geosystems (29%) and asset life cycle intelligence (15%), with the majority of revenue from EMEA (~33%), followed by USA (~30%) and Asia (~14%).

When Market Fear Creates Opportunity

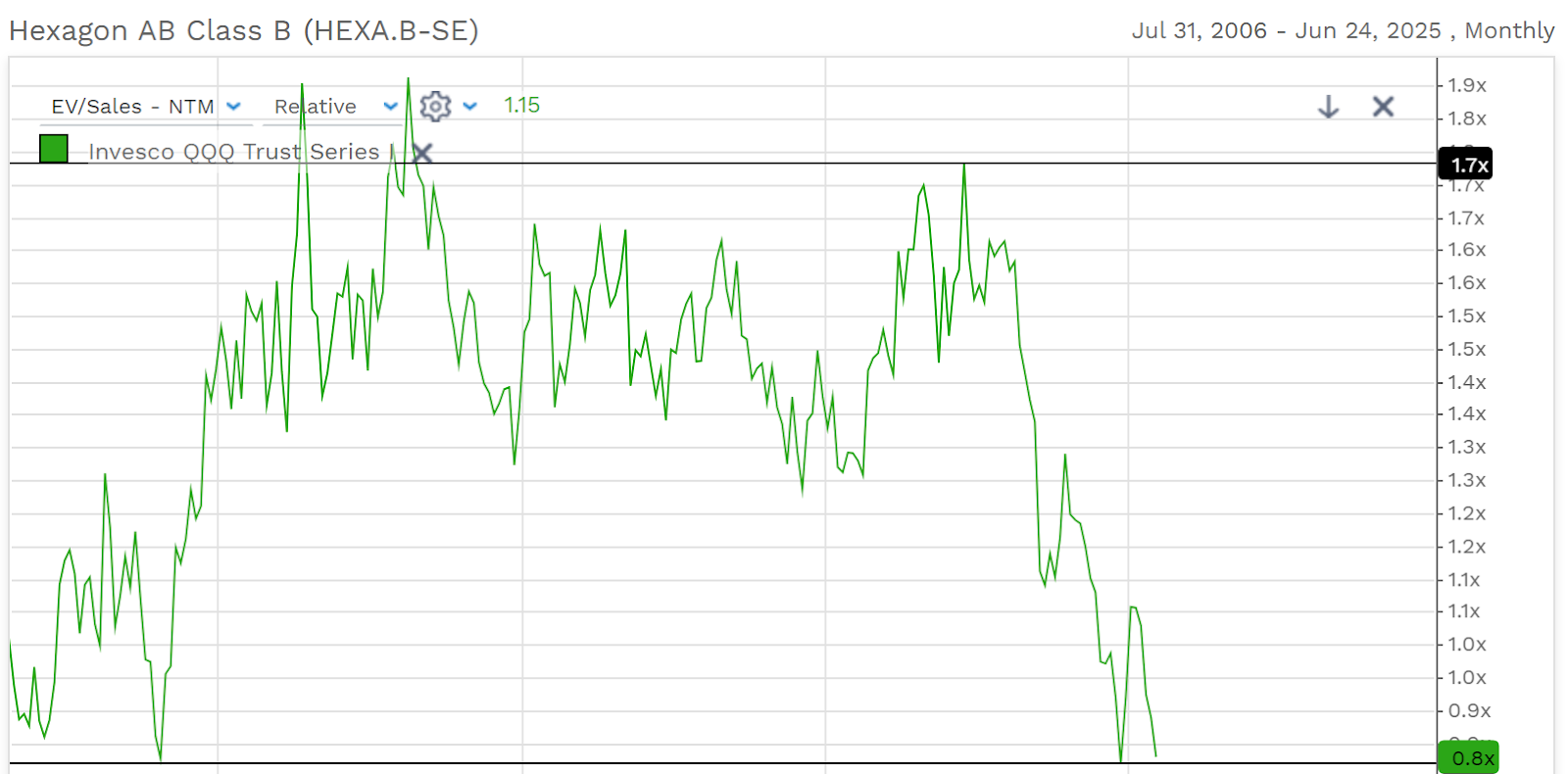

Despite Hexagon’s success, global footprint, exposure to multiple industrial cycle opportunities, and their new humanoid robotics launch, the company trades at attractive valuations:

4.7x projected 2025 EV/Sales

Just under 20x projected 2025 P/E ratio

Currently at 10-year relative valuation lows

Chart: FactSet, June 2025 – Relative NTM EV/Sales compared to NASDAQ 100, at lowest relative levels since the financial crisis, now trading at a discount versus historical premium.

HXGBY exemplifies just one of many publicly-traded robotics companies trading well below historical averages. These companies haven’t experienced the valuation hype-premium seen in private markets or artificial intelligence, creating significant opportunities.

Sovereign AI’s Importance

Our research shows that current valuation discrepancies stem primarily from investor fears around tariffs and geopolitics, which have temporarily delayed several projects. However, the bigger picture shows accelerated commitments both in the U.S. and globally, as sovereign supply chains for energy and AI become increasingly critical.

“Sovereign AI is an imperative – no company, industry or nation can outsource its intelligence,” stated NVIDIA CEO Jensen Huang earlier this month.

This dynamic creates compelling entry points for investors in established robotics companies with proven business models and expanding AI capabilities.

Catch the replay of the webinar, “The dynamic trends shaping robotics, AI, and healthcare” here.

Looking for regular updates? Subscribe here for weekly insights on robotics, AI, and healthcare technology, delivered straight to your inbox.

ROBO is the underlying index for the ROBO Global Robotics & Automation ETF (ROBO), the L&G ROBO Global Robotics and Automation UCITS ETF (ROBO.LN), and the Global X ROBO Global Robotics & Automation ETF (ROBO.AU). THNQ is the underlying index for the ROBO Global Artificial Intelligence ETF (THNQ) and the L&G Artificial Intelligence UCITS ETF (AIAI).

VettaFi is the index provider for the ROBO ETF and THNQ ETF, for which it receives an index licensing fee. However, the ROBO ETF and THNQ ETF are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi and its affiliates have no obligation or liability in connection with the issuance, administration, marketing, or trading of theROBO ETF and THNQ ETF.