As we sit at the midway point of 2025, we expect the global economy to continue expanding, but at a slower pace. Tariffs are likely to weigh on growth and boost inflation, though the impact should be less damaging than that of the inflation episode of 2022. Given this landscape, we think investors should consider modestly overweight exposure to risk assets.

A Downshift to Moderate Economic Growth

Changes in US trade policy challenged markets last quarter, but the global economy is still expanding despite some slowing in the US. Household and business sentiment, which fell sharply when tariffs were initially announced, seems to be on the mend as the outlook clears. Manufacturing remains weaker than services but is above post-pandemic lows.

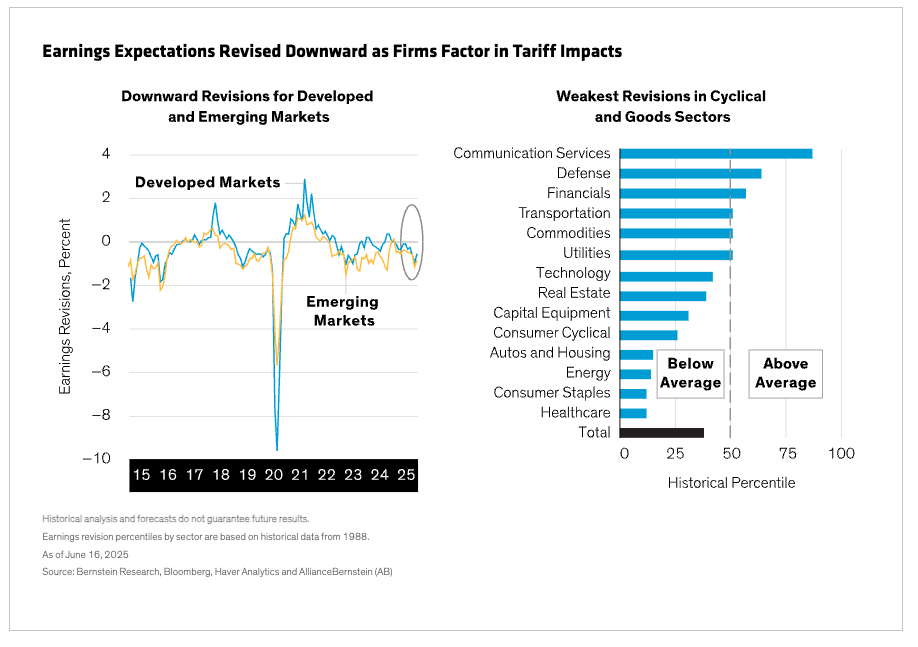

Corporate earnings expectations were marked down meaningfully as importers factored in the impact of wide-ranging tariffs on their businesses (Display, left). Cyclical and goods sectors—those likely to bear the brunt of a trade war—experienced the sharpest downward revisions (Display, right).

Despite the weaker sentiment across households and businesses, end demand has remained broadly resilient. While US household consumption slowed somewhat in the first half, robust real wage growth and continued job creation are underpinning strong spending power in the US and the EU. US household spending has slowed year over year but has been partly offset by improving momentum elsewhere in the world.

Corporate spending also seems to be holding up. Yes, weak business confidence is weighing on the capital spending plans of manufacturers and smaller firms. However, this softness has been mostly offset by robust US technology investment, thanks to continued spending on AI.

Fiscal and Monetary Policies Recalibrate

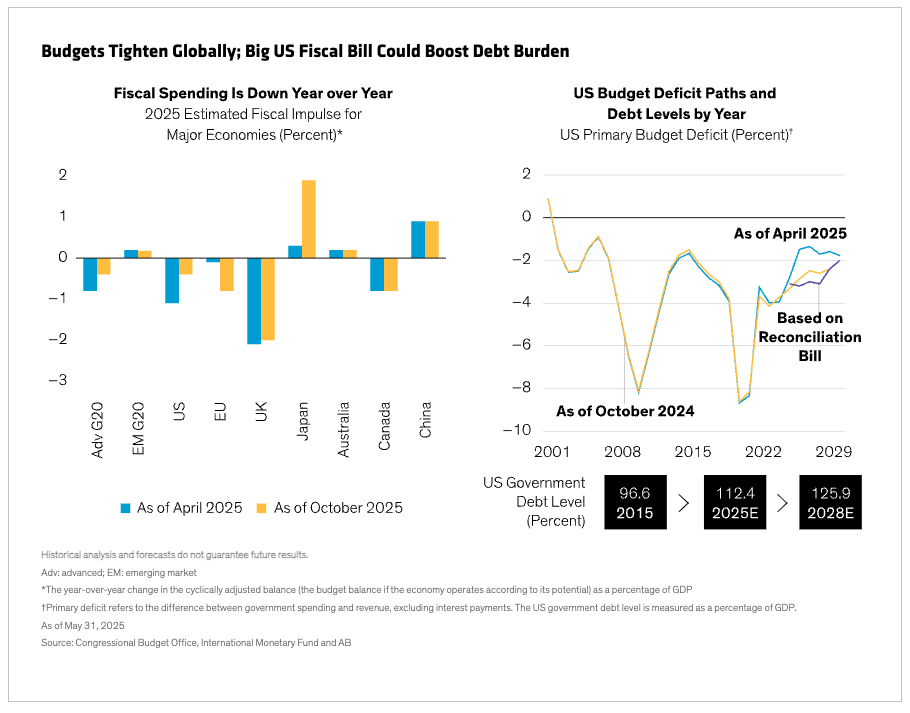

Considering that tariffs can be viewed as a form of tax, recent US trade policies have made the fiscal stance more contractionary (Display, left). The “One Big Beautiful Bill” Act has yet to be finalized, but judging from provisions as of this writing, we expect fiscal gains from tariffs to be mostly offset, returning the US budget deficit’s trajectory to its pre-tariff course from October 2024 (Display, right). This is a clear negative for fiscal sustainability but a positive for near-term growth. In our view, it’s likely to temper tariffs’ drag.

Inflation has continued to moderate gradually, but we’re watching to see the full pass-through impact of higher tariffs. Average three-month run rates across developed markets are 2.5%, with the US, Canada and EU closer to the 2% target. Policy interest rates, historically speaking, remain restrictive in most major markets, giving central banks the flexibility to respond to slower growth or start cutting again as the impacts of tariffs peak.

Consider Modest Equity Overweight

In this environment, we think investors should consider overweighting developed market equities, tilting to the US, Japan and Europe. The reasons: We expect steady US consumer spending and continued growth in tech investment. In Europe, household spending patterns are improving and fiscal spending on defense and infrastructure is substantial.

For more defensive markets and those heavily exposed to commodities, such as those of Canada and the UK, we think an underweight is warranted. When it comes to emerging market equities, a neutral positioning seems called for, given China’s secular growth prospects and overcapacity in manufacturing, creating extra supply that has compressed corporate earnings.

Neutral View on Credit and Interest-Rate Risk

Investors should consider targeting greater balance between high-yield credit and equity allocations. Credit rallied when sentiment around tariffs improved, but spreads have declined and are approaching their long-term median levels. If they were to decline further, we think it would make sense to source more of a portfolio’s risk exposure from equity than from credit, especially if leverage is a concern.

We think the current economic picture argues for a neutral position on government bond exposure. Central bank policy rates remain high and inflation trends have been favorable, but the Federal Reserve seems likely to remain on hold with further rate cuts until the full effects of the new tariffs become visible in economic data.

Among developed market currencies, the US dollar seems likely to weaken as economic growth differences between it and its peers seem likely to narrow going forward. We think the euro looks relatively appealing: it should benefit from improving domestic consumption in that region.

Looking at the Big Picture

To sum things up, we see a backdrop of moderate economic growth ahead. Corporate earnings expectations have discounted the likely direct impacts of tariffs, which—based on our assessment—should pale in comparison to the 2022 stagflation episode. If tariff impacts prove to be a one-off, as we expect, earnings growth should accelerate again toward its historical mid-cycle averages. This landscape calls for muti-asset investors to stay flexible when pursuing select diversification opportunities.

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams, and are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein