Key takeaways

- We believe tariffs remain the key risk to corporate profits in the second half of the year and is less concerned about geopolitical events or the outlook for fiscal and monetary policy.

- Credit trends and market breadth appear to support the market bulls' thesis that the current advance is both healthy and sustainable while inflation expectations remain well anchored, which should keep Treasury yields rangebound.

- While more neutral on the near-term outlook for equities due to tariff uncertainty and valuations, we believe multiple catalysts could drive an earnings acceleration in 2026 as current risks are likely to dissipate.

US stocks near fair value amid tariff complacency

After two outsize positive performance years in 2023 and 2024, US equity markets are digesting a mixed bag of risks and opportunities in 2025. While the second quarter saw increased volatility from concerns over the impact of tariffs on economic growth and inflation, markets quickly dismissed those concerns, rallying back to all-time highs. In our opinion, the US stock market currently stands near fair value, lacking material upside in the short run and vulnerable to potential negative surprises in the second half of the year. We are more focused on the outlook in 2026 when multiple catalysts could drive an acceleration in corporate profits and many of the current risks are likely to dissipate.

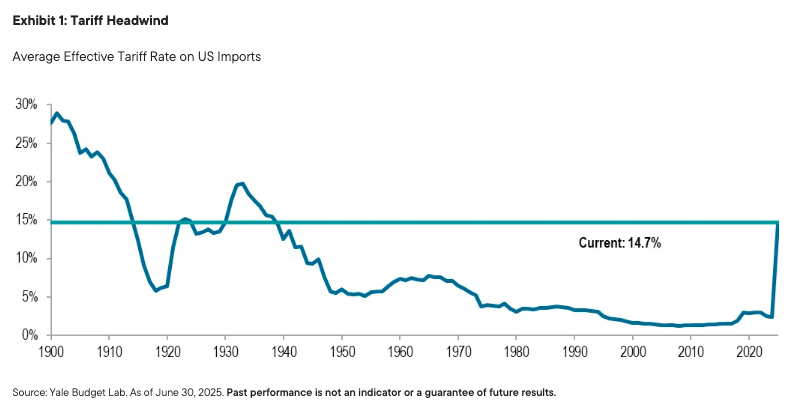

We believe tariffs remain the key risk to corporate profits in the second half of the year and are less concerned about geopolitical events or the outlook for fiscal and monetary policy. While the tariff deal deadline has been extended, there has been slow progress beyond a few broad deal “frameworks” announced. Tariffs on our biggest trading partners in the European Union and China are likely to stay high and take longer to resolve, while tariffs on secondary trading partners will remain in place for extended periods. To date, the impact on both growth and inflation has been muted by existing inventory and a fear of backlash for raising prices. However, conversations with corporate management teams tell us that while they are willing to absorb some costs and prices are likely to rise in the coming months as pre-tariff inventory is absorbed. We estimate that the average effective tariff rate will ultimately settle in the 14%–15% range from approximately 2.5% in the prior year (Exhibit 1).

While the overall economy can absorb that impact without recession, we believe that current profit estimates are too high and likely to weaken. Earnings estimate revisions are likely to begin declining more significantly starting in the fall. Housing, autos and investment spending excluding artificial intelligence (AI) are all weakening and should become more pronounced in the months ahead.

Fortunately, inflation expectations to date remain well anchored and, while higher tariffs are likely to lead to higher goods inflation, lower oil prices and a slowing housing market should help to offset those pressures, keeping 10-year Treasury yields rangebound. Longer term, Treasury yields remain a risk for equity investors as concerns about higher deficits are real and worrisome. So far, the market has been willing to look past those concerns as rising deficits from the One Big Beautiful Bill (OBBB) won’t be visible to investors for some time.

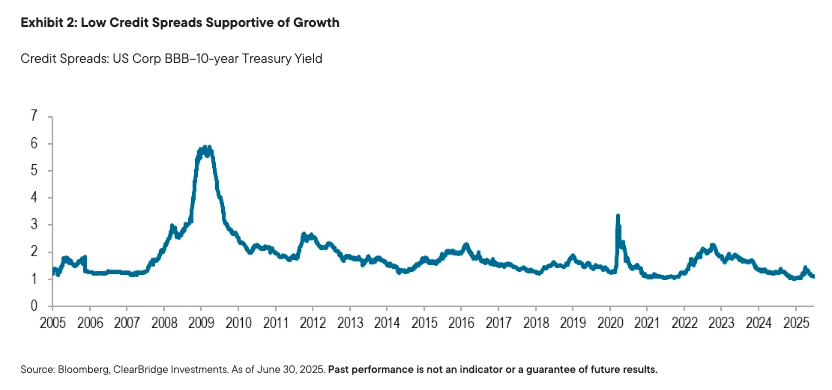

Despite our near-term caution, we acknowledge that credit trends and market breadth appear to support the bull thesis that the current advance is both healthy and sustainable. Bond spreads, historically a good measure of expectations for future financial distress, remain tight and supportive of growth. Current market breadth, or the level of participation of stocks in the market advance, is sufficiently broad. Finally, leadership in sectors like technology, industrials and financials looks indicative of a strong and resilient market outlook.

While we are more neutral on the near-term outlook for equities based on tariff uncertainty and valuations, we are more bullish on the outlook for 2026, when we believe that S&P 500 Index profits can return to double-digit growth. Our expectations assume a broader resolution of most tariff negotiations resulting in more of a one-time price adjustment than a lasting impact on both prices and profits. We expect continued strong investment in all things related to AI, but also in other industries as deregulation boosts investment and capital markets activity resumes amid declining corporate uncertainty. Finally, we expect both monetary stimulus from lower Federal funds rates in the next year, and fiscal stimulus from the front-loaded impact of the OBBB to support profit growth.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Equity securities are subject to price fluctuation and possible loss of principal. Large-capitalization companies may fall out of favor with investors based on market and economic conditions. Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

US Treasuries are direct debt obligations issued and backed by the “full faith and credit” of the US government. The US government guarantees the principal and interest payments on US Treasuries when the securities are held to maturity. Unlike US Treasuries, debt securities issued by the federal agencies and instrumentalities and related investments may or may not be backed by the full faith and credit of the US government. Even when the US government guarantees principal and interest payments on securities, this guarantee does not apply to losses resulting from declines in the market value of these securities.

Read more commentaries by ClearBridge Advisors