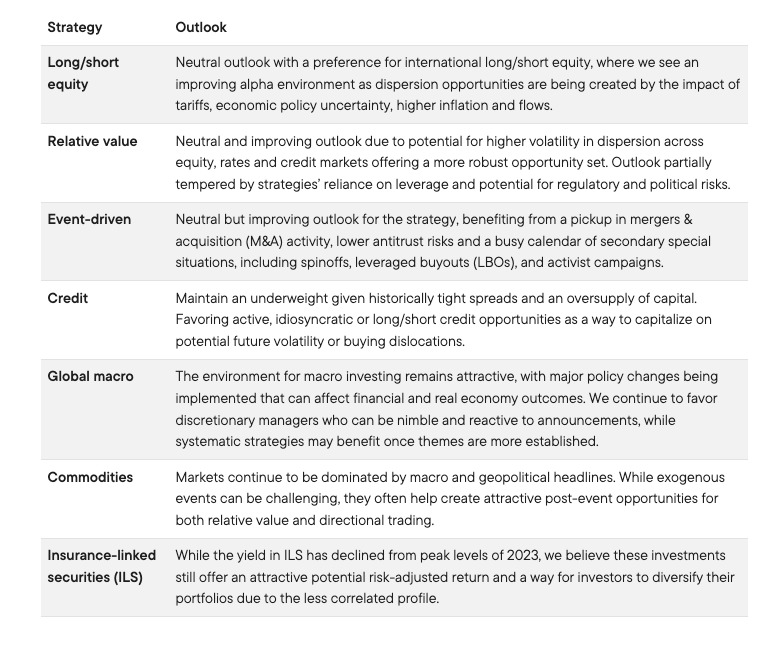

Hedge Fund Strategy Outlook: Third Quarter 2025

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAmid market uncertainty, geopolitical tensions, and President Trump’s transactional orientation and propensity to change his goals, we believe the outlook for hedge fund strategies remains constructive. Heightened dispersion and constrained liquidity are creating compelling opportunities for dynamic, market-neutral and nimble investment approaches.

Strategy highlights

- Commodities: Managers may find attractive trading opportunities in market dislocations brought on by macro and geopolitical headlines.

- Discretionary global macro: A combination of factors is driving the US dollar weaker, with broad implications for global markets.

- International long/short equity: Improving alpha opportunities outside the United States will be influenced by dispersion resulting from geopolitical realignments, varying sensitivities to tariffs and divergent central bank policies.

Macro themes we are discussing

Last quarter, we described the investment environment as one defined by elevated economic uncertainty, rising geopolitical tensions, stretched valuations and tight credit spreads. Today, both uncertainty and geopolitical risk have arguably softened a bit. While valuations have gotten more stretched, we are not yet seeing signs of distress—Warren Buffett (retired) is sitting heavily in cash, the Chicago Board Options Exchange's CBOE Volatility Index (VIX) is below 17 and credit markets remain mostly orderly as Wall Street is beginning to offload to retail investors in the private markets.

There are differing views on the drivers of this shift. Some point to the return of US President Trump and the resurgence of market “animal spirits,” others to a broader reordering of the global system as described by Ray Dalio, and still others to the mounting burden of global debt. Regardless of the cause, we anticipate continued market volatility and dispersion, sporadic liquidity during unexpected news events, Trump tweets and the potential for positioning flows to drive markets.

For hedge fund investors and managers, this environment presents both meaningful opportunity and heightened risk. The tails to both the upside and downside are expected to be fatter than previously experienced over the last five years. We expect to see greater divergence in manager performance—even within the same sector—driven by increased volatility. In our view, success in this environment will require portfolios that are diversified, liquid, opportunistic and patient.

Q3 2025 outlook: Strategy highlights

Commodities

Commodities are often quick to react to major macro events, and this has been especially evident this year with oil price volatility around the US tariff announcements in April and the Israel-Iran conflict in June. Bursts of volatility, most notably when driven by an unexpected catalyst, can be a risk to trading strategies, but they are often also a source of opportunity as news is digested and interpreted over time. Large price dislocations are often accompanied by temporary shifts within commodity term structures or across different related commodities. Should macro headlines continue to create these types of dislocations, commodity-focused hedge funds may be able to identify attractive relative value and directional trading opportunities.

Exhibit 1: Oil Prices Have Trended Lower with Volatility in 2025

Price of Brent Crude Oil

December 31, 2024 to June 30, 2025

Source: Bloomberg. Important data provider notices and terms available at www.franklintempletondatasources.com.

Discretionary global macro

The US dollar has trended weaker in recent months, driven lower by a combination of factors related to domestic and international policies, as well as a broad reassessment of popular US exceptionalism narratives. Some currencies, like the Taiwanese dollar, have seen dramatic moves as foreign investors rethink their FX hedging policies or future portfolio allocation decisions. To the extent that this weaker dollar trend persists, macro managers may find opportunities not just in currency momentum but also across developed and emerging markets as well as other asset classes. As with any significant move in major macro markets, there could be risks and opportunities around dislocations or unexpected outcomes—a potentially rich environment for macro-driven traders and investors.

Exhibit 2: The US Dollar Has Weakened Vs. Foreign Currencies

DXY Index Return

December 31, 2022 to June 26, 2025

Source: Bloomberg. The DXY index measures the value of the US dollar against a basket of foreign currencies. Important data provider notices and terms available at www.franklintempletondatasources.com.

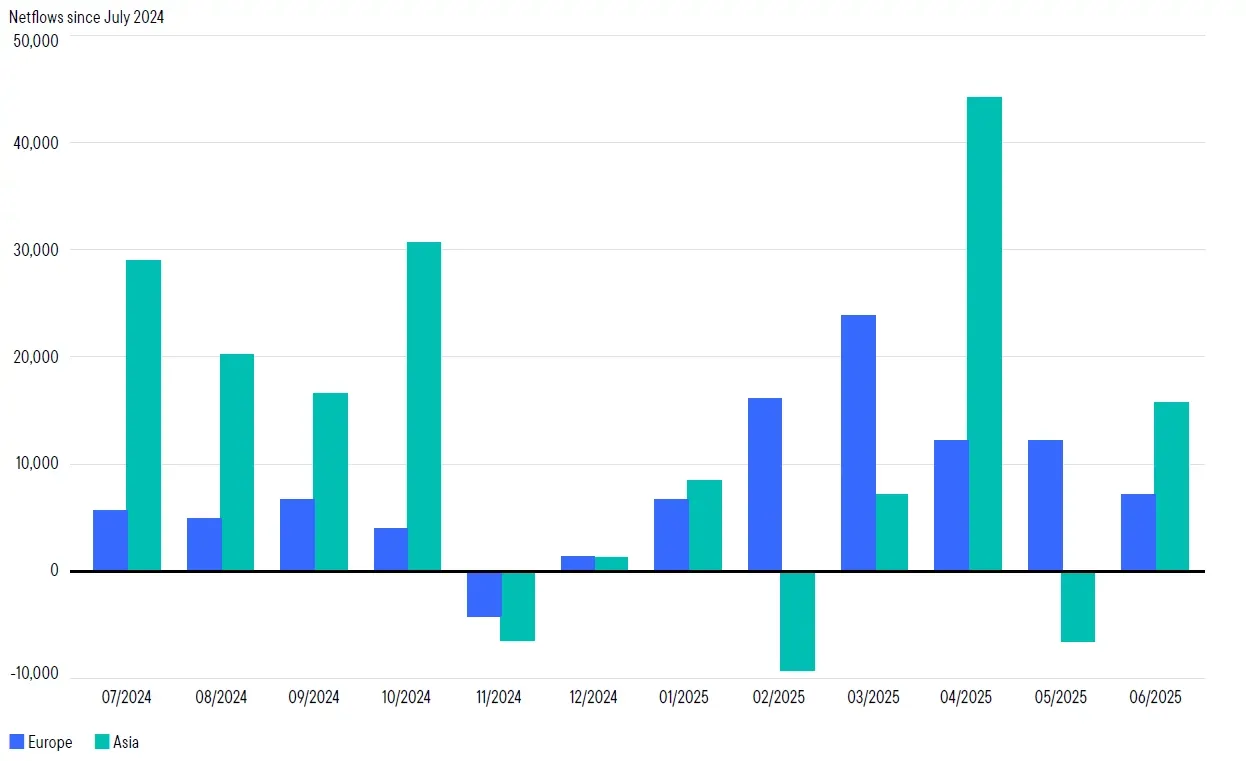

International long/short equity

We are in a market environment increasingly driven by macro events, including geopolitical tensions, trade policy shifts, divergent fiscal and monetary paths and inflation concerns. These dynamics contribute to greater dispersion, especially outside of the United States, where geopolitical realignments and divergent monetary policies result in shifting flows. While concerns over US equity valuations and waning US exceptionalism are leading flows abroad—creating a beta tailwind for international long/short equity strategies—the more compelling case lies in the alpha opportunity. Dispersion is being fueled by correlation breakdowns, divergent tariff sensitivities, sectoral realignments and disparate fiscal responses. As global capital is reallocated, flows should not only reflect market sentiment but should also actively drive dispersion, creating alpha opportunities. International markets, shaped by uncertainty and surprises, offer fertile ground for skilled managers to capture alpha through active positioning in a fragmented global landscape.

Exhibit 3: Europe and Asia Equity Net Flows

July 31, 2024 to June 30, 2025

Source: Bloomberg. Important data provider notices and terms available at www.franklintempletondatasources.com.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. The allocation of assets among different strategies, asset classes and investments may not prove beneficial or produce the desired results. Some subadvisors may have little or no experience managing the assets of a registered investment company. International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Derivative instruments can be illiquid, may disproportionately increase losses, and have a potentially large impact on performance.

Equity securities are subject to price fluctuation and possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default. Currency management strategies could result in losses to the fund if currencies do not perform as expected.

Commodity-related investments are subject to additional risks such as commodity index volatility, investor speculation, interest rates, weather, tax and regulatory developments. Short selling is a speculative strategy. Unlike the possible loss on a security that is purchased, there is no limit on the amount of loss on an appreciating security that is sold short. Investments in companies engaged in mergers, reorganizations or liquidations also involve special risks as pending deals may not be completed on time or on favorable terms. Liquidity risk exists when securities or other investments become more difficult to sell, or are unable to be sold, at the price at which they have been valued.

Active management does not ensure gains or protect against market declines.

WF: 6122277

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All