Given short-term and long-term price implications, the growth trajectory for copper could be electrifying. The industrial metal’s usage in electricity is giving way to its ubiquity.

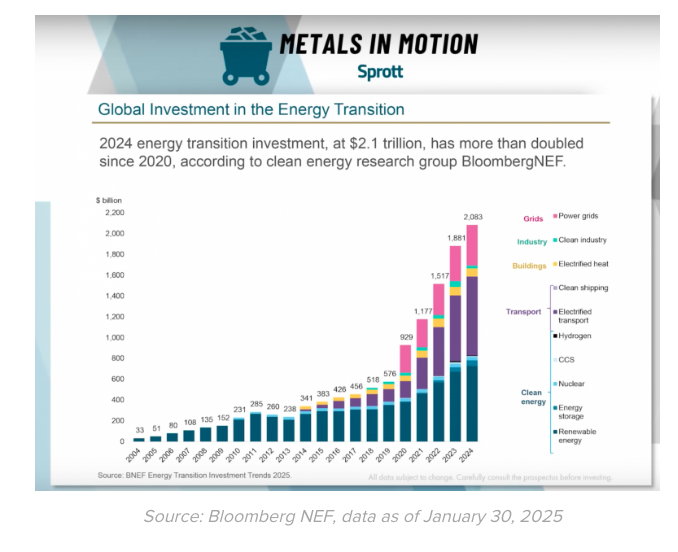

As the world relies more heavily on electricity to power day-to-day devices, cars, and a swathe of other applications, the need for copper will only intensify. Global investment into alternative energy has already been growing at a fever pitch. At the center of this growth is electricity, which is translating into higher demand for copper.

“Anywhere we see electricity needing to be transmitted, you’ll find copper,” noted Steven Schoffstall, director of ETF product management at Sprott Asset Management, in an interview with ETFguide.

“It’s the second most conductive metal behind silver, but it’s much more cost effective than silver,” Schoffstall added, confirming that’s why “you see copper being more demand in applications than silver.”

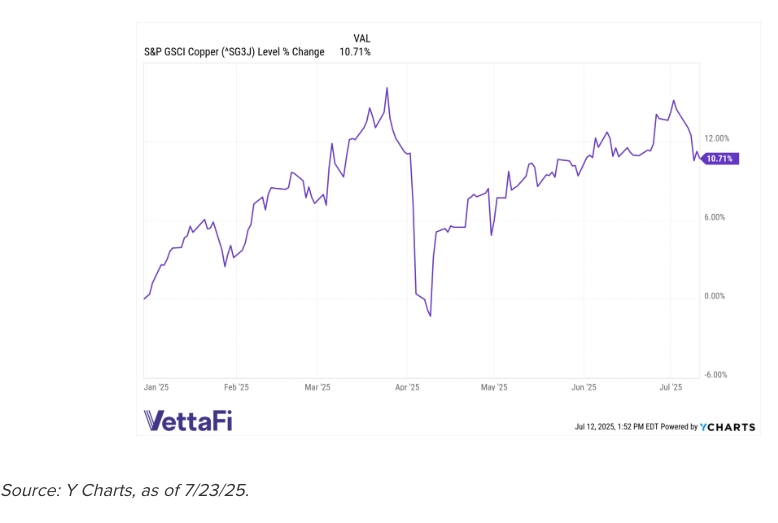

Rising copper prices have translated into a nice recovery for the S&P GSCI Copper Index. It’s recovering from April’s tariff tantrum and could keep climbing if short-term and long-term factors continue working in the metal’s favor.

The Standard & Poor’s Goldman Sachs Commodity Index Copper is a sub-index of the S&P GSCI that serves as a publicly available benchmark for investment performance in the copper commodity market.

Short-Term Price Catalysts

Tariffs continue to be central to today’s market news. Copper, in particular, could see short-term price momentum work in its favor as U.S. president Donald Trump has earmarked August 1 as the day to implement tariffs on the industrial metal.

The news shouldn’t come as too much of a surprise, as President Trump was already eyeing copper as a potential tariff target. In February, the president ordered a Section 232 investigation into copper imports and their effect on national security.

Given that investigations have now translated into actual tariffs, this could have suppliers scrambling to purchase copper at a quickened pace. This could certainly push up prices in the short-term, but there are also long-term factors that could continue to spur prices even higher.

Long-Term Price Implications

The easy answer to meet rising copper demand is to simply mine for more and create more copper mines. If only it was that easy.

When looking at data from ING, S&P Global, and Statista, the average lead time to build a new copper mine (from discovery to production) is 21 years.

Needless to say, a lot goes into building a mine. There’s the prospecting and exploration necessary to find a suitable location to build a mine. Furthermore, getting the necessary licenses to build a copper mine can be an arduous task in and of itself. This could mire the prospective copper mine producer in bureaucratic red tape. Then, finally, development and extraction can take place.

Needless to say, the demand for copper is increasing. Meanwhile, trying to supply that demand adequately can seem like trying to fit a square peg in a round hole. It can be done, but one needs aspirin nearby to alleviate the ensuing headaches.

All that said, this is disconcerting news for electricity consumers. However, it’s an opportune time for copper investors.

One Fund for Copper Exposure

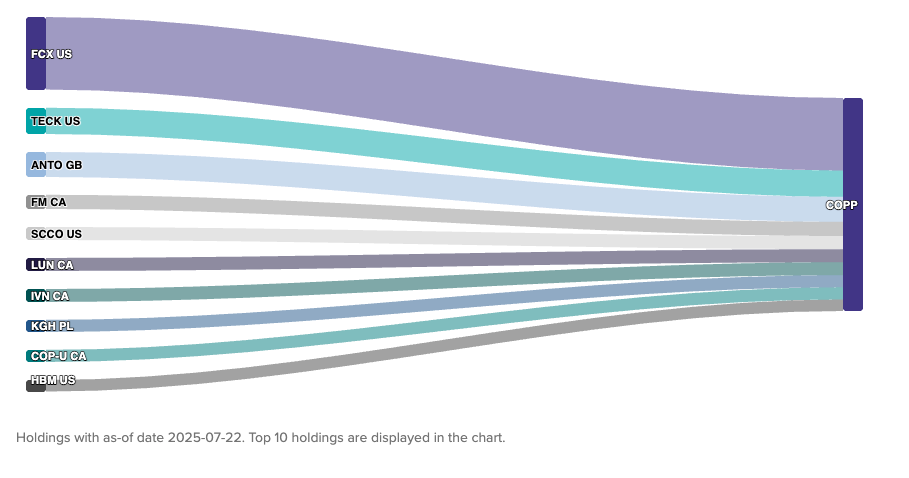

Consider a fund that provides blanket exposure to copper. This includes copper miners and copper itself. It’s all available in the Sprott Copper Miners ETF (COPP).

COPP already featured mining exposure as an indirect play on prices. Now, it includes physical copper in the fund, which can track copper spot prices more closely. The addition of physical copper was implemented last month, giving investors the opportunity to attain that mining/physical copper combination now.

An investor should consider the investment objectives, risks, charges, and expenses carefully before investing. To obtain a Prospectus, which contains this and other information, contact your financial professional or call 888.622.1813. Read the Prospectus carefully before investing, which can also be found by clicking one of the links below.

Past performance is no guarantee of future results. One cannot invest directly in an index.

Funds that emphasize investments in small/mid-cap companies will generally experience greater price volatility. Diversification does not eliminate the risk of investment losses. ETFs are considered to have continuous liquidity because they allow an individual to trade throughout the day. A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses, affect the Fund’s performance.

Sprott Asset Management USA, Inc. is the Investment Adviser to the ETFs. ALPS Distributors, Inc. is the Distributor for the ETFs and is a registered broker-dealer and FINRA Member. ALPS Distributors, Inc. is not affiliated with Sprott Asset Management USA, Inc. or VettaFi.