Room to Run in Local Currency EM Debt

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEmerging markets (EM) local currency debt posted strong returns in the second quarter, building on momentum from earlier in the year. Gains were broad based, driven largely by currency appreciation against the U.S. dollar and supported by declining local rates. While volatility picked up at times, resilient growth, easing inflation, and high real yields continue to support a constructive outlook. Below, we highlight our largest active positions across countries and explain the thinking behind them.

Local Currency: Prepared to Withstand Instability

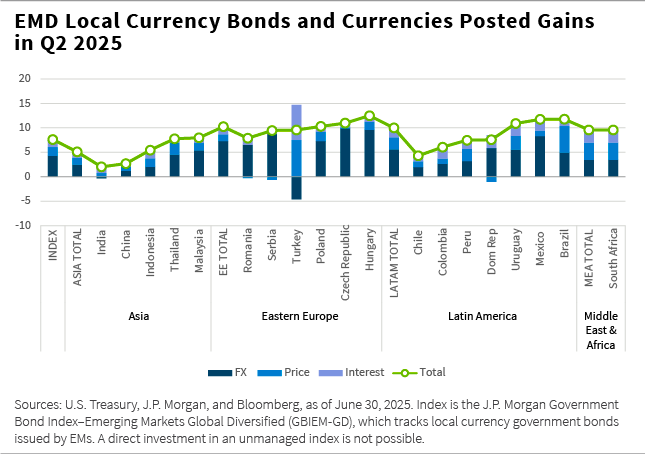

First, however, let’s look back at the quarter. As Marcelo Assalin, head of our emerging market debt team, explained in his mid-year outlook, the quarter had a volatile start, but in local markets, strong momentum from the first quarter continued. Gains in both rates and foreign exchange (FX) accelerated through the second quarter.

The J.P. Morgan Global Bond Index-Emerging Markets Global Diversified (GBIEM-GD) returned 7.62%, of which more than 4% resulted from EM currency appreciation against the U.S. dollar. Bonds also performed well, gaining 1.8% in price terms, with yields declining by an average of 29 basis points (bps) across the index.

With the exception of some relative underperformance in Asia (+5.1%), variation in the other regions was minimal, all converging on the +10% level.

We continue to see opportunities in the EM local currency space, where currency valuations appear attractive and real interest-rate differentials versus developed markets are high.

In our opinion, growth has held up well despite trade-related headwinds, and inflationary pressures have eased. Our outlook is that there will be additional cuts from EM central banks to further support the asset class. Local currency bonds should also benefit from the weakening U.S. dollar trend.

While we have positioned the portfolios anticipating a period of higher volatility, we have a constructive medium- and long-term outlook for EM debt and believe the asset class is fundamentally well prepared to withstand a period of instability.

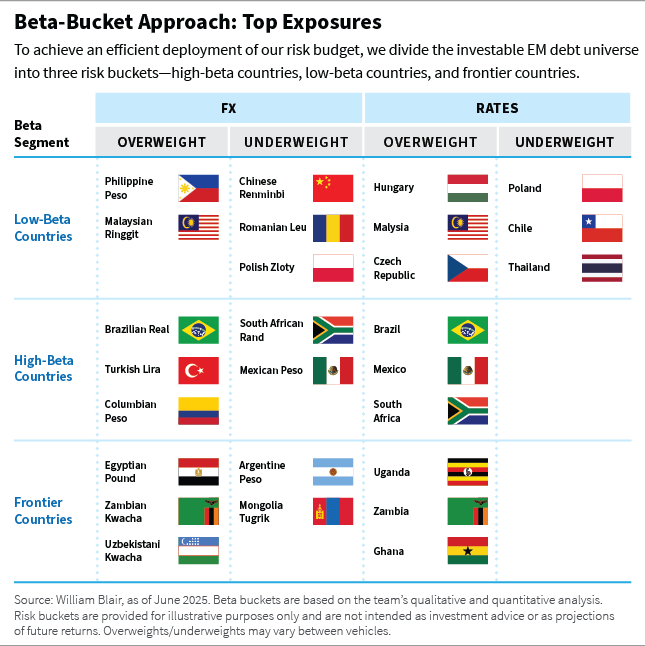

Below, we break down some of our largest active positions by beta bucket, which is how we allocate our risk budget.

Low-Beta Bucket Highlights

Hungary: Our duration overweight was primarily in a green bond. We find real rates attractive, and while they’re now closer to terminal levels, the central bank remains one of the region’s most progressive. A renewed European focus on excessive deficit targets could help contain Hungary’s fiscal deficit, even as defense spending rises.

Malaysia: We remain overweight the ringgit. Economic growth is holding up, driven by private consumption, and fiscal consolidation is underway. While the currency outperformed last year, it still looks undervalued on a trade-weighted basis. We’re also overweight duration, given benign inflation and the central bank’s room to cut rates if trade uncertainty weighs on growth.

Czech Republic: We believe the central bank still has room to ease policy, even with rates already low relative to peers. Its cautious stance has helped keep the inflation outlook benign.

Poland: We are underweight the zloty on valuation concerns and expect some reversal of its 2024 strength. We’re also underweight rates, given a less supportive political backdrop for fiscal consolidation.

Chile: In Chile, we remain underweight the local curve in favor of higher-yielding regional peers. The peso has strengthened and copper prices are boosting external balances, but rising inflation is eroding real rates. With several cuts already priced in, there’s limited room for further curve flattening.

Thailand: In Thailand, we are underweight duration due to unattractive valuations. While rate cuts are priced in, financial stability concerns may limit the central bank’s willingness to deliver them.

Philippines: In the Philippines, we are overweight the peso as lower oil prices are improving terms of trade. We believe strong remittance growth and easing inflation have given the central bank room to cut rates and support the economy.

China: In China, we are underweight the renminbi due to uncertainty around U.S. tariffs and trade policy. Although the central bank has managed volatility through currency fixing, the renminbi has weakened on a trade-weighted basis.

Romania: In Romania, we are underweight the leu due to concerns over twin deficits, especially in an election year. The ruling coalition has yet to deliver a credible fiscal plan, and we view the currency as overvalued, which undermines regional competitiveness and contributes to a wide current account deficit.

High-Beta Bucket Highlights

Brazil: In Brazil, local assets have continued to outperform as the central bank nears peak rates. With a 15% nominal rate and inflation expectations around 4.5%, Brazil offers one of the highest real rates in the index after Turkey, supporting portfolio inflows as investors trim U.S. dollar exposure. We believe growth remains solid and is set to benefit further from upcoming rate cuts.

Mexico: In Mexico, we remain overweight bonds, expecting further inflation convergence with the United States to compress the 5% Mbono-Treasury spread. We also see room for rate cuts beyond the 50-bps cut already priced in, which could support bond performance.

South Africa: In South Africa, we moved overweight rates following what we saw as an overdone sell-off tied to the budget delay. With the budget now passed, we expect curve flattening, with the long end poised to benefit from attractive relative valuations.

Turkey: In Turkey, despite rising political volatility, the reform agenda remains on track, supporting improvements in the current account and FX reserves. We believe high yields continue to overcompensate investors for currency risk, and the central bank’s emergency rate hike may renew interest in local bonds.

Colombia: In Colombia, we’ve trimmed our bond exposure to a smaller overweight but remain long the peso. The macro backdrop is more challenging than in some peers, but the currency still offers attractive carry and is supported by a weaker dollar. We also believe oil prices have bottomed after Middle East tensions eased, which should bolster sentiment.

Frontier Bucket Highlights

Uganda: In Uganda, we remain constructive on local currency assets and express this view through longer-dated bonds, supported by attractive real rates. We recently removed our partial currency hedge, reflecting greater confidence in the fundamentals backing the exchange rate.

Zambia: In Zambia, we maintain our long bond position, expecting further disinflation in 2025 to support performance. While the central bank may stay hawkish amid short-term global risks, we see potential for the local yield curve to bull steepen.

Ghana: In Ghana, we remain constructive on rates given a favorable technical and fundamental backdrop. Limited bond supply and disinflation have supported local currency bonds, and we view high real rates to remain supportive. Following strong currency gains, we’ve moved to hedge our FX exposure.

Egypt: In Egypt, we remain constructive on the Egyptian pound carry trade amid lighter foreign positioning and easing regional tensions. The market’s resilience during periods of risk aversion has reinforced our confidence in the current monetary and exchange rate framework.

Uzbekistan: In Uzbekistan, we hold an out-of-benchmark position supported by high gold prices and a recovering Russian ruble. Gold is a key driver of reserves and fiscal revenue, while a stronger ruble—given Russia’s role as a major trading partner—helps ease pressure on Uzbekistan’s competitiveness.

Argentina: In Argentina, we remain underweight the peso despite high interest rates, as the currency has appreciated sharply in real terms. The government has prioritized stability ahead of fourth-quarter elections, but rising overvaluation, a terms-of-trade shock, and weakening external accounts may force a policy shift sooner.

Mongolia: In Mongolia, we are underweight the tugrik as lower coal prices are expected to weigh on export revenues. With the economy heavily reliant on commodities, weaker prices typically pressure fiscal and external balances. Despite stabilization efforts, the tugrik may face further depreciation given its rich valuation and deteriorating terms of trade.

Lewis Jones, CFA, FRM, is a portfolio manager on William Blair’s emerging markets debt team.

Want more insights on the economy and investment landscape? Subscribe to our blog.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

This content is for informational and educational purposes only and not intended as investment advice or a recommendation to buy or sell any security. Investment advice and recommendations can be provided only after careful consideration of an investor’s objectives, guidelines, and restrictions.

Information and opinions expressed are those of the authors and may not reflect the opinions of other investment teams within William Blair Investment Management, LLC, or affiliates. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information is current as of the date appearing in this material only and subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material may include estimates, outlooks, projections, and other forward-looking statements. Due to a variety of factors, actual events may differ significantly from those presented.

Investing involves risks, including the possible loss of principal. Equity securities may decline in value due to both real and perceived general market, economic, and industry conditions. The securities of smaller companies may be more volatile and less liquid than securities of larger companies. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks. These risks may be enhanced in emerging markets and frontier markets. Different investment styles may shift in and out of favor depending on market conditions. Individual securities may not perform as expected or a strategy used by the Adviser may fail to produce its intended result.

Investing in the bond market is subject to certain risks including market, interest rate, issuer, credit, and inflation risk. Rising interest rates generally cause bond prices to fall. High-yield, lower-rated, securities involve greater risk than higher-rated securities. Sovereign debt securities are subject to the risk that an entity may delay or refuse to pay interest or principal on its sovereign debt because of cash flow problems, insufficient foreign reserves, or political or other considerations. Derivatives may involve certain risks such as counterparty, liquidity, interest rate, market, credit, management, and the risk that a position could not be closed when most advantageous. Diversification does not ensure against loss. The inclusion of Environmental, Social and Governance (ESG) factors beyond traditional financial information in the selection of securities could result in a strategy's performance deviating from other strategies or benchmarks, depending on whether such factors are in or out of favor. ESG analysis may rely on certain values based criteria to eliminate exposures found in similar strategies or benchmarks, which could result in performance deviating.

Collective Investment Trusts (CITs) are available to qualified retirement plans. For non-U.S. citizens or residents, William Blair offers a series of Luxembourg-domiciled SICAV products.

There can be no assurance that investment objectives will be met. Any investment or strategy mentioned herein may not be appropriate for every investor. References to specific companies are for illustrative purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future returns.

Privacy & Security | Cookie Policy | Social Media Disclaimer | FINRA’s BrokerCheck | Glossary

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits