Stay Long Tech and Growth

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- While the tech sector experienced weakness in 1Q25 in anticipation of a global trade war, the recent rebound in the second quarter proves that there is value in the sector’s longer-term secular trends, namely AI, software, semiconductors and power generation.

- As the U.S. economy proves resilient and names within the sector continue to trade within a reasonable range from a valuation standpoint, Russ advocates adding to select names in the space during late summer’s historical period of seasonal weakness.

Tech and the broader growth style had a rough first quarter. The weakness did not last. Since early April investors have, once again, reverted to a tech bias. On a one and three-month basis, technology is the top performing sector. I believe growth, tech and AI-related themes can continue to lead in the back-half of 2025.

I would focus on three reasons why tech and related names can continue to outperform: a supportive macro backdrop, elevated but not unreasonable valuations and earnings momentum.

From a top-down perspective the early spring sell-off hurt crowded positions, momentum and any stock that carried excess risk, i.e. high beta. In contrast it rewarded less volatile, slow growth, stable companies that were perceived to be more resilient in the event of a trade war. As we have gained more clarity on tariffs, and more importantly, more confidence in the economy’s resilience, investors have rotated back into longer-term secular themes, notably artificial intelligence (AI), software, semiconductors and power generation.

My assumption is that the market, while still vulnerable to trade-related headline risks, will operate in a somewhat calmer atmosphere during the second half. Growth is likely to slow but the U.S. should avoid a recession. At the same time, price pressures associated with tariffs have proved modest and inflation has, thus far, been (mostly) contained. This should help keep long-term rates range-bound, as they have been for most of the year. An environment of positive but slow growth and stable rates should support growth over value, which, by contrast, has historically tended to perform best during periods when growth is accelerating.

From a valuation standpoint, while tech is not cheap, valuations are within range. According to data from Bloomberg, the tech heavy Nasdaq 100 is trading 25x FY1 estimates and 22x FY2. Based on price-to-earnings ratios, the Russell 1000 growth index trades for approximately 1.8x the value index. Relative valuations are right around the five-year average and down from the post-pandemic peak of 2x.

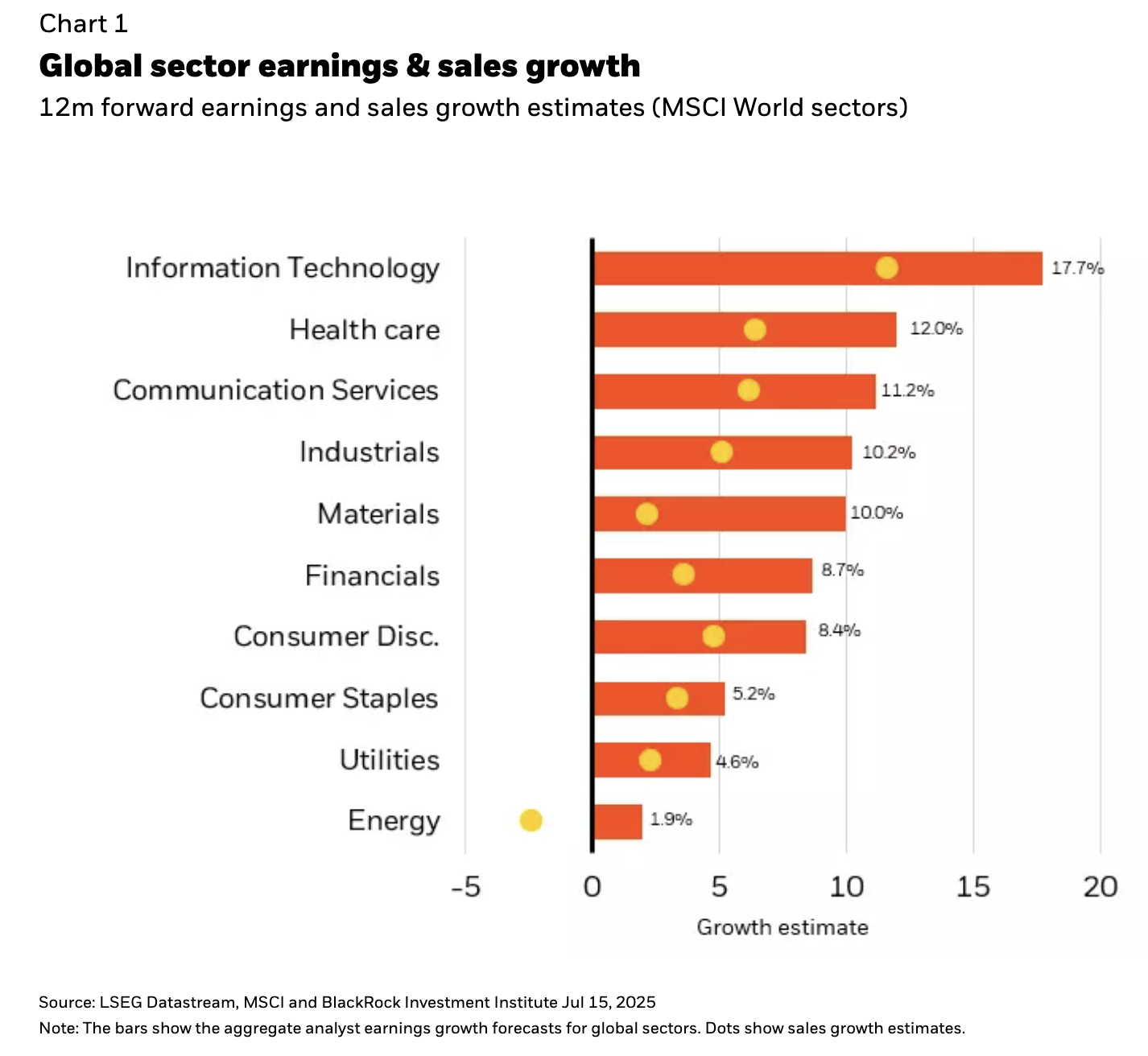

Elevated growth valuations are arguably justified based on profitability, margins and still stellar earning growth. We continue to live in a world in which mega-cap tech companies remain remarkably profitable, and despite large capital-spending plans, capable of driving strong earnings growth. On a global basis, the MSCI World tech sector is expected to lead the rest of the market in both earnings and sales growth (see Chart 1).

After a huge run, I doubt whether tech stocks are likely to move up in a straight line. Many of the top names are up 50% or more from the April lows. We are also entering a seasonally weaker period for stocks. That said, rather than trim excessively, I would use any late summer weakness to add to core positions in AI-related themes, software and communications. Looking out 6-12 months, I believe these names have the potential for further gains.

Russ Koesterich, CFA, JD, Managing Director and portfolio manager, is a member of the Global Allocation team as well as the lead portfolio manager on the GA Selects model portfolio strategies.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

To obtain more information on the fund(s) including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month end, please click on the fund tile.

The Morningstar RatingTM for funds, or "star rating", is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure (excluding any applicable sales charges) that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

A significant portion of the aggregate world gold holdings is owned by governments, central banks and related institutions. One or more of these institutions could sell in amounts large enough to cause a decline in world gold prices. Should there be an increase in the level of hedge activity of gold producing companies, it could cause a decline in world gold prices. Should the speculative community take a negative view towards gold, it could cause a decline in world gold prices.

Principal Risks: The fund is actively managed and its characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Non-investment grade debt securities (high yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities. Asset allocation strategies do not assure profit and do not protect against loss. Short selling entails special risks. If the fund makes short sales in securities that increase in value, the fund will lose value. Any loss on short positions may or may not be offset by investing short sale proceeds in other investments. The fund may use derivatives to hedge its investments or to seek to enhance returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility.

International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks often are heightened for investments in emerging/developing markets or in concentrations of single countries.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of July 2025 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

The BlackRock Model Portfolios are provided for illustrative and educational purposes only, do not constitute research, investment advice or a fiduciary investment recommendation from BlackRock to any client of a third party financial advisor (each, a "Financial Advisor"), and are intended for use only by such Financial Advisor as a resource to help build a portfolio or as an input in the development of investment advice from such Financial Advisor to its own clients and shall not be the sole or primary basis for such Financial Advisor’s recommendation and/or decision. Such Financial Advisors are responsible for making their own independent fiduciary judgment as to how to use the BlackRock Model Portfolios and/or whether to implement any trades for their clients. BlackRock does not have investment discretion over, or place trade orders for, any portfolios or accounts derived from the BlackRock Model Portfolios. BlackRock is not responsible for determining the appropriateness or suitability of the BlackRock Model Portfolios or any of the securities included therein for any client of a Financial Advisor. Information and other marketing materials provided by BlackRock concerning the BlackRock Model Portfolios –including holdings, performance, and other characteristics –may vary materially from any portfolios or accounts derived from the BlackRock Model Portfolios. Any performance shown for the BlackRock Model Portfolios does not include brokerage fees, commissions, or any overlay fee for portfolio management, which would further reduce returns. There is no guarantee that any investment strategy will be successful or achieve any particular level of results. The BlackRock Model Portfolios themselves are not funds. The BlackRock Model Portfolios, allocations, and data are subject to change.

For financial professionals: BlackRock’s role is limited to providing you or your firm (collectively, the “Advisor”) with non-discretionary investment advice in the form of model portfolios in connection with its management of its clients’ accounts. The implementation of, or reliance on, a Managed Portfolio Strategy is left to the discretion of the Advisor. BlackRock is not responsible for determining the securities to be purchased, held and sold for a client’s account(s), nor is BlackRock responsible for determining the suitability or appropriateness of a Managed Portfolio Strategy or any securities included therein for any of the Advisor’s clients. BlackRock does not place trade orders for any of the Advisor’s clients’ account(s). Information and other marketing materials provided to you by BlackRock concerning a Managed Portfolio Strategy—including holdings, performance and other characteristics–may not be indicative of a client’s actual experience from an account managed in accordance with the strategy.

For investors: BlackRock’s role is limited to providing your Advisor with non-discretionary investment advice in the form of model portfolios in connection with its management of its clients’ accounts. The implementation of, or reliance on, a Managed Portfolio Strategy is left to the discretion of your Advisor. BlackRock is not responsible for determining the securities to be purchased, held and sold for your account(s), nor is BlackRock responsible for determining the suitability or appropriateness of a Managed Portfolio Strategy or any securities included therein. BlackRock does not place trade orders for any Managed Portfolio Strategy account. Information and other marketing materials provided to you by BlackRock concerning a Managed Portfolio Strategy—including holdings, performance and other characteristics—may not be indicative of a client’s actual experience from an account managed in accordance with the strategy. This material is subject to change.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2025 BlackRock, Inc. or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USRRMH0825U/S-4699950

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All