As the Federal Reserve (Fed) conducts its quinquennial review of monetary policy, it must recognize the severe shortcomings of its current policy framework. Since the advent of quantitative easing in 2008, the federal funds rate, a benchmark for trillions of dollars of short-term credit, is no longer guided by market forces. This diminishes the effectiveness of Fed policy and destabilizes long-term rates.

Currently, the fed funds rate is set by the interest rate paid on bank reserves. This administered rate is determined by the “best guess” of members of the Federal Open Market Committee (FOMC), often relying on imprecise and dated releases of economic data. It replaces the market rate set by the demand and supply of bank reserves, a regime which determined the fed funds rate through most of the post-World War II era.

In this former “scarce reserve regime,” the Fed transacted in the reserve market on almost a daily basis, undertaking open market purchases and sales in order to add and subtract reserves and thereby maintain the fed funds rate within a target range. If the Fed’s trading desk found the fed funds rate trading persistently above target, this signaled that the FOMC should consider raising the rate target. Conversely, when the rate persistently fell short of target, this was a signal that the demand for credit was weak, prompting the Fed to lower its target.

But since the great financial crisis, all this has changed. Quantitative easing raised the level of reserves far above requirements, pushing the fed funds market into a chronic state of excess reserve supply (called the “ample reserve regime.). In this regime, the fed funds rate is not determined by the market, but by the interest rate that the Fed pays on reserves, a right granted by Congress in 2009.

Increased Rate Volatility

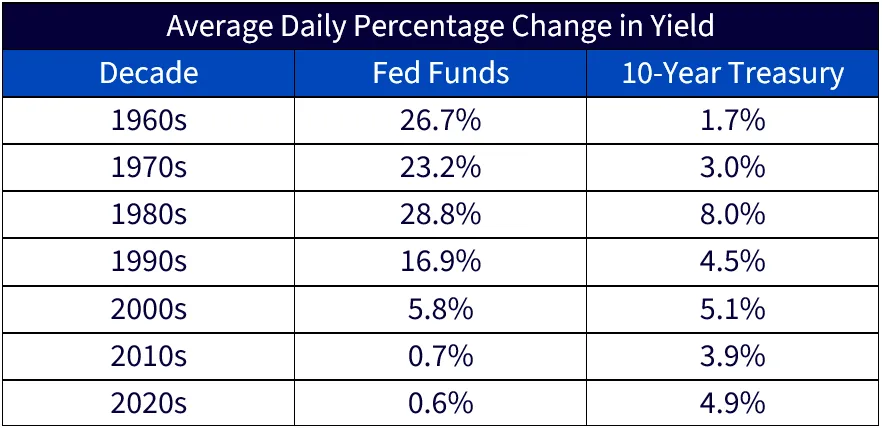

One of the negative consequences of this new regime is that short-term rates have become rigid while the volatility of long-term interest rates has increased. The accompanying chart shows the average daily fluctuations of the fed funds rate and yield on the 10-year treasury over the past seven decades. Except for the volatile 1980s, which saw persistent double-digit inflation, the trend of the fluctuations of the fed funds rate is sharply lower, while the fluctuations in the long-term bond have shown little change and are actually up over the last decade.

Sources: WisdomTree, Bloomberg

This is not the way interest rates are supposed to behave. Throughout history, short-term rates have been more volatile than long-term rates and have served as the shock-absorber to shifts in the credit market. Today, with short rates fixed, all the adjustments to the changing economic outlook are forced onto longer rates. It is the case of the tail wagging the dog.

Without market guidance, the Fed chooses a funds rate that it hopes will lead to full employment and stable prices. But this response is too slow. For example, in 2021, while the Fed was debating the “temporary” nature of inflation, the demand for credit was increasing at a record pace. Had the scarce reserve regime been in place, the Fed would have quickly seen the upward pressure on the funds rate, prompting them to raise interest rates much earlier. Market-based prices invariably move before lagged and imperfect government data.

Solution

The Fed goal should be to bring back the scarce reserve regime, reduce the interest it pays on reserves, and swing the central bank back to profitability. Given the bloated size of the Fed’s balance sheet and trillions of dollars of excess reserves, this goal requires an innovative approach.

If interest rates on current reserves are set back to zero, banks would use their excess reserves to buy short-term treasuries, sending these and other short-term credit rates plummeting and sparking an inflationary surge in borrowing and money creation. On the other hand, to mop up all the excess reserves would require the massive and rapid sale of trillions of dollars government bonds from the Fed’s bloated portfolio, which would disrupt the bond market.

One way the Fed could gain the advantages of the scarce reserve regime is by both raising reserve requirements to restore reserve scarcity while setting the interest rate that the Fed pays on reserves to some fixed level, say 2 percentage points, below the targeted fed funds rate. Such a policy would resurrect the funds market as an indicator of short-term credit conditions, cut interest payments to the banks, and restore the Fed to profitability.

The Fed could offset the revenue loss to the banks by relaxing many of the regulatory reforms instituted since the great financial crisis. In 2010, the Bank for International Settlements estimated that losses from unnecessary regulations reach $100 billion a year, a level that is undoubtedly much higher today. With higher reserve requirements, the Fed should relax capital requirements (as they began to do last month), modify restrictions on proprietary trading, and level the playing field with other non-bank lenders and fintech firms. These reforms could more than make up for the banks’ loss of interest on reserves.

The Fed cannot just tinker with its current system. It is time to bring back market-determined short-term interest rates, stabilize the long-term rate, and wean the banks from holding high-yielding, non-productive reserves.

Jeremy J. Siegel

Emeritus Professor of Finance, The Wharton School of the University of Pennsylvania

Senior Economist, WisdomTree

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Past performance is not indicative of future results. You cannot invest in an index. Professor Jeremy Siegel is a Senior Economist to WisdomTree, Inc. and WisdomTree Asset Management, Inc. This material contains the current research and opinions of Professor Siegel, which are subject to change, and should not be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. The user of this information assumes the entire risk of any use made of the information provided herein. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.