More defined contribution (DC) plan sponsors have adopted lifetime income solutions to improve their participants’ retirement outcomes, but we believe there are still too many holdouts. Part of the issue stems from misconceptions about how practical the solutions are as well as their risks, costs and flexibility. Here’s our perspective on four of the most common myths (Display) we hear.

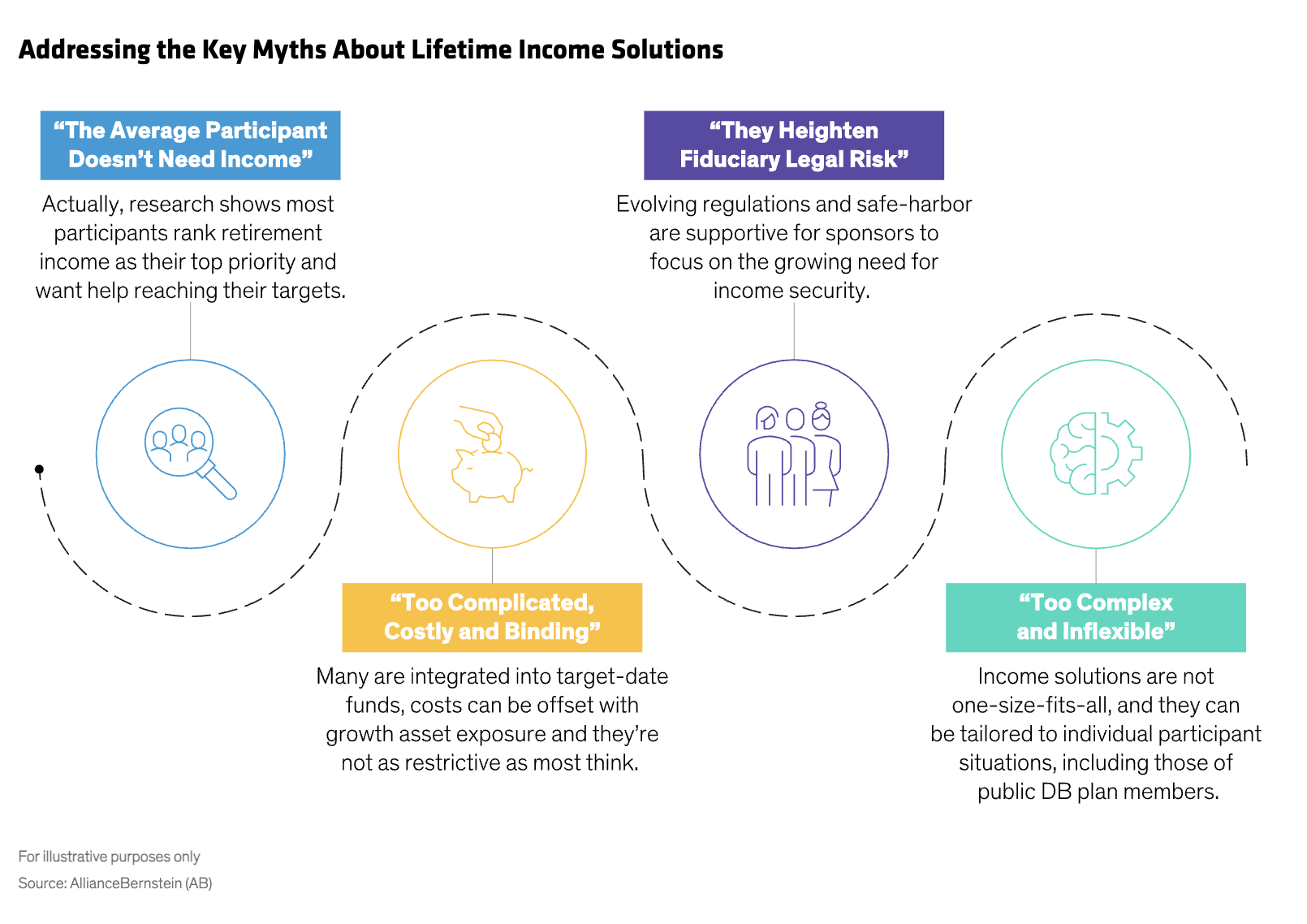

Myth One: The “Average” Participant Doesn’t Need Lifetime Income

Actually, research and our experience suggest that participants need—and want—lifetime income. A 2025 study showed that adding just five more years to retirement boosts the chances of running out of money by 41%. That longevity risk is very real for nearly everyone, which we think explains why most participants would try to deal with it given the opportunity.

In fact, according to AB’s 2025 Inside the Minds of Plan Participants survey, nine of 10 participants said they’d be at least “somewhat likely” to invest in a guaranteed income solution if it were offered in their plan, including 73% that were “very likely.”1 The impact of this year's market turmoil on retirement savings has only amplified the need, as we see it.

Myth Two: Lifetime Income Solutions Increase Plan Sponsors’ Fiduciary Risk

It’s understandable that DC plan sponsors have concerns about fiduciary liability, but we think it may be overstated. From our perspective, fiduciaries should prioritize doing the right thing for participants, not simply making decisions based on avoiding lawsuits. What’s more, the clarity provided by the SECURE Act and SECURE Act 2.0 safe-harbor umbrella seems to have resolved many, if not all, fiduciary concerns surrounding retirement-income solutions. With that as a starting point, we see an opportunity for robust dialogue around the topic of guaranteed income, which could help plan sponsors holding out for a “magic bullet” move forward.

Myth Three: They’re Too Complex, Expensive and Like Tattoos—Permanent or Painful if You Change Your Mind

On the contrary, some lifetime income solutions can be cost-effective, transparent and integrated into familiar vehicles like target-date funds. In fact, many solutions don’t impose surrender penalties or force participants to give up access to their assets when they lock in income. Still, not all solutions are alike, so we believe comparing the net impact of both explicit fees and implicit costs can help plan sponsors level the playing field when shopping for one. Some insurance types are fully liquid and portable—familiar qualities that participants see in other retirement options.

Myth Four: Default Income Solutions Are “One Size Fits All” and Can’t Be Customized

Not exactly. There have been advances in tools that help personalize income solutions at the sponsor and participant levels—based on age, salary, savings, other income benefits and even retirement goals. Sponsors and recordkeepers should be able to up their game in this area as data from more experience is factored into plan designs—and AI will likely contribute to the drive for personalization. Tailorable DC lifetime income solutions may even play a supporting role for workers who rely on public DB plans and Social Security: many DB plans are reducing benefits to newer workers, and 25% of public employees are ineligible for Social Security.

We believe the stars have aligned for lifetime income. The participant need is there, regulators seem increasingly supportive, and product innovation and implementation technology have advanced. Plan sponsors now just need to connect the dots, starting with separating fact from fiction about how guaranteed income solutions may help.

1 Response breakdown: “Very Likely,” 73%; “Somewhat Likely,” 21%; “Not Likely, 4%; “Don’t Know, 3%. Numbers may not sum due to rounding.

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams, and are subject to change over time.

“Target date” in a fund’s name refers to the approximate year when a plan participant expects to retire and begin withdrawing from his or her account. Target-date funds gradually adjust their asset allocation, lowering risk as a participant nears retirement. Investments in target-date funds are not guaranteed against loss of principal at any time, and account values can be more or less than the original amount invested—including at the time of the fund’s target date. Also, investing in target-date funds does not guarantee sufficient income in retirement.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein