Sunny Outlook, Shifting Sentiment

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways

- Economic resilience allowed the Fed to remain in wait-and-see mode in July, but July’s non-farm payroll report may cloud the horizon.

- Municipal issuance on pace to break records and continues to outpace reinvestment flows.

- Municipals appear attractive on a relative-value basis, particularly in the long end of curve.

General market update

Against a backdrop of solid economic data, including an upward revision of second-quarter GDP to a +3% annual rate, returns in the fixed income markets were mostly negative in July. With the labor market holding up and any disinflationary trend mitigated, market participants weren’t surprised when the Fed left rates unchanged at their meeting on July 30. Perhaps the data was overshadowed by concerns over the approaching tariff deadline and ongoing White House criticism of Fed chair Powell.

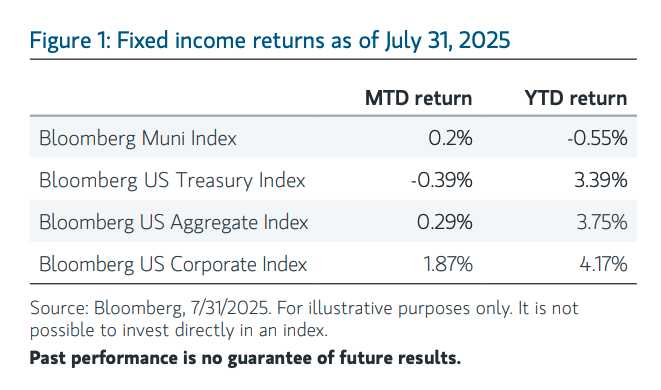

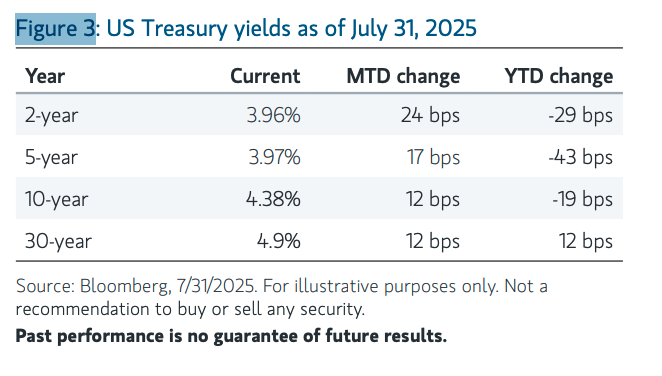

The 10-year Treasury began the month yielding 4.24%—the low close—and finished July at 4.37%. Most of the month was spent in a tight range between 4.33% and 4.48%. For the month, the Bloomberg US Treasury Index returned -0.26%, while the Bloomberg US Corporate Index eked out a small gain at 0.07% on tightening credit spreads. Municipals, continuing to deal with the headwind of a heavy calendar, posted a -0.2% return.

Market perception shifted on August 1 with a weak employment report. A miss on non-farm payroll expectations, combined with major revisions to the two prior months, pointed to a jobs market that was weaker than previously assumed. Market expectations for rate cuts increased, with futures again pricing in two cuts by the end of the year, and bonds rallied back to their early July yields.

Supply

So far 2025 is on track to be a record-setting year for municipal supply on the heels of the previous record year, 2024. July looks to have seen about $42 billion in issuance, and most forecasts are for total annual issuance to exceed $500 billion. Markets expect even typically quiet August to see more than $50 billion in issuance (JP Morgan Research, 7/30/2025).

Because municipal bonds are constantly maturing or being called, there’s a natural demand for bonds from existing bondholders looking to reinvest proceeds. One way analysts tend to decipher the potential market impact of supply is to look at net supply, defined as the difference between issuance and the reinvestment flows described above, plus coupon cash flows.

For January through June, the trailing five-year average net supply was -$16 billion. The negative number means the value of new bonds created in the market was less than the proceeds generated. Last year, net supply was positive $25 billion. In contrast, this year’s figure looks to be a stunning $75 billion (JP Morgan Research, 7/30/2025). Headwind indeed.

Market opportunity

We were hoping this month’s update would be as simple as “See you in September, don’t forget your sunscreen!” August historically is a quiet month and a popular one for vacations. Mid-month it appeared that tariffs weren’t reigniting inflation concerns, that economic data was mixed but strong enough to keep the Fed on the sidelines and that the rates market was hanging within a reasonably tight range. Municipal bonds specifically presented some attractive value, especially on the longer end of the curve, where ratios have cheapened compared to earlier in the year. Taken together they didn’t make a strong case that investors should hurry to get cash to work or that the sand was shifting beneath our feet.

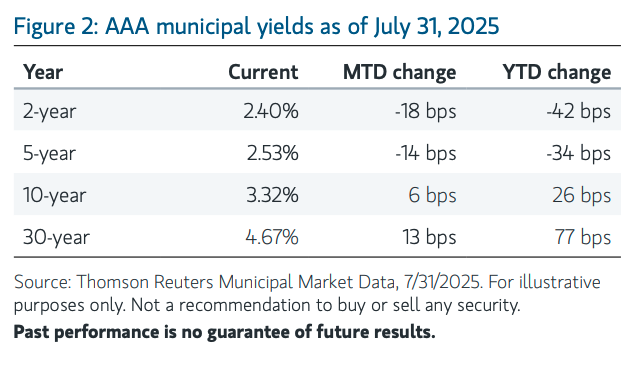

But then the July unemployment report came along. The weak report and accompanying revisions seem to have shifted market perception of the economy. The yield on the 10-year Treasury dropped more than 15 basis points (bps), and consensus firmed around a September rate cut. Benchmark AAA yields in municipals came down seven bps. While the market appears to believe that the Fed will be compelled to act, we’d caution that these assumptions are far from certain. We’ve seen before that a few data points and constantly changing headline news can shift market sentiment.

Our relaxed mindset entering July has switched. While the municipal calendar remains heavy, yields have declined and relative value has improved. Even after the move, yields remain attractive, but Friday was a stark reminder just how fast markets can move when conditions change. So while we still think the window of opportunity could remain open in August, investors might be better served acting sooner rather than later. Better not to get burnt. And don’t forget the sunscreen.

Economic outlook

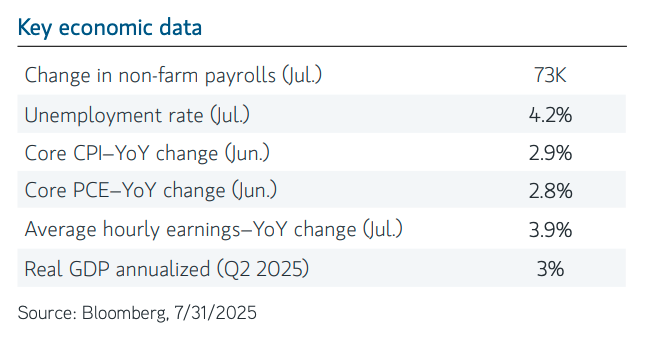

It would be hard to overstate the impact of the July mon-farm report. While the headline change wasn’t a big miss at up 73,000 compared with an expected 101,000, the revision to the previous two months was significant. The three-month average change in non-fam payrolls went from 150,000 to 64,000. To put that three-month number in perspective, the average monthly change from July 2010 through July 2025 has been 160,000 (though there were some extreme swings during the pandemic).

A full three months of well-below-average employment growth casts the economy in a much different light. For many, this would appear to be the first hard data signal of a meaningful slowdown. Market participants seem increasingly convinced that it will bring the Fed off the sidelines. There’s no August Fed meeting however, so all eyes will be on September’s.

Lasty, with the latest tariffs taking effect on August 1, we should see at least early indications of their impact. There’s also potential for more clarity on trade negotiations with the EU and China. With the prospect of new Russian sanctions imminent, both trade and geopolitical events remain sources of uncertainty over the near term.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

ABOUT

Parametric Portfolio Associates® LLC (“Parametric”), headquartered in Seattle, is registered as an investment advisor with the US Securities and Exchange Commission under the Investment Advisers Act of 1940. Parametric is a leading global asset management firm, providing investment strategies and customized exposure management directly to institutional investors and indirectly to individual investors through financial intermediaries. Parametric offers a variety of rules-based investment strategies, including alpha-seeking equity, fixed income, alternative and options strategies. Parametric also offers implementation services, including customized equity, traditional overlay and centralized portfolio management. Parametric is part of Morgan Stanley Investment Management, the asset management division of Morgan Stanley, and offers these capabilities through offices located in Seattle, Boston, Minneapolis, New York and Westport, Connecticut.

DISCLOSURES

This material may not be reproduced, in whole or in part, without the written consent of Parametric. Parametric and its affiliates are not responsible for its use by other parties.

This information is intended solely to report on investment strategies and opportunities identified by Parametric. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Past performance is not indicative of future results. The views and strategies described may not be suitable for all investors. Investing entails risks, and there can be no assurance that Parametric will achieve profits or avoid incurring losses. Parametric and Morgan Stanley do not provide legal, tax or accounting advice or services. Clients should consult with their own tax or legal advisor prior to entering into any transaction or strategy described herein.

Charts, graphs and other visual presentations and text information were derived from internal, proprietary or service vendor technology sources or may have been extracted from other firm databases. As a result, the tabulation of certain reports may not precisely match other published data. Data may have originated from various sources, including, but not limited to, Bloomberg, MSCI/Barra, FactSet or other systems and programs. Parametric makes no representation or endorsement concerning the accuracy or propriety of information received from any third party.

The views expressed in this report are those of the authors and are current only through the date stated at the top of this page. These views are subject to change at any time based on market or other conditions, and Parametric disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions are based on many factors, may not be relied on as an indication of trading intent on behalf of any Parametric strategy. This commentary may contain statements that are not historical facts, referred to as “forward-looking statements.” The strategy’s actual future results may differ significantly from those stated in any forward-looking statement, depending on factors such as changes in securities or financial markets or general economic conditions.

References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, a recommendation to purchase or sell such securities. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision.

The index data referenced herein is the property of ICE Data Indices, LLC (“ICE”), its affiliates and its third-party suppliers. ICE, its affiliates and its third-party suppliers accept no liability in connection with its use.

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. As interest rates rise, the value of certain income investments is likely to decline. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. While certain US government–sponsored agencies may be chartered or sponsored by acts of Congress, their securities are neither issued nor guaranteed by the US Treasury. Mortgage- and asset-backed securities are subject to credit, interest rate, prepayment and extension risk. Derivative instruments can be used to take both long and short positions, be highly volatile, result in economic leverage (which can magnify losses) and involve risks in addition to the risks of the underlying instrument on which the derivative is based, such as counterparty, correlation and liquidity risk. Diversification does not guarantee profit or eliminate the risk of loss.

All contents ©2025 Parametric Portfolio Associates® LLC. All rights reserved. Parametric Portfolio Associates® and Parametric® are trademarks registered with the US Patent and Trademark Office and certain foreign jurisdictions. Parametric is headquartered at 800 Fifth Avenue, Suite 2800, Seattle, WA 98104. For more information regarding Parametric and its investment strategies, or to request a copy of Parametric’s Form ADV or a list of composites, contact us at 206 694 5500 or visit www.parametricportfolio.com.

For more information regarding Parametric and its investment strategies, or to request a copy of Parametric’s Form ADV or a list of composites, contact us at 206 694 5500 or visit www.parametricportfolio.com.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | NOT A DEPOSIT

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All