Rising US deficits and debt, coupled with less predictable policy, have created anxiety about US exceptionalism and spurred bond investors to re-examine their diversification options away from US assets. While no other capital market offers the depth and liquidity of the US and there’s no single credible replacement for US Treasuries, we believe that there’s a strong case for considering an increase in ex-US exposure. Europe is a prime candidate: its bond markets have grown, are high quality and may benefit from a fall in yields. And as European markets are considerably smaller than the US’s, even a small shift in US investors’ allocations may make a significant price difference.

European Markets: Credibility Meets Opportunity

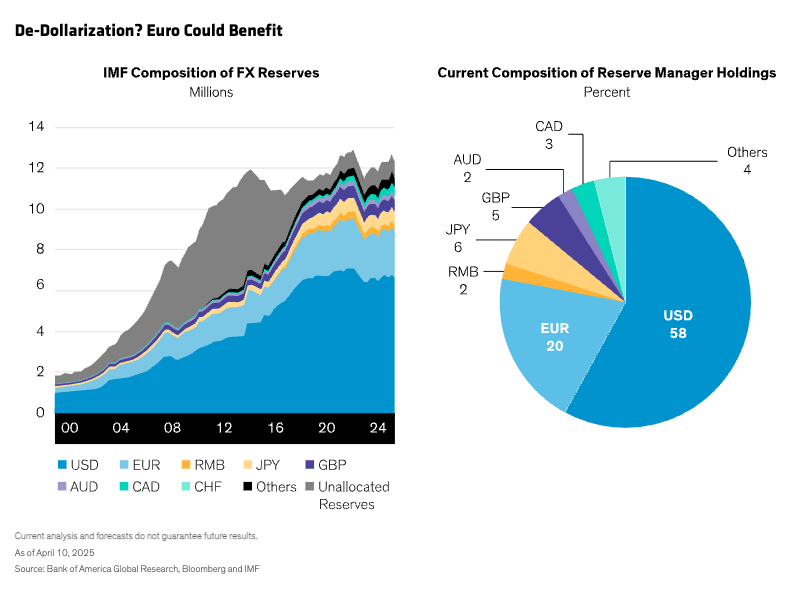

The euro is second-largest in the world’s central bank reserve managers’ currency holdings, currently at 20% of total (Display), down from a peak of around 30%. If investors start to rotate out of US dollars (USD) into euro, that could contribute to the euro appreciating against USD.

Three major issues driving previous euro weakness have been fixed: following the resolution of the 2012 European sovereign debt crisis, the European Central Bank (ECB) has proven and diversified tools at its disposal; the period of negative interest rates is over and European yields are now at attractive levels relative to history; and the ECB is no longer constraining the supply of euro bonds through quantitative easing.

The depth and liquidity of the euro bond markets have also been issues in the past but have improved over time. In investment-grade corporate credit, for instance, the euro market is now over 40% the size of the USD market—plenty big enough to warrant a higher allocation for global investors.

A modest percentage reallocation out of USD bonds into euro fixed-income could have an outsize impact in price terms, in our analysis. For example, the German government bond (Bund) market is one-tenth the size of US Treasuries, so every dollar that moves out of Treasuries has a proportionately higher market impact on Bunds.

Two Ways to Capitalize: Hedged and Unhedged

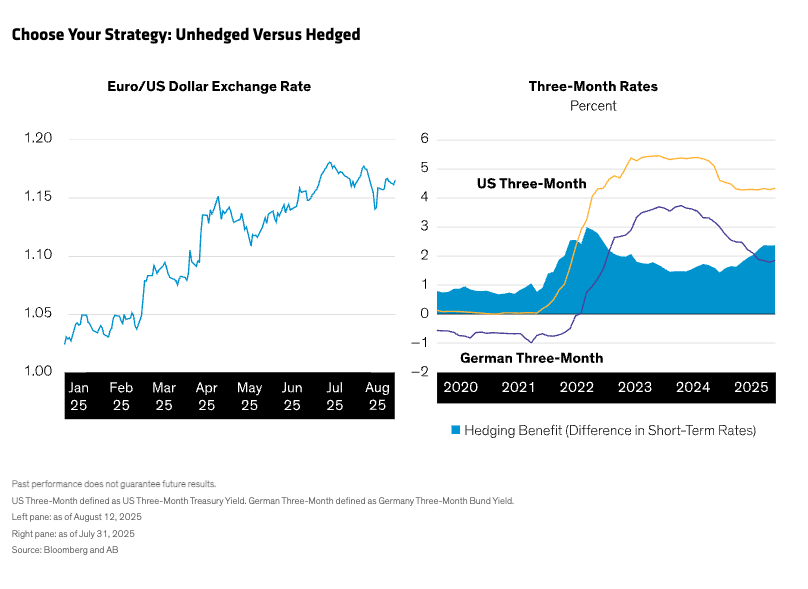

The euro has risen by 11% against USD this year through August 12 (Display, left). For fixed-income investors expecting that trend to continue, an unhedged position in euro bonds may be compelling.

Alternatively, as we see it, a hedged approach may be beneficial for US dollar-based investors seeking exposure to euro bonds while avoiding currency-related volatility. Owing to the gap between short-term euro and USD rates (which has widened this year as the ECB continued to ease while the Fed paused), hedging their exposure to European bonds back to USD could enhance their yield by almost 2.5% (Display, right).

Global investors can capitalize on these dynamics by diversifying their allocation to US assets with European strategies (either hedged or unhedged, depending on their currency views).

Interest Rates in Europe Have Further to Fall

We believe that interest rates in the euro area have a more clearly defined path to fall than in the US, with potentially less volatility. In the short term, US tariffs and policy uncertainty will continue to weigh on European economies. Meanwhile further disinflationary forces may come from China, whose exports will likely be partially redirected to European markets. These pressures could lead to inflation undershooting the ECB’s targets, paving the way for more rate reductions than the single cut in our current forecast.

Meanwhile, medium-term growth prospects for the region have improved, thanks to large-scale fiscal easing by Germany, Europe’s largest economy. In our view, this would likely be supportive of credit.

European Corporate Credit Looks Attractive

Although the US’s recently-agreed baseline 15% tariffs are higher than the ECB’s base case, we believe they won’t cause major disruption to credit markets, and European high-yield and investment-grade bonds still look compelling to us. European corporates entered the economic slowdown with strong balance sheets and healthy margins and could continue to weather further economic weakness, in our view.

European credit markets also enjoy strong technical support, with buyers emerging whenever spreads and yields increase. As cash rates in Europe progressively dwindle, we expect further flows out of deposit and money market funds to continue to support European credit markets.

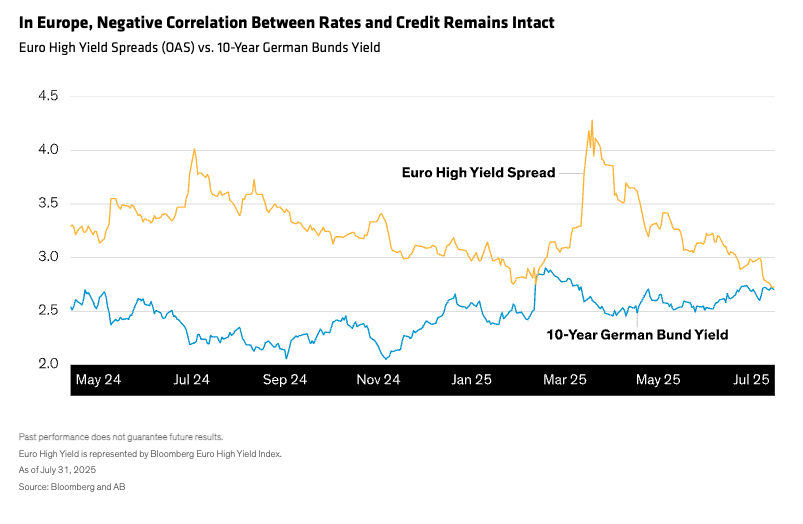

European Rates and Credit Are Negatively Correlated

While US rates and credit markets have seen periodic shifts in correlations, in Europe these two asset classes have remained negatively correlated throughout (Display).

We believe this supports the case for a European credit barbell—a strategy that combines rates and credit exposure in a single, dynamically managed portfolio. A barbell approach seeks to balance the two main risks within fixed-income markets: interest-rate risk and credit risk.

In a barbell portfolio, higher-quality assets such as government bonds help mitigate drawdowns in times of market stress—such as during the present period of trade-policy volatility—while higher-yielding assets such as high-yield corporate bonds provide extra yield and return when markets are doing well. The respective allocations are managed dynamically.

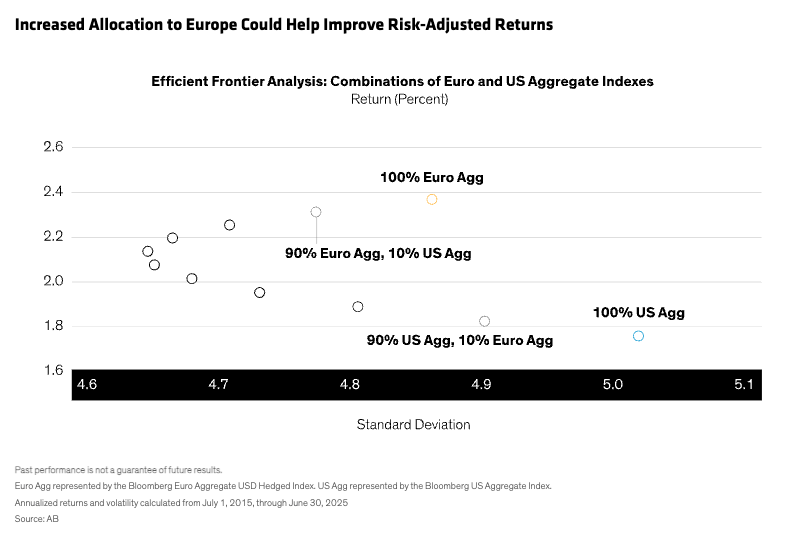

European Assets Have Potential to Improve Risk-Adjusted Returns

For US and other US dollar-based investors, an allocation to a European core plus strategy has the potential to diversify sources of income, differentiate yield contribution and improve risk-adjusted returns, in our view. In the Display below, we show how combining US and European fixed-income assets has historically created more efficient portfolios.

While US policy changes have whipped up storm-clouds worldwide, we see a potential silver lining for alert investors: prudent, proportionate and timely diversification could prove to be their trump card.

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams, and are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein