Mainstream commentary repeats a simple refrain: “Buybacks return capital to shareholders.” The logic sounds convincing. A company reduces its outstanding shares, giving each shareholder a larger slice of the earnings pie. But as I’ve discussed in past work like “Stock Buybacks Aren’t Bad, Just Misused,” the reality is more complex. If corporate buybacks were an actual return of capital, like a dividend, it would mean “cash in your pocket” paid equally to all shareholders. However, buybacks, in reality, distribute that “return” unevenly, primarily due to insider selling.

What does that mean?

To benefit from a corporate buyback, an individual must sell their shares to the company. Conversely, those holding on to their shares are not compensated. The only benefit shareholders may receive is a proportional increase in their ownership percentage, which is meaningless if the company’s intrinsic value isn’t increasing.

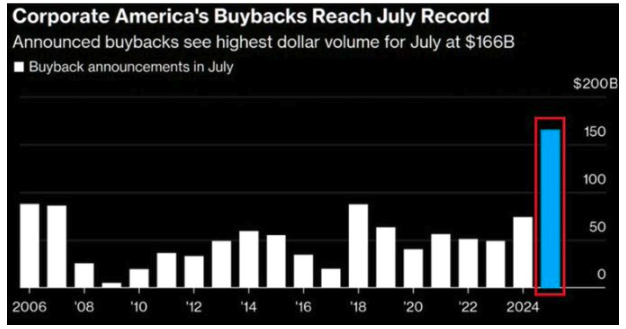

Notably, the latest data on insider selling and corporate buybacks makes this disconnect very clear. In July, S&P 500 companies announced $166 billion in buybacks, the largest July on record.

However, for corporations to perform buybacks, they need someone to buy their shares from. So, who is mostly selling their shares?

It’s corporate insiders, of course. Why? Since the turn of the century, changes in compensation structures have made companies heavily dependent on stock-based compensation. Insiders regularly liquidate shares that were “given” to them as part of their overall compensation structure to convert them into actual wealth. As the Financial Times previously penned:

“Corporate executives give several reasons for stock buybacks but none of them has close to the explanatory power of this simple truth: Stock-based instruments make up the majority of their pay and in the short-term buybacks drive up stock prices.”

Furthermore, a report on a study by the Securities & Exchange Commission found the same:

- SEC research found that many corporate executives sell significant amounts of their shares after their companies announce stock buybacks.

Interestingly enough, the July data also supports that analysis.

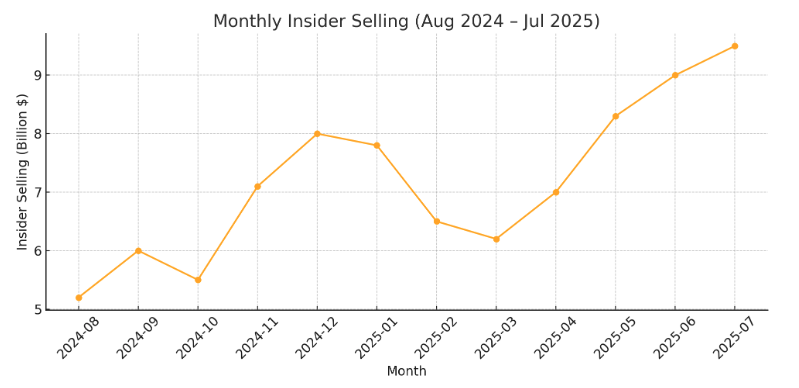

In July, insider selling reached its highest level since at least 2018, with only 151 companies reporting insider buying. That means fewer than one-third of firms saw insiders increasing their stakes. If buybacks truly represented a confident return of capital, insiders, the people with the most information, would buy alongside the company. They weren’t.

That’s because buybacks are often used for another purpose entirely: boosting earnings per share (EPS) without improving actual profits. This EPS inflation can help meet Wall Street targets, trigger executive bonuses, and maintain short-term stock price momentum. For insiders planning to sell, that’s an ideal setup. Announce the buyback, let the price firm, and sell into the strength. It’s perfectly legal under SEC safe-harbor provisions, but the same price manipulation led the SEC to ban buybacks before 1982.

In short, “buybacks return capital to shareholders” is more of a myth. However, for many companies, “buybacks return capital to selling insiders.”

July Data Is A Warning

It should raise questions when you see record buybacks and a surge in insider selling in the same month. As noted, July’s $166 billion in repurchase announcements set a record, as insider selling also surged. Such should not be a surprise given the market’s sharp rise since the April lows. If you are an insider of a company and are sitting on significant gains from option-based compensation, it makes sense to convert those gains into actual wealth. However, that data should also serve as a warning.

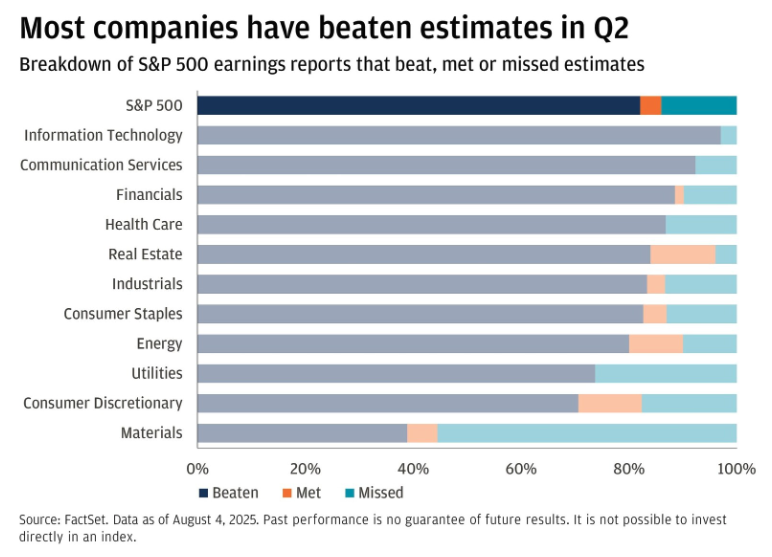

Let’s examine Q2’s “strong earnings season.” Yes, there was a significant “beat rate” of companies exceeding estimates.

However, investors must take that news with a “grain of salt” for two reasons.

First, since April, consensus Q4 U.S. GDP expectations had dropped by about one percentage point, while earnings expectations for the equal-weight S&P 500 have fallen around 6%. The advantage of low expectations is that they set a low bar to surpass. With three-quarters of the reporting season complete, over 80% of S&P 500 companies have exceeded Q2 earnings expectations, well above the 10-year average of 75%.

Secondly, as noted in last weekend’s #BullBearReport, the overall economy’s weakness was evident. Earnings growth would not have occurred without Megacap Technology and major Wall Street banks.

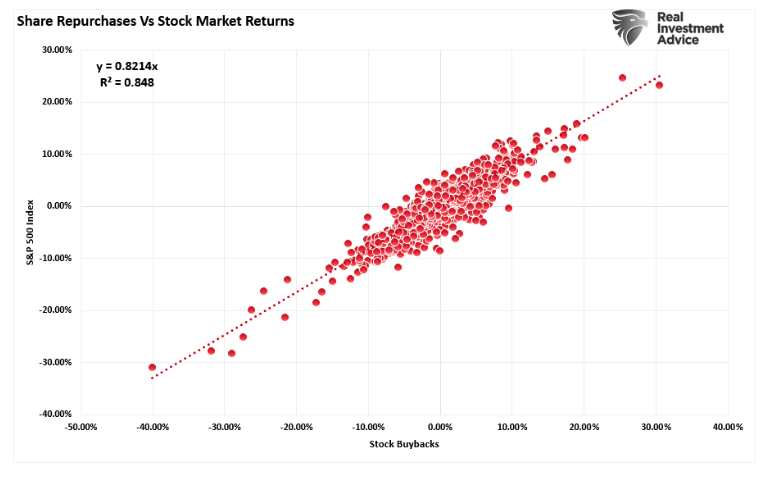

Yes, the market is doing well on the surface. However, as discussed previously, a significant correlation exists between corporate share buybacks and stock market performance.

This isn’t an isolated anomaly. It would make sense that insiders are more likely to sell, and in larger volumes, as share prices rise. As such, it should also be unsurprising that the timing of insider selling and corporate buybacks is deliberate. When a buyback reduces the share count, it boosts EPS. Wall Street rewards those EPS beats, often pushing the stock higher in the short term. Insiders then use that strength to liquidate part of their holdings at better prices.

July’s numbers fit the pattern perfectly. Management teams authorized billions in buybacks, yet the people with the most profound knowledge of company prospects were not putting their own money alongside yours. Instead, the reduced float created the illusion of improved performance while insiders quietly exited.

That’s not a return of capital, it’s a transfer of capital from the corporate treasury to those selling their shares.

Investors should continually evaluate buyback programs in the context of insider activity. A buyback combined with insider selling is not a sign of confidence. It’s often a liquidity event for executives. Despite massive buyback authorizations, July’s lack of insider buying speaks louder than any corporate press release.

Why This Matters: EPS Engineering and Long-Term Investor Risk

In 2023, Jason Zweig penned an article for the WSJ stating:

“Over the past five years, according to S&P Dow Jones Indices, big U.S. companies have spent $3.9 trillion repurchasing their own stock. Buybacks are neither bad nor good. They are simply a tool. Just as you can use a hammer either to build a house or knock one down, buybacks are useful in the right corporate hands and dangerous in the wrong ones.“ – Jason Zweig, WSJ

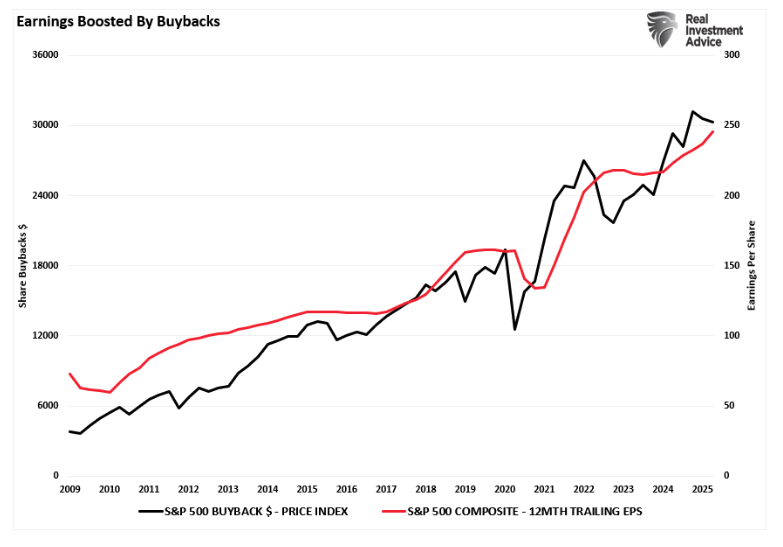

That is a fair statement. The impact of share buybacks is vital to manufacturing earnings growth since we measure earnings on a per-share basis. In other words, if you reduce the number of shares outstanding, corporate earnings “per share” improve, as shown below.

The connection between insider selling and buybacks is more than an optics problem; it’s a fundamental misallocation of shareholder capital.

“But Lance, I was told that when a company buys back their shares that is their conviction about the future of the business.”

Yes, there are times when that might be true. But think about it this way: If I were convinced about my business, wouldn’t I rather spend my capital on investments or assets that will increase my future revenue and growth? Take Apple (AAPL) for instance. Over the last 3 years, revenue and earnings growth have stagnated as the company bought back more than $500 billion in stock.

However, the current administration’s threat of massive tariffs was enough to push Apple into spending $600 billion over the next five years to invest in the company rather than just repurchase shares. Does that speak of “conviction” about the company’s future or a defensive action to protect existing profitability? If investing $600 billion is a “good idea,” why didn’t Apple do it years ago?

In Apple’s case, as well as most companies engaging in share buybacks, this has not benefited all shareholders. The reduction in share count, which inflates EPS, helps management meet quarterly targets. But those increases don’t necessarily increase intrinsic value. That’s why the SEC originally prohibited them, they were seen as a form of market manipulation.

Investors must be cautious about understanding the impact of buybacks on earnings when investing in companies. As Warren Buffett noted:

Finally, an important warning: Even the operating earnings figure we favor can easily be manipulated by managers who wish to do so. Such tampering is often considered sophisticated by CEOs, directors and their advisors. Reporters and analysts embrace its existence as well. Beating ‘expectations’ is heralded as a managerial triumph. That activity is disgusting. It requires no talent to manipulate numbers: Only a deep desire to deceive is required. ‘Bold, imaginative accounting,’ as a CEO once described his deception to me, has become one of the shames of capitalism.“

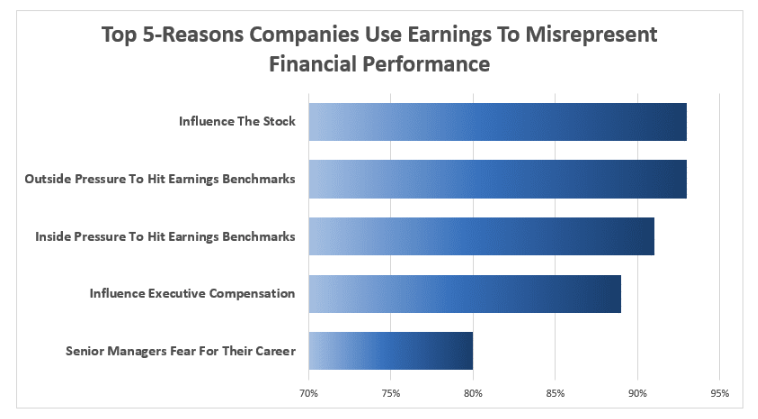

Why would CEO’s want to manipulate earnings? Unsurprisingly, a WSJ survey of CFOs found that 93% pointed to “influence on stock price” and “outside pressure” as the reasons for manipulating earnings figures.

When insiders sell into a seemingly “bullish” environment, they benefit from the inflated valuation, while remaining shareholders are left holding a potentially overvalued stock. Over time, this practice can erode shareholder returns, especially if the company has diverted cash from productive uses like R&D, acquisitions, or debt reduction, into buybacks designed to prop up metrics.

The July data should serve as a warning. Record buybacks with historically low insider buying are a red flag. They suggest that insiders may not believe the stock is undervalued or that growth prospects are as strong as assumed. They also indicate that the primary beneficiaries of the buyback program are the insiders themselves.

For long-term investors, that’s a problem. Capital used for financial engineering today is capital not used for future growth.

Track insider transactions closely if you’re evaluating a company with an active buyback program. Look for patterns where buybacks align with heavy insider selling. Those patterns often precede underperformance.

Remember: a dividend puts cash in your pocket. A buyback only benefits you if the stock is genuinely undervalued and insiders are holding, not selling.

In July, that wasn’t the case.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Real Investment Advice

Read more commentaries by Real Investment Advice