While equity markets have run hot and cold, high-yield bonds have been steady performers over the past 12 months. Following a strong second quarter, high yield is one of the top-performing fixed-income asset classes thus far in 2025. We expect this momentum to continue on the strength of sound fundamentals, elevated yields and conservative balance-sheet management.

On the heels of additional tariff announcements and bellicose trade rhetoric, investors are now digesting weaker-than-expected jobs growth and evidence of economic slowing. You might expect these economic risks to rattle the high-yield market. But they haven’t and, in our view, likely won’t. Here’s why.

Fundamentals Support Tight Credit Spreads

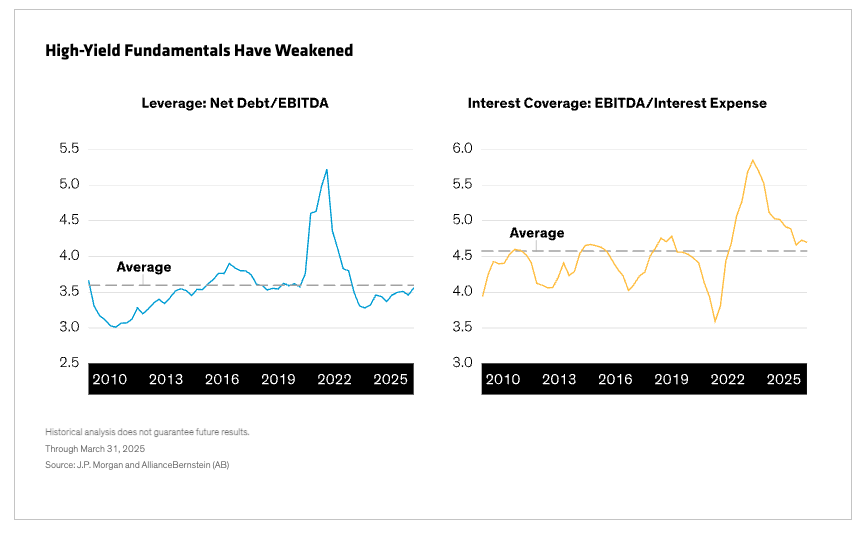

Corporate fundamentals remain sound despite recent softening, both in the US and Europe. Yes, credit downgrades are outpacing upgrades, while interest-coverage ratios and EBITDA margins have deteriorated. But fundamentals are coming off a position of remarkable strength following a post-pandemic housecleaning that cleared out underperformers and increased overall credit quality. These metrics are now inching back toward their long-term averages (Display).

.

.

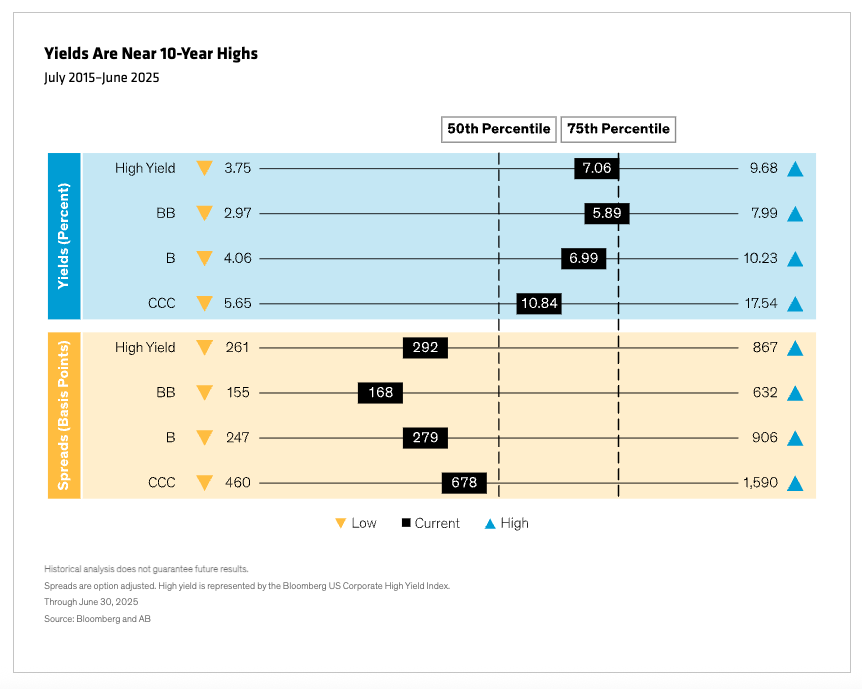

As for today’s narrow credit spreads, we’re not especially concerned. Given elevated rates, spreads comprise a smaller portion of yield. More importantly, spreads don’t drive returns; yield does. While a bond’s spread reflects in-the-moment assessments of its credit risk relative to Treasuries, yield to worst captures the bond’s expected return from both government yield levels and credit spreads.

That’s why, in our analysis, yield to worst is a reliable proxy for five-year forward returns, regardless of the environment. Yield to worst is currently hovering near the top 25% of its 10-year range (Display). Given these elevated yields, we expect high-yield returns to compete with those of stocks in the coming years.

Of course, there’s a risk that spreads could widen. We saw this in April when credit spreads blew out temporarily in reaction to new tariffs. But the sector was resilient, and spreads eventually retreated. This highlights both the sticky nature of spreads, which can stay range bound for extended periods, and the solid fundamentals of today’s high-yield market.

That said, we think spreads may widen as short rates rally on Fed rate-cut expectations. But because high-yield bonds would likely benefit from the rate rally, high-yield bond prices could rise even as spreads widen. Lastly, trade-related headline risks aren’t going away soon, and we anticipate continued spread volatility accordingly.

We expect yields to provide ample cushion against the negative price effects of spread widening, underscoring the high-yield market’s resilience.

Trade Uncertainty Has Led to Corporate Belt Tightening

Beyond upending the financial markets and keeping US trading partners guessing, trade uncertainty has had the unintended effect of strengthening corporate balance sheets. Because it’s difficult to budget against a chaotic backdrop, high-yield issuers have chosen instead to bolster working capital and keep debt levels manageable as they wait to see how the tariff and trade picture settles.

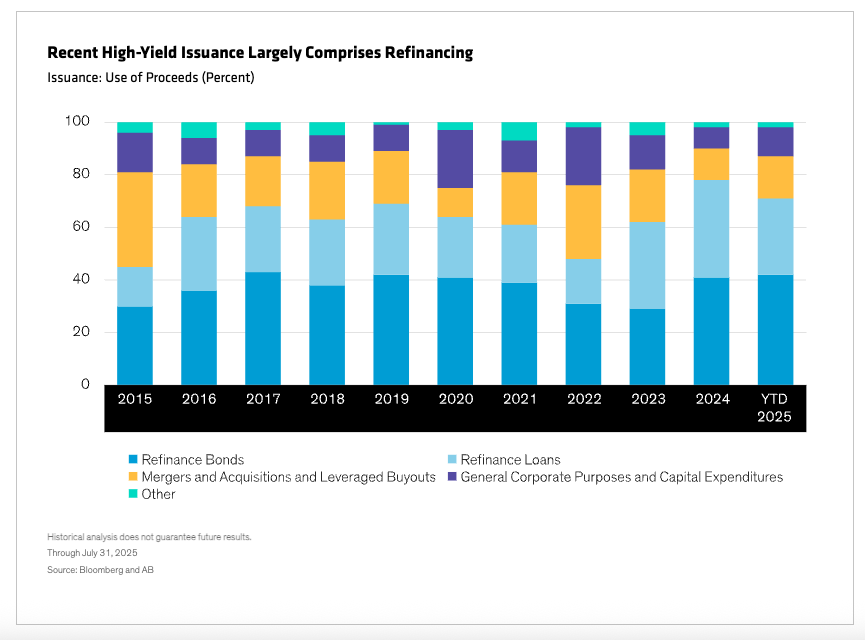

This more conservative fiscal approach is reflected in both the limited volume of net new issuance in the European and US markets and issuers’ use of proceeds. An explosion of new issuance would be concerning—both to us and to the markets—particularly if it were used to finance leveraged buyouts and M&A activity. But that’s not what we’re seeing.

Instead, new issuance has largely involved rolling over debt and refinancing (Display)—benign corporate actions that have kept spreads sticky and the high-yield universe relatively clean. Even in the event of an external shock, we wouldn’t expect the high-yield markets to buckle, because market excesses have largely been wrung from the system.

Trade wars have not only forced issuers to manage debt more carefully but have also assuaged any lingering concerns about a looming maturity wall. Maturity walls have worried investors for the past 30 years, as there frequently appears to be a large amount of debt due to mature in the next two to four years. This time, with issuers quietly refinancing and near-term maturities skewing toward higher-quality debt, what could have been a concern has largely passed uneventfully—a trend we expect to continue.

High-yield bonds are by no means immune to economic disruption—nor are they recession-proof. But with credit quality high, yields elevated and issuers managing their balance sheets prudently, a more boring version of high yield may be just the recipe for weathering an unpredictable market.

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams, and are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein

.

.