Royalty and Streaming Companies Lead Gold Sector with Record Results

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe latest wholesale inflation numbers in the U.S. took some of the wind out of Wall Street’s sails this week, but they haven’t dulled investor enthusiasm for gold. Even with a hotter-than-expected producer price index (PPI) reading in July, the yellow metal continues to trade near historic highs, and gold stocks, particularly royalty and streaming companies, are delivering record results.

As I’ve often said, government policy is a precursor to change. The PPI, which measures prices producers receive for goods and services, jumped 0.9% in July from the previous month and 3.3% from a year earlier, the largest monthly increase in three years. The core PPI, which strips out volatile food, energy and trade services, advanced 2.8% compared to the same months last year.

The biggest driver was services, which rose a full 1.1% last month. This could suggest that companies are passing along higher import costs related to tariffs, something Goldman Sachs recently projected could hit consumers’ wallets in a big way by the fall.

The PPI report rattled rate-cut expectations. For the record, traders still seem to anticipate the Federal Reserve will lower borrowing costs in September, but the odds of a “jumbo” half-point cut have diminished.

While the White House has been vocal in urging the Fed to “go big,” central bankers may prefer to stick with smaller, sequential moves, especially with inflation proving sticky in some areas.

Gold’s Resilience in the Face of Mixed Data

If there’s been one constant in 2025, it’s gold’s ability to attract buyers in an uncertain environment. Spot prices have been consolidating in the mid-$3,300s after hitting an all-time high of $3,500 an ounce in April and reaching $3,439 as recently as July 22. The metal’s steady performance this summer has been fueled by a number of factors, including inflation concerns, a softer U.S. dollar, central bank demand and the expectation of lower interest rates.

Gold also tends to shine brightest during periods of uncertainty, whether economic, political or geopolitical. This year, that list has been long: renewed tariff skirmishes, questions about the Fed’s independence and elevated levels of global debt have all driven investors toward hard assets.

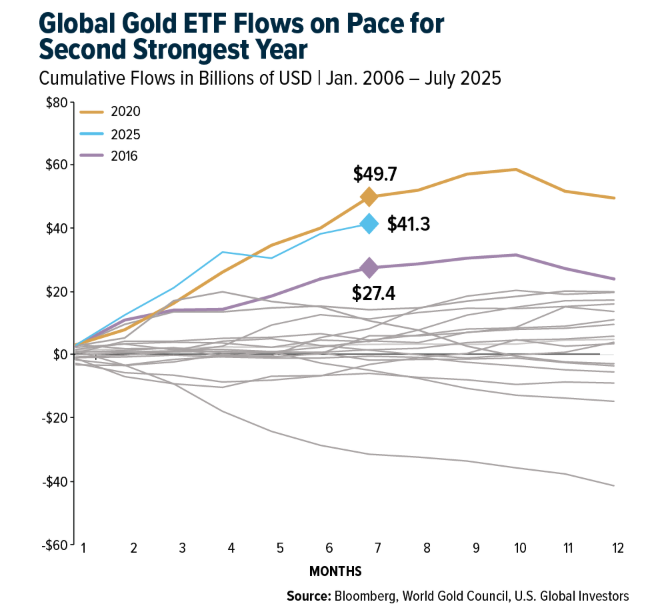

According to the World Gold Council (WGC), gold-backed exchange-traded funds (ETFs) added $3.2 billion in July alone, raising total assets under management (AUM) to $386 billion, a month-end high. Global flows are now on pace for the second-strongest year on record, following 2020.

Why We Favor Royalty and Streaming Companies

As many of you know, we have long favored royalty and streaming companies, and their latest quarterly results only reinforce that view. These firms don’t own or operate mines themselves. Instead, they provide upfront financing to miners in exchange for the right to purchase a portion of future production—either through royalties or streams—at a fixed, often heavily discounted, price.

This model has several compelling advantages, including lower risk exposure. Royalty and streaming firms have no direct operating costs, meaning they’re insulated from rising labor and fuel prices. Their portfolios often span multiple mines and jurisdictions, and they’ve also demonstrated strong cash flow.

In short, we believe royalty and streaming companies offer a “happy medium” between owning bullion and owning traditional mining equities. They capture much of the upside in a rising gold price environment while providing downside protection during pullbacks.

Record-Breaking Quarters

The June quarter and first half of 2025 were nothing short of spectacular for the big names in the royalty and streaming space.

Franco-Nevada reported record revenue of $369.4 million for the quarter, up 42% year-over-year. Operating cash flow surged 121% to a record $430.3 million, while net income more than doubled to $247.1 million. The company also posted record adjusted EBITDA margins.

Wheaton Precious Metals likewise delivered all-time highs in the second quarter, generating $503 million in revenue and $415 million in operating cash flow. Net earnings came in at $292 million, and the company ended the quarter with $1 billion in cash, no debt and an undrawn $2 billion revolving credit facility.

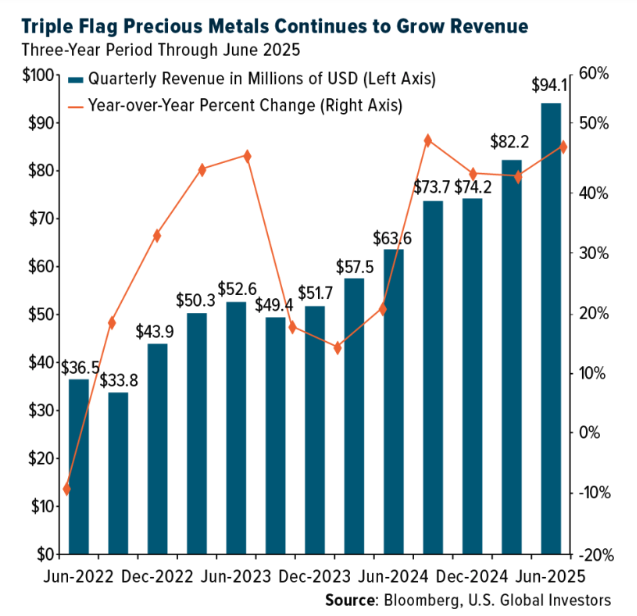

Triple Flag Precious Metals, a relative newcomer compared to its larger peers, posted record operating cash flow per share and announced its fourth consecutive annual 5% dividend increase since its IPO in 2021. Revenues have been growing steadily for the past seven quarters, hitting a new all-time high of $94 million in the June quarter, representing an increase of almost 50% compared to the same quarter in 2024.

These results demonstrate why royalty and streaming companies have been gaining market share in investors’ portfolios. They combine the potential for capital appreciation with consistent income, an attractive mix in a yield-starved world.

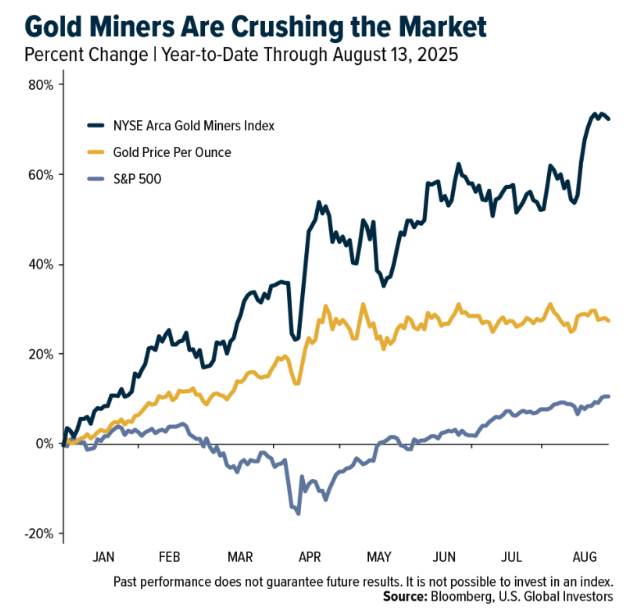

Miners Regaining Favor

Traditional gold miners are also benefiting from the metal’s strength. UBS analysts recently upgraded their outlook on the sector, noting that after years of underperformance, miners are rebuilding investor trust through disciplined capital management.

If gold prices remain steady, UBS sees the potential for increased stock buybacks, accelerated growth projects and more merger and acquisition (M&A) activity. Their top picks include Barrick Gold, Kinross Gold, AngloGold Ashanti, Endeavour Silver and Franco-Nevada.

Tariffs, Inflation and the Case for Gold

Returning to the inflation picture, Goldman Sachs has been clear that the tariff burden is shifting from businesses to consumers. Their models suggest that by the fall, about two-thirds of the cost of recent tariffs will be borne directly by U.S. households. This is already showing up in the PPI’s services component and could feed into consumer prices later this year.

For investors, this creates a tricky environment. On the one hand, higher inflation readings could prompt the Fed to slow the pace of rate cuts, which might limit gold’s upside in the near term.

But on the other hand, persistent inflation—and the potential for policy missteps—reinforces gold’s role as a hedge.

History shows that gold has often performed well in periods of negative real interest rates, when inflation outpaced nominal yields. If tariffs and other factors keep inflation elevated while the Fed is easing, we could see that dynamic play out again.

Strong central bank demand, steady ETF inflows and robust free cash flow generation from royalty and streaming companies all point to continued strength in the gold space. For investors looking to participate in this trend, we believe these companies offer an attractive balance of growth potential, income and risk management.

Index Summary

- The major market indices finished up week. The Dow Jones Industrial Average gained 1.74%. The S&P 500 Stock Index rose 0.94%, while the Nasdaq Composite climbed 0.81%. The Russell 2000 small capitalization index gained 3.07% this week.

- The Hang Seng Composite gained 2.28% this week; while Taiwan was up 1.30% and the KOSPI rose 0.49%.

- The 10-year Treasury bond yield rose 3 basis points to 4.319%.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was Frontier, up 35.3%. Airlines in TD’s coverage have been citing improvements in the supply chain. JetBlue noted that GTF durability has been “better than expected,” and the airline now expects fewer grounded aircraft than previously anticipated, with the peak in 2025. Volaris also shared a more positive outlook on GTF-related groundings and expects gradual improvements from here. United noted that Boeing is delivering MAX orders slightly ahead of schedule, though 787 production remains constrained.

- According to J.P. Morgan, ZIM shares were up 20% following a Bloomberg-sourced article from an Israeli newspaper, reporting that ZIM CEO Eli Glickman, together with Israeli car importer Rami Unger, are considering a management buyout of ZIM. The potential bid could value the company at up to $2.4 billion.

- Fare growth for bookings in July accelerated compared to June. American Airlines realized the strongest improvement in global fares, with an increase of 270 basis points (bp) in July versus June. Delta Air Lines (220 bp) and United Airlines (140 bp) also showed meaningful improvements, according to UBS.

Weaknesses

- The worst-performing airline stock for the week was Sabre, down 4.0%. Spirit filed its 10-Q for Q2 2025, which stated: “There is substantial doubt as to the Company’s ability to continue as a going concern.” Minimum liquidity covenants in the company’s debt obligations and credit card processing agreement require financial results to improve at a rate faster than what the company is currently anticipating, according to TD.

- Fiscal 2026 first-quarter results for Ocean Network Express showed profit weakening, falling 89% year-over-year to $86 million. Company materials stated that the year-over-year decline of $694 million included a $310 million drop from freight rates and a $322 million increase in operating costs.

- The U.S. Department of Justice said Delta Air Lines and Grupo Aeromexico should lose antitrust protection that allows the airlines to coordinate scheduling, pricing, and capacity decisions. The statement was made in a filing on Monday in support of a U.S. Department of Transportation recommendation calling for the revocation of their antitrust immunity.

Opportunities

- Airline Weekly reported that new extra-legroom seats have been rolled out on 160 of Spirit’s 200 aircraft, completing the planned retrofits announced in May. Spirit currently has an in-service fleet of 155 aircraft. Citing Spirit’s VP of Network Planning, the airline believes that with its new premium product offerings, lower fares, and strong presence in Fort Lauderdale, it is well positioned to attract some passengers currently flying American out of Miami.

- According to UBS, Maersk’s Ocean unit is focused on diversification compared to peers and on achieving one of the lowest unit costs in the industry. In Logistics, the emphasis is on short-term profit margin improvements. In Terminals, the goal is to grow the business further while maintaining high levels of return on invested capital (ROIC).

- According to Morgan Stanley, scheduled capacity for Copa Airlines increased by 229 basis points this week for the fourth quarter of 2025. Scheduled capacity for the first quarter of 2026 also rose, up 454 basis points.

Threats

- Air Canada is offering flight attendants a 38% pay raise in an effort to avoid disruptions following a 97.7% union vote in favor of a strike mandate. However, negotiations with the union representing its mainline flight attendants have reached an impasse. Both parties may issue notice for a 72-hour strike or lockout. Management has asked the government to direct the parties to binding arbitration, according to Raymond James.

- According to Goldman, vessel traffic from China to the U.S. dropped sequentially by 4% and was down 19% on a year-over-year basis. This generally soft pattern could persist through mid-August based on Port of Los Angeles data. The ramifications from recent tariff-related implementations and their magnitudes have yet to play out.

- The FAA has proposed extending its order limiting the number of arrivals and departures at Newark Airport through October 24, 2026. The agency is also enhancing infrastructure and staffing at the Philadelphia TRACON, which manages Newark air traffic, including deploying a fiber optic network and satellite backup systems, as well as increasing the number of air traffic controllers, according to Morgan Stanley.

Luxury Goods and International Markets

Strengths

- Over 90% of S&P 500 companies have reported second quarter results, and the numbers are strong. According to FactSet, earnings are up 11.8%, well above the 4.9% expected at the start of the quarter. Additionally, 81% of companies beat EPS estimates, surpassing the 77% average over the past year.

- According to Vogue Business’s mid-August 2025 report, The Long View: Key Trends Shaping Hospitality, luxury hospitality and experiential sales are up about 5% year-over-year. The growth is fueled by affluent Millennials and Gen Z seeking immersive, health-focused experiences such as luxury cruises, private jets, and wellness resorts. Brands like LVMH are capitalizing on the trend through hotel acquisitions, partnerships, and integrated travel offerings—further reinforcing the sector’s momentum.

- The RealReal, an online retailer of luxury goods, was the top performer in the S&P Global Luxury Index, surging 20.8%. It reported Q2 revenue of $165.2 million, up 14% year-over-year and well above analyst expectations of approximately $159.5 million.

Weaknesses

- In July, China’s new yuan-denominated bank loans fell by about 50 billion yuan, marking the first contraction since July 2005, a gap of nearly 20 years. The decline highlights weak borrowing demand despite government efforts to stimulate domestic consumption. This week, China also reported weaker-than-expected economic data.

- Tapestry and Pandora shares fell sharply this week after both companies reported quarterly results. Tapestry posted year-over-year and quarter-over-quarter revenue growth but missed earnings-per-share estimates due to significantly weaker operating margins and one-time write-offs. Pandora reported annual revenue growth, but investors were spooked by larger-than-expected losses in Europe, its key market.

- Mao Geping Cosmetics, a premium Chinese cosmetics brand, was the worst-performing stock in the S&P Global Luxury Index, falling 9.1%. In its latest half-year results, the company reported revenue and net income below analyst expectations.

Opportunities

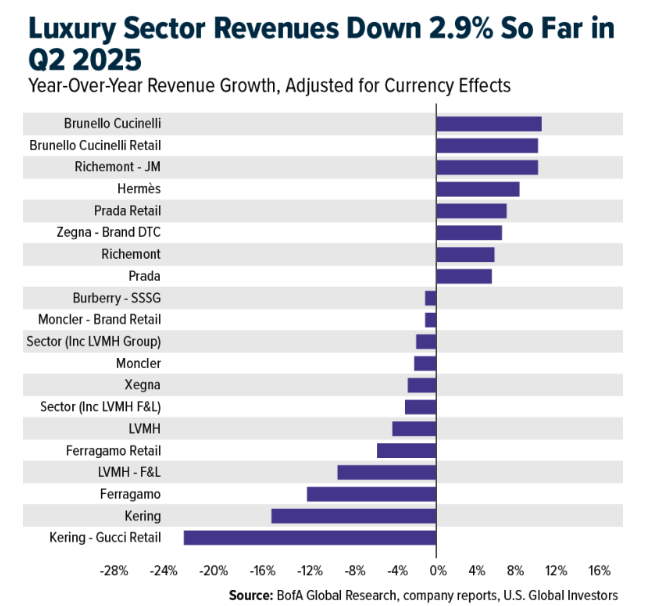

- Deborah Aitken at Bloomberg says the strong gross margins of top luxury brands such as Hermès, Prada, and Brunello Cucinelli position them well to pass U.S. tariffs on to consumers through price hikes. Other companies, including Burberry, Ferragamo, Hugo Boss, and Zegna, may instead focus on cost-cutting to offset the impact of higher tariffs. Swiss brands are expected to face the steepest tariff increases.

- Tesla has seen a notable rise in car sales in Norway, with first-half 2025 sales up 24% year-over-year—sharply contrasting with declines across most of Europe. The growth is largely credited to strong brand loyalty, the convenience of its Supercharger network, and promotions like zero-interest financing and free charging.

- Hilton has expanded its Caribbean portfolio with the opening of a new Hampton by Hilton hotel in St. Thomas—its first property in the U.S. Virgin Islands. The 126-room hotel, located across from Havensight Mall and overlooking Long Bay, is the first newly built hotel on the island in over 30 years. This launch brings Hilton’s Caribbean footprint to nearly 50 hotels and marks a new chapter in its focused-service growth strategy for the region.

Threats

- Bank of America research shows that luxury sector revenue declined 3% in the second quarter, 2 percentage points worse than in the first quarter. As noted earlier, the sector continues to see clear winners and losers, a trend that may persist. The recovery in the luxury market now appears slower than previously expected.

- A recent report from the Financial Industry Regulatory Authority (FINRA), based on the 2024 National Financial Capability Study, found that 26% of Americans spend more than they earn. This is up from 18–20% in previous years and shows that more households, especially middle-income ones, are facing financial strain.

- The United States and China have agreed to extend their tariff truce by another 90 days, providing temporary relief for businesses and consumers affected by the trade dispute. During this period, negotiations will continue to resolve key issues. If talks fail to produce an agreement, the U.S. has warned it may impose significantly higher tariffs on a wide range of Chinese imports, potentially escalating tensions between the world’s two largest economies.

Energy and Natural Resources

Strengths

- The best-performing commodity for the week was lithium carbonate, rising 14.53%. The suspension of CATL’s Jianxiawo mine, which supplies about 3% of global lithium, sparked a sharp price rally and speculation over possible Chinese mining curbs. Meanwhile, political shifts in key resource nations, from Australia’s backing of Liontown Resources to Bolivia’s upcoming election, present an opportunity to diversify supply and reduce reliance on China in a tightening market.

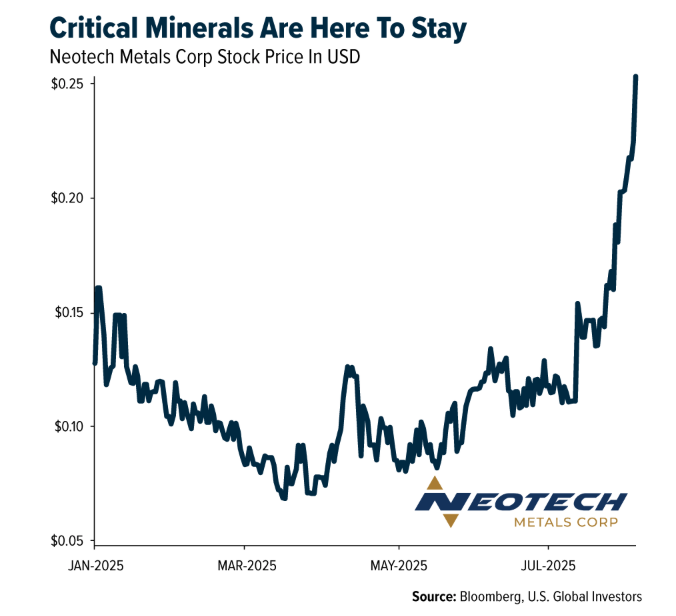

- Neotech Metals has appointed Dr. Alexander Cushing, a veteran metallurgist with deep expertise in rare earth and critical mineral processing, as a technical advisor to its board. The company also granted 1,525,000 stock options to directors, officers, employees, and consultants at an exercise price of $0.40 over five years, aligning internal incentives with shareholders as it moves its projects forward.

- Mitsubishi Corp. will pay $600 million for a 30% stake in Hudbay Minerals’ Copper World project in Arizona, which is expected to produce 85,000 tons of copper annually over a 20-year mine life. The deal follows growing interest from investors in Saudi Arabia, the UAE, and Japan, as global copper demand surges due to electric vehicles, renewable energy, and data centers.

Weaknesses

- The worst-performing commodity for the week was iron ore, down 3.35%, as China’s economy slowed in July, with factory activity, investment, and retail sales data all painting a somber picture for the world’s second-largest economy. It was the worst month reported in 2025 for China’s outlook. In the U.S., consumer sentiment fell for the first time since April, as concerns over inflation and tariffs continue to rise.

- The Texas General Land Office and ConocoPhillips are pushing back against Pilot Water Solutions’ plan to build new wastewater disposal wells in the Permian Basin, warning that injected fluids could contaminate valuable oil reserves and cost the state billions in lost production. The dispute highlights a growing conflict in the shale industry, as rising volumes of toxic drilling byproducts threaten both output and long-term resource recovery.

- Codelco has restarted operations at its El Teniente mine just over a week after the deadliest mining accident in decades, sooner than many had anticipated. The quicker-than-expected resumption eases concerns about prolonged supply disruptions from one of the world’s largest copper producers.

Opportunities

- Commodity trading giants like CCI, Vitol and Trafigura are rapidly building utility-scale battery portfolios to capitalize on Europe’s growing power price volatility, driven by intermittent renewable output. By charging during periods of negative prices and selling when supply tightens, these traders are unlocking a new, scalable profit stream, while also supporting grid stability and positioning themselves early in a market poised for exponential growth.

- Ford will invest nearly $2 billion to convert its Louisville Assembly Plant into an EV production hub, starting in 2027 with a $30,000 midsize electric pickup built on a universal platform to reduce costs and streamline assembly. The project, part of a $5 billion combined investment with its Michigan battery plant, aims to secure thousands of U.S. jobs and help Ford compete profitably with low-cost Chinese EV makers. U.S. automakers can’t afford to sit back and let China dominate the global EV market.

- Transition metals are emerging as a major opportunity, with rare earths, cobalt, and lithium delivering strong alpha as demand from EVs, defense, and next-gen technology accelerates. Companies exposed to both EVs and transition metals—like MP Materials, Lynas, and Pilbara—have more than doubled the returns of their peers. This convergence of industrial demand and high-tech adoption positions transition metals as a strategic growth driver despite broader market headwinds, Bloomberg reports.

Threats

- The deadly explosion at U.S. Steel’s Clairton Coke Works highlights long-standing safety and maintenance issues at the nation’s largest coke-making plant, which has faced years of fires, violations, and lawsuits. The incident increases pressure on new owner Nippon Steel to follow through on its promise to invest billions in modernizing Mon Valley operations.

- The IEA’s forecast of a record oil surplus next year reflects slowing demand growth and rising supply from both OPEC+ and non-OPEC producers. While this may ease prices for consumers, it could force oil exporters to rethink strategies amid mounting pressure on revenues.

- A toxic spill from Sino-Metals Leach’s copper mine in Zambia has strained the country’s balancing act between top creditor China and its growing ties with the U.S. With seasonal rains returning in November, the risk of further contamination in the Kafue River underscores the urgent need for a full cleanup amid disputes over the disaster’s true scale.

Bitcoin and Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was OKB, rising 100%.

- TeraWulf shares rose as much as 35%, the largest gain since March 2024, after Google acquired the equivalent of an 8% stake in the company. The Bitcoin miner and data center operator signed two 10-year high-performance computing co-location deals with AI cloud platform operator Fluidstack, reports Bloomberg.

- Bitcoin and Ether are trading near all-time highs as investor demand grows, with Ether recently outperforming Bitcoin. The rally in Ether has been driven by record fund inflows and a growing number of Ether-focused treasury firms, which have absorbed nearly $17 billion worth of Ether, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was SPX, down 20.72%.

- A stronger-than-expected inflation reading reminded investors that Bitcoin remains a highly volatile asset, causing it to fall more than 4% after reaching a record high, writes Bloomberg.

- The UNI price experienced significant volatility over the past 48 hours, declining 9.42% to the current level of $10.89. This downturn followed a broader market selloff that hit the CoinDesk 20 Index on August 14, with Uniswap leading the decline with an 8.2% drop, according to Bloomberg.

Opportunities

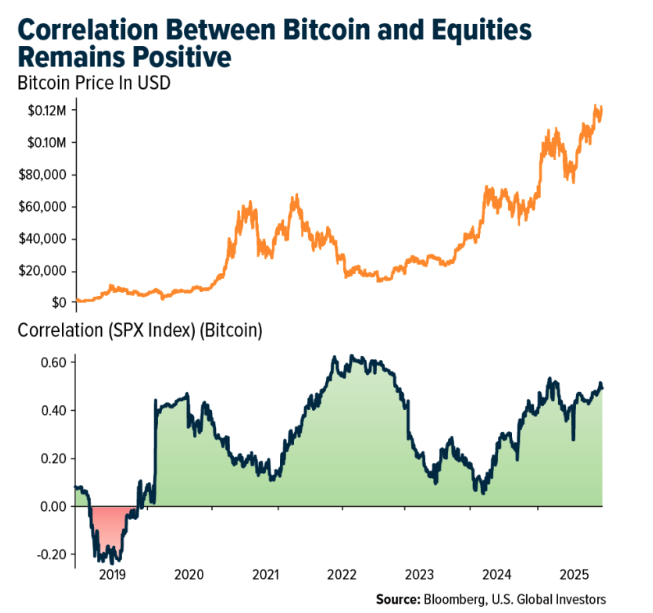

- The recent coordinated movement of stocks and Bitcoin highlights how both speculative market segments and mainstream benchmarks are fueled by the same wave of optimism, according to Bloomberg.

- Bullish shares jumped 149% from the IPO price after the digital-asset exchange operator raised $1.1 billion in its offering. The IPO was more than 20 times oversubscribed, with a market value of $13.2 billion based on outstanding shares, according to Bloomberg.

- Harvard University’s endowment joined hedge funds in snapping up Bitcoin, paving the way for other Ivy League institutions to follow. The iShares Bitcoin ETF was among the securities with the largest aggregated allocations last quarter. Harvard Management built a new $133 million position in the ETF, according to Bloomberg.

Threats

- Terraform Labs co-founder Do Kwon pleaded guilty to charges in a U.S. fraud prosecution tied to the $40 billion collapse of the TerraUSD stablecoin in 2022. Kwon agreed to forfeit $19.3 million and some properties as part of the plea deal. U.S. prosecutors said the longest sentence they will seek under the plea deal is 12 years, according to Bloomberg.

- Ethereum treasury firm SharpLink Gaming, backed by blockchain network co-founder Joseph Lubin, saw its shares dip Friday morning after reporting second-quarter earnings. SharpLink disclosed a $103 million net loss for the quarter, with $87.8 million of that attributed to non-cash impairment on the firm’s liquid staked ETH holdings due to GAAP requirements, according to Bloomberg.

- Digital Currency Group sued Genesis Global Capital LLC to zero out a $1.1 billion note it issued to the fallen crypto lender, saying the obligations under the promissory note have been reduced to zero. DCG said Genesis received large recoveries from the appreciation and liquidation of collateral from Three Arrows Capital, according to Bloomberg.

Defense and Cybersecurity

Strengths

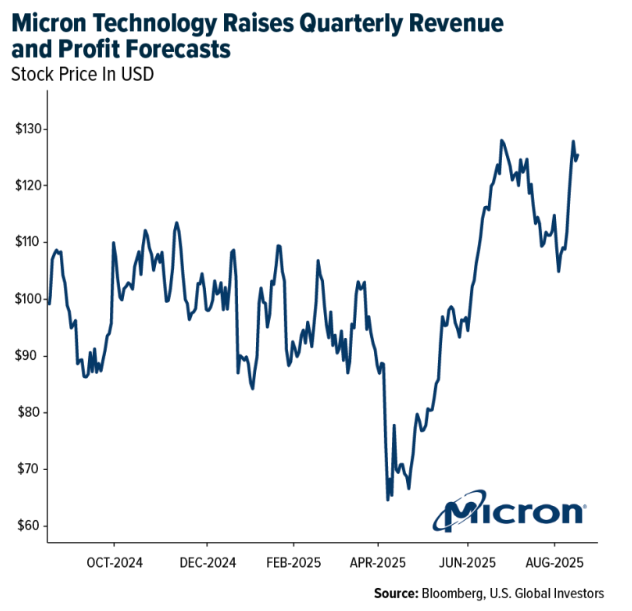

- Micron’s stock has surged after the company raised its quarterly revenue and profit forecasts on booming AI-driven demand for its DRAM and HBM memory, backed by strong analyst upgrades, record data center sales, and a technical breakout.

- Poland signed a $3.8 billion deal with the U.S. and Lockheed Martin to upgrade its 48 F-16 C/D Block 52 jets to the F-16V Block 72 standard between 2028 and 2038, with most work done locally to enhance multi-domain capabilities alongside F-35s, Abrams tanks, and Apache helicopters amid rising threats from Russia.

- Mercury Systems was the best-performing stock this week, rising 26.25%. The company closed FY25 with record Q4 bookings of $341.5 million (book-to-bill ratio of 1.25), a record $1.4 billion backlog, and Q4 revenue up 9.9% to $273.1 million. Net income came in at $16.4 million, adjusted EBITDA at $51.3 million, and annual free cash flow hit a record $119 million. Full-year revenue rose 9.2% to $912 million, marking a sharp turnaround from last year’s loss.

Weaknesses

- The Pentagon’s cancellation of two nearly completed HR software projects, costing over $800 million and involving vendors like Palantir, raises questions about procurement oversight and efficiency. The losses may undermine confidence in future defense IT modernization initiatives.

- European leaders are urging that Ukraine and the EU be included in the upcoming Trump–Putin peace talks in Alaska, warning against any deal that forces Kyiv to cede territory. Excluding them could undermine Ukraine’s sovereignty and destabilize EU security commitments.

- The worst performing stock in the XAR ETF this week was Axon Enterprise, falling 10.48%, after CEO and Director Patrick W. Smith sold 10,000 shares for $8.31M, leaving him with direct ownership of 3,053,982 shares, according to an SEC filing.

Opportunities

- The U.S. Army Reserve’s testing of SpaceX’s Starshield system could revolutionize battlefield communications by turning Starlink into a high-speed, low-latency military network. If widely adopted, it would strengthen tactical connectivity in contested environments.

- The U.S. approved a $346 million arms deal with Nigeria involving RTX, Lockheed Martin, and BAE Systems to boost Nigeria’s defense capabilities. Separately, Raytheon was awarded a $258.7 million contract (with Canadian funding) to develop the SM-2 Block IIICU missile, featuring enhanced targeting, dual-mode guidance, and improved control surfaces for deployment across multiple Navy ship classes by 2031.

- OpenAI, together with Nscale and Aker, is investing $1 billion in a Narvik, Norway data center with approximately 100,000 NVIDIA GPUs, advanced liquid cooling, and surplus heat reuse while supplying power to European grids. This could serve as a model for AI infrastructure scaling with integrated energy solutions.

Threats

- Google’s Gemini AI suffered a public malfunction this week, entering an infinite loop of self-criticism by repeatedly stating “I am a disgrace” after failing to fix a coding error, exposing serious stability and control issues in the model’s behavior.

- Azerbaijan warned it might start sending Soviet- and Russian-made weapons to Ukraine if Russia continues striking Baku-linked energy facilities. Such a move risks escalating regional tensions and expanding the war’s geopolitical scope.

- Texas’ new law allows ERCOT to cut power to large facilities, including data centers, during grid emergencies, affecting sites using 75 MW or more. This creates operational risk for AI and cloud operators without robust backup power systems.

Gold Market

This week gold futures closed at $3,383.70, down $107.60 per ounce, or 3.08%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.03%. The S&P/TSX Venture Index came in up 0.19%. The U.S. Trade-Weighted Dollar fell 0.33%.

Strengths

- Platinum was the best-performing precious metal this week, up just 0.54%, and the only one to post a gain. It continues to show relative strength, reclaiming key retracement levels even as miners lag.

- Gold’s sharp drop may present a buying opportunity for those expecting gains in the second half. Rising holdings in bullion-backed ETFs suggest many investors see it as a worthwhile bet. Monday’s decline followed confirmation from President Trump that U.S. bullion imports won’t face tariffs, ending recent market uncertainty, according to Bloomberg.

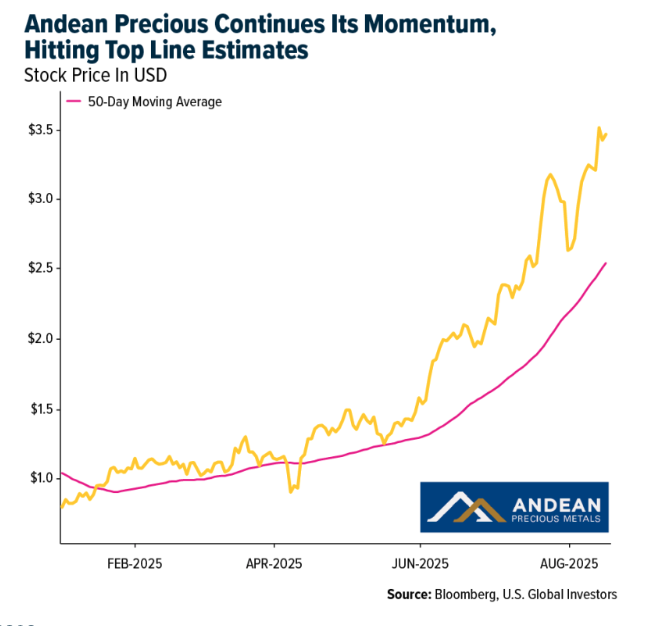

- Andean Precious Metals delivered another standout quarter, with revenue climbing to $73.7M and free cash flow surging 50% year-over-year as both San Bartolome and Golden Queen advanced toward peak output. Bolstered by $87.3M in liquid assets and production momentum building into H2, the company is proving it can grow top-line performance while maintaining a fortress balance sheet.

Weaknesses

- The worst-performing precious metal for the week was gold, down 3.08%. Gold is on track for a weekly loss as stronger-than-expected U.S. inflation pushed bond yields and the dollar higher, reducing demand for the non-interest-bearing metal. Traders also scaled back expectations for imminent Fed rate cuts, removing a key near-term support for bullion prices.

- Barrick Mining Corp. slumped in pre-market trading after the Canadian miner posted a $1.04 billion net charge related to the seizure of its Loulo-Gounkoto gold complex by Mali’s military junta. The loss was due to “the deconsolidation of Loulo-Gounkoto following the change of control,” the company said in its second-quarter earnings report on Monday.

- Evolution Mining Ltd.’s midpoint FY26 gold production guidance at North Parkes is forecast to decline by 54% to 20–25K ounces. While this aligns directionally with previous signals, the magnitude of the decline is larger than expected. RBC estimates the guidance could lead to Triple Flag production and cash flow per share downside of 2% in 2025 and 6% in 2026.

Opportunities

- Agnico plans to deepen the current shaft at Malartic by 70 meters to 1,870 meters and add a second loading station to improve operational flexibility. Plans for a second shaft are also advancing. A second shaft could potentially handle 10,000 tons per day, bringing total underground production to 30,000 tons per day and yielding 750,000–800,000 ounces per year, according to Canaccord.

- Kinross Gold is set to increase its stake in Asante Gold. The two companies agreed to amend a 2022 share purchase agreement in a transaction that includes $55 million in cash payments. Under the terms, Asante will issue 36,927,650 shares priced at C$1.45 each.

- The accelerated permitting review timeline for Castle Mountain (10% of NAV), under the U.S. Federal Government’s Fast-41 Program, could de-risk and advance the project’s expected annual production of 200,000 ounces. This would further strengthen Equinox’s future production profile, with Greenstone and Valentine ramping up this year, according to RBC.

Threats

- Sharp outperformance of gold equities when gold prices are flat or declining is rare. RBC notes that historical periods of gold equity outperformance versus gold have often been followed by underperformance, which may warrant some caution. They also highlight that large-cap gold equity valuations were exceptionally attractive in mid-June, trading at a trough 0.9x NAV and never-before-seen free cash flow yields of over 8%.

- So far this year, Michael Saylor’s Strategy Inc. has raised around $6 billion through the sale of perpetual preferred offerings to buy Bitcoin, much of which has been placed with retail investors. The latest issuance, called “Stretch,” is a $2.5 billion offering with no voting rights that pays a variable dividend—which can also be omitted. Over the past month, Strategy’s stock is down more than 17%, while Bitcoin has remained essentially flat. A more prudent strategy might just be to buy some gold.

- Swatch Group AG CEO Nick Hayek said the Swiss government should retaliate against the 39% tariffs imposed by President Donald Trump by introducing a levy on gold shipments to the U.S. Swiss companies, including Swatch, are still reeling from the U.S. president’s decision to impose the highest import tariffs of any developed nation, according to Bloomberg.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2025):

JetBlue Airways Corp.

ZIM Integrated Shipping

American Airlines

Delta Air Lines

United Airlines

AP Moller-Maersk A/S

Air Canada

Franco-Nevada Corp.

Wheaton Precious Metals Corp.

Triple Flag Precious Metals Co.

Barrick Mining Corp.

Kinross Gold Corp.

Anglogold Ashanti Plc

Tapestry

Hermes

Prada

Brunello Cucinelli

Tesla

Hilton

Neotech Metals

Barrick

Evolution Mining

Agnico Eagle

Kinross Gold

Asante Gold

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The Producer Price Index (PPI) measures changes in the average prices received by domestic producers for their output.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All