The emergence of private credit as a substantial asset class presents an opportunity for investors to pursue enhanced returns and portfolio diversification. The quality of the loans being underwritten is the key determinant of long-term performance, but other factors can have a large impact too. For instance, marketplace pressures arising from fierce competition amongst lenders could cause a deterioration of underwriting standards, particularly during periods of irrational exuberance. To borrow an example from wine making - the soil and seeds are critical in producing top quality grapes, but so are the weather conditions during the time of growth. A combination of warm days and cool nights often produce the most stellar vintages of wine. Similarly, the right combination of fiscal conditions and marketplace technicals can also result in a vintage of private credit loans that are a cut above the rest. ‘Vintage’ in this context refers to the year in which a loan or investment is originated. This paper will examine the critical role of vintage selection in private credit investment performance, through the lens of recent market experiences, focusing specifically on the contrasting characteristics of the 2021 and 2022 vintages. By exploring these case studies and discussing best practices, this paper aims to provide valuable insights to navigate the complexities of the private credit market effectively.

The role of vintage selection in private credit

Selecting the right vintage can be the difference between a robust return profile and a lackluster one. While the middle-market direct lending landscape is generally perceived as a lower-risk environment with steady returns, the non-accrual rate of loans from 2021 serves as a reminder that not all vintages are equally promising. Sharper scrutiny and a more nuanced approach to vintage selection are warranted in light of these findings

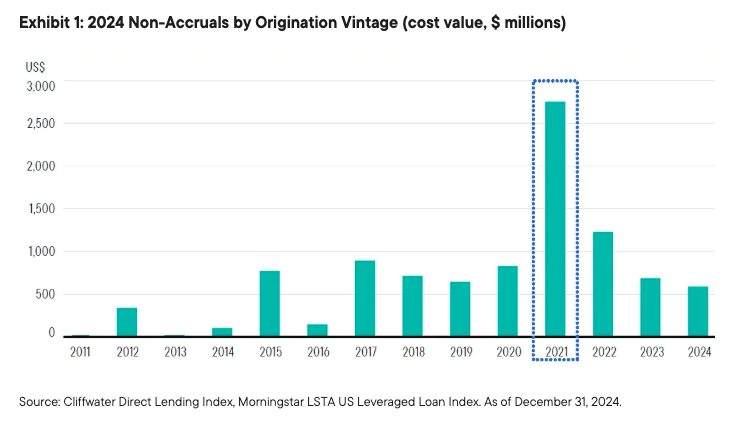

Non-accruals by origination vintage

Examining non-accruals by origination vintage offers insights into the risks of loan originations by period. As of December 31, 2024, the 2021 vintage had the highest non-accruals by a wide margin, totaling about $2.8 billion. This relatively high level of non-accruals suggests that loans originated during this period have an elevated risk of credit loss. For newer funds that avoided the landmine of 2021, this may result in a superior return profile, as they have sampled investments from better vintage years.

The 2021 vintage: A case study

The 2021 vintage is a prime example of the increased risks during certain periods. Policy makers responded to the global pandemic with a range of economic measures to prop up the economy. This ranged from easing monetary policy via rate cuts, to generous fiscal policy via direct stimulus checks and loan forgiveness programs. Economic conditions felt like being on the set of Oprah’s Christmas show, with the host bellowing “You get a car! You get a car! Everybody gets a car!” Except “car” was replaced with “loans with excessive leverage, bad covenants, and rock bottom rates”.

It is worth doing a deeper dive into the perfect storm of factors that led to bad loans being underwritten in this period.

The biggest driver was the Federal Reserve’s decision to cut the policy rate to zero, which incentivized companies to go on a borrowing binge. Compounding this was the decision to do Quantitative Easing (QE), whereby the Fed expanded its balance sheet by purchasing government debt, which lowered rates across the yield curve. Lenders and investors were eager to lend money as the opportunity cost of holding cash in risk-free assets was very high - any capital you had raised was now burning a hole in your pocket if you were earning almost nothing by parking it at the bank or buying treasuries. The natural consequence of this was that underwriting standards weakened, as there was a race to the bottom to deploy money. Loose covenants, creative EBITDA addbacks, and elevated leverage multiples became commonplace. Lenders tried to compensate for this increased risk by charging more of a spread on these loans, but due to base rates being zero, the overall cost of financing was the cheapest it had been in many years. Marginal companies that would otherwise not have access to debt markets were now able to borrow freely.

Another key factor was the decision by the administration to use a policy tool that economists sometimes call “helicopter money”. The metaphor of a helicopter doing cash drops over a city is used to approximate the idea of a direct cash transfer to consumers without any strings attached. Multiple stimulus checks were sent to everyone as part of this policy. Consumers, now flush with cash, started spending like drunken sailors. This spending artificially inflated the revenues and EBITDA for many companies, particularly in the consumer discretionary space. Oftentimes companies were just pulling forward to the current year those revenues that would have come in future years. Or, in the case of leisure companies, they were experiencing a surge from “revenge travel” - a phenomenon where consumers were making up for lost time during the lockdowns by taking more vacations. In either case, companies were experiencing a temporary sugar rush of increased revenues and EBITDA. Unfortunately, many lenders treated this temporary surge as evidence of a permanently higher growth trajectory, and provided financing based on lofty assumptions. Leverage levels were also elevated, as interest costs were low in a zero-rate environment and lenders did not underwrite rates going up too much.

The final element of this perfect storm was the Russian invasion of Ukraine in February 2022. This immediately snarled supply chains that were still recovering from Covid, and were now thrown into disarray again. The bottlenecks led to a spike in inflation, with CPI hitting a level of 9.1% in June 2022. Inflation was already trending up due to all the excessive money printing in 2021, but the Ukraine invasion added fuel to the fire, and the Federal Reserve was forced to raise rates in an attempt to tame this runaway inflation. This series of rate hikes in 2022 caused the inevitable crash after the 2021 high.

The crash came as economic conditions tightened rapidly, and companies were hit with a double whammy of normalizing revenues in a slowing economy, and suddenly higher interest costs due to higher base rates. As a result, many companies found it difficult to cover the interest payments on the money they borrowed in 2021, which is why that cohort of loans has a much higher default rate than prior and subsequent cohorts.

This example underscores the need for new funds to carefully navigate periods of economic upheaval, particularly when market conditions are a toxic brew of froth, excess, and complacency.

Great opportunities in turbulent times: The case of 2022

The flip side of having a bad vintage is that the subsequent periods can have outsized returns, as the markets overcorrect in the other direction. 2022 is the perfect example of this. The Russian invasion of Ukraine led to pain for loans that were already outstanding but also created an opportunity for new loans that reflected the new reality and were priced appropriately.

When Russia invaded Ukraine, large global banks found themselves caught in a bind as they had underwritten deals in the prior months which were still warehoused on their balance sheets, waiting to be syndicated and transferred to other lenders. This is the normal ebb and flow of deal making - big banks provide financing for M&A deals, which are long drawn-out processes, and they subsequently distribute those loans to other participants in the loan market (such as CLOs and Loan Mutual Funds). Crucially, if there is an economic dislocation while the banks are still holding on to the loans, they could be “hung” with them, i.e. they will have to take a loss to sell them to other investors and clean up their balance sheets. This is what happened in 2008, during the Great Financial Crisis. 2022 was a replay of that, albeit on a much smaller scale.

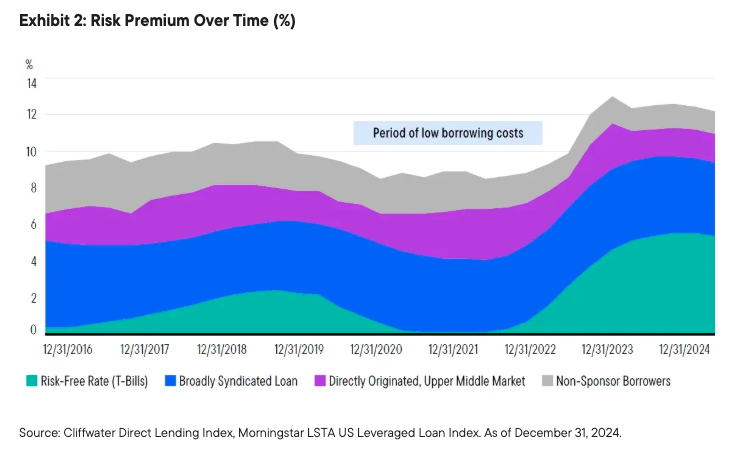

With the Russian invasion, risk premia were reset overnight, and suddenly banks found themselves taking a hit to their balance sheets. When this happens, banks will often pull back from providing new financing as they rebuild their capital buffers. Which is precisely what happened in 2022. The bank pull back created a vacuum in the market, and private credit stepped in to fill it. With no competition in sight, direct lenders were able to dictate terms and lend at very attractive rates.

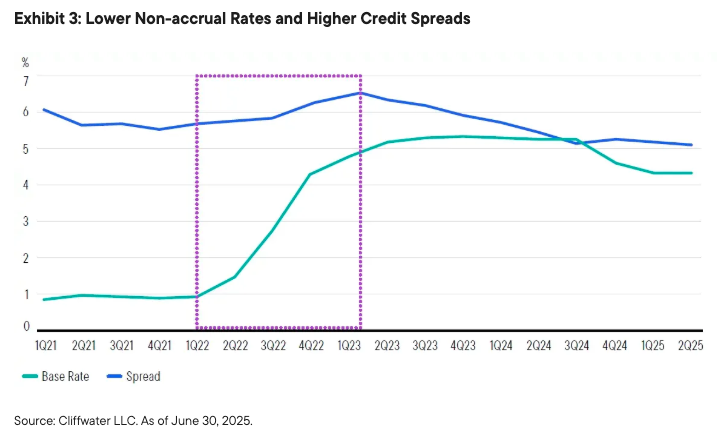

In the context of vintage selection, 2022 stands out as a year where the right timing and strategic investment choices in turbulent times could yield substantial benefits. The lower non-accrual rates and higher credit spreads indicated a more resilient and potentially higher-returning portfolio.

Best practices for vintage selection

To optimize vintage selection, investors should follow these best practices:

-

Diversification: The strategy here is to spread risk across various vintages, capturing the strengths of different economic cycles. This prudent approach can lessen the impact of an underperforming vintage.

-

Thorough Analysis: Conduct thorough analysis of economic conditions, market trends, and borrower quality for each vintage. Utilize a combination of quantitative and qualitative data to make informed decisions.

-

Risk Management: Establishing vigorous risk management protocols is essential for identifying and addressing risks linked to distinct vintages. This encompasses stress testing and scenario analysis, illuminating how loans could fare under varied economic landscapes.

-

Long-Term Perspective: When it comes to private credit, it is wise to take a long-term view. By resisting the urge to react to short-term market flux, one can better position themselves to capitalize on the potential benefits private debt can offer across market cycles.

Manager selection: A complementary strategy

While the selection of vintage is paramount, it is not the sole consideration for investors in private credit. Manager selection is equally crucial to the success of these investments. A manager with the right expertise can skillfully navigate the complexities of the private credit market, identifying high-quality loan opportunities through extensive proprietary networks and close relationships while managing risks astutely. Investors should assess the manager’s historical performance, including their adeptness in navigating various economic cycles and their track record of mitigating non-accruals. Additionally, evaluating the manager’s risk management strategies, such as their underwriting approach, portfolio diversification, and stress testing practices, is essential. Ensuring that the manager provides clear and transparent communication about their investment strategies and portfolio performance is critical for building trust and making informed decisions.

Conclusion

The selection of vintage is a critical factor in private credit investing, significantly impacting the risk and return profile of the investment. The 2021 vintage serves as an example of how a high level of non-accruals can change the risk profile of a fund. Conversely, the 2022 vintage showed how leaning in during the right period can also lead to alpha generation.

Just as a winemaker needs to play close attention to the weather conditions, private credit managers need to focus on the financial conditions during a fund’s investment period. Skilled managers know when to dynamically deploy more capital or pull back, as the weather changes.

Terms:

Non-Accruals: Non-Accruals are unsecured loans no longer generating its stated interest rate because no payment has been made by the borrower for 90 days or more.

EBITDA: EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization, representing a company's profitability before considering non-operating expenses and accounting adjustments.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

Investments in many alternative investment strategies are complex and speculative, entail significant risk and should not be considered a complete investment program. Depending on the product invested in, an investment in alternative strategies may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. An investment strategy focused primarily on privately held companies presents certain challenges and involves incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity.

Diversification does not guarantee a profit or protect against a loss.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

WF: 6426658

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Franklin Templeton

Read more commentaries by Franklin Templeton