The year to date has been complicated by a cloud of uncertainty as a new U.S. administration took the world economy by storm. Over the past month, U.S. policy has settled into a steadier state. The outlook for global markets is becoming somewhat clearer. There are still ongoing negotiations and outstanding issues to be resolved, but the trade landscape is better defined.

Trade restrictions will be a consideration for the foreseeable future, weighing on the outlook for all nations. Consumption across the world has slowed; no advanced economy is thriving. Exporters may struggle to replace a reliably eager U.S. consumer market.

Most markets have escaped recession in the year to date, and lower volatility is a favorable omen for continued growth. But lower demand and higher costs raise the specter of stagflation.

Following are our thoughts on how top markets are faring.

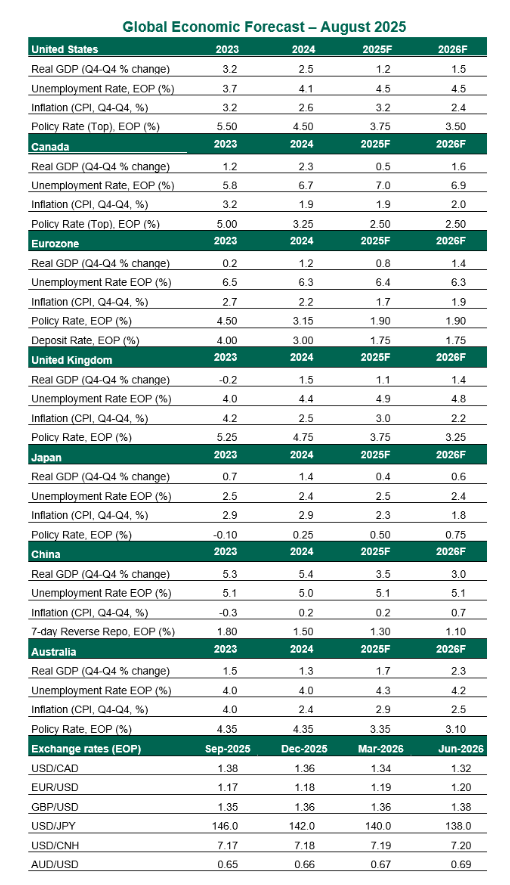

United States

- After a years-long stretch of outperformance, the U.S. economy has faltered in the past month. The weak job creation and significant downward revisions in the July employment report illustrated a stagnating labor market. The Consumer Price Index (CPI) for July showed firming prices for import-intensive goods, though a cooling housing market is helping to keep overall inflation contained.

- The slower labor market clears the way for the Federal Reserve to resume rate cuts. The Fed had the luxury of waiting for inflation to heal as the rest of the economy held up well; if the job market is no longer thriving, support through lower rates is justifiable. At his highly-anticipated Jackson Hole keynote speech, Fed Chair Powell conceded a shifting balance of risks and expressed hope that tariff-driven inflation would be a one-time event. We now expect rate reductions at the next three meetings. However, inflation remains too stubborn for a prolonged or steep easing cycle.

Australia

- Australia’s economy continues to hold steady amid an uncertain global context. Unemployment has arrested its rise, and incomes are gaining, though the outlook for job creation is mixed. Combined with lower taxes and falling interest rates, domestic demand should remain sufficient to support growth, but not to a heightened extent that could renew a cycle of inflation. Although Australia’s direct exposure through trade with the U.S. and manufacturing supply chains is low, a global slowdown or crackdown on transshipment could have implications for Australia through its impact on its trading partners.

- With inflation calming, the Reserve Bank of Australia (RBA) cut rates again at its August meeting. With consumer price inflation most recently registering 2.1%, near the low end of the RBA’s target, we expect limited further easing. Current rates leave ample room for the RBA to ease further if external conditions deteriorate.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Northern Trust

Read more commentaries by Northern Trust