Markets are currently pricing in a Goldilocks scenario. Investors believe tariffs will not compress corporate margins, inflation is contained, labor markets will soften just enough to allow rate cuts without triggering a recession, and AI will drive an acceleration in productivity. As the Reddit crowd would say, “stonks to the moon.”

We think that perfect outcome is a low-probability scenario and that the market is too optimistic that earnings growth will remain strong as the Fed cuts rates. In fact, history suggests if the Fed were to ease policy significantly amid strong growth, it could go down as one of the Fed’s great policy blunders. The last time the Fed cut rates into a profit acceleration was September 2024, and the 10-year yield subsequently rose 120bps and the equity market plummeted. Rate cuts only help markets if they fall below neutral (and are stimulative) or coincide with strong earnings growth AND low inflation. Neither is likely in the coming months. The truth is far less exciting. We’re deep into an economic expansion, labor markets are weakening, margins are under pressure, and inflation is sticky. Investors can’t have it all.

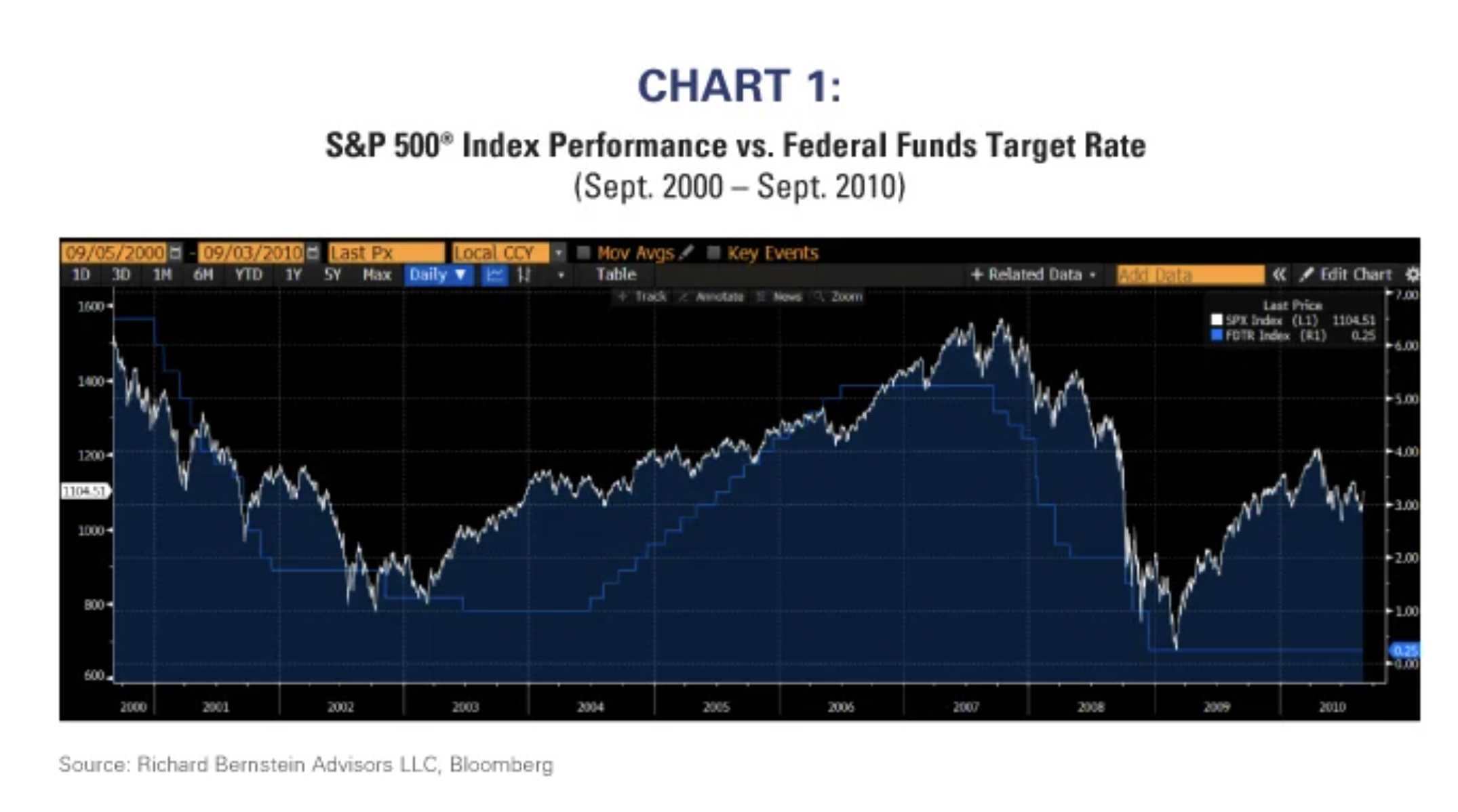

The Fed typically cuts rates during profits slowdowns, and the market falls during the initial rate-cuts. Take 2001 and 2007 as classic examples where rate cuts came well before any sustained market recovery. The Covid period, of course, was a significant outlier, and even then, the S&P 500® fell 34% before policy support finally took hold.

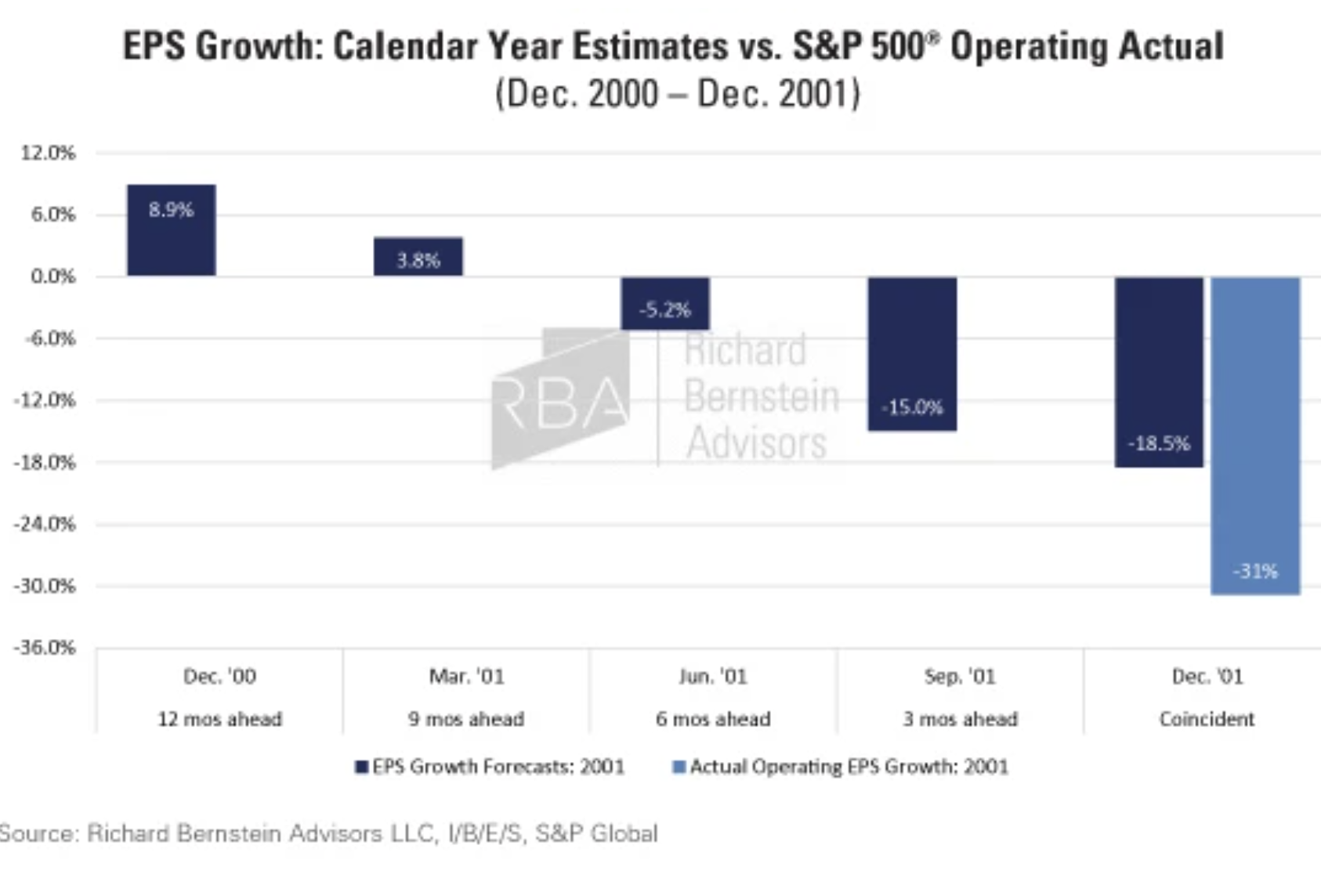

Analysts nearly always overestimate earnings heading into slowdowns and this time is unlikely to be different. Slowing earnings, rising odds of Fed cuts, and weakening employment aren’t the ingredients of a bull market — they’re classic signs of stress that create opportunities in overlooked areas of the market.

Certainly, if the Fed cuts rates, inflation falls, and earnings growth accelerates, then markets could go “to the moon.” However, given the low probability of a Goldilocks outcome and investors’ willingness to take substantial portfolio risk, we recommend emphasizing high-quality, dividend-paying equities, increasing regional diversification, and avoiding corporate credit exposure.

Michael Contopoulos, Deputy Chief Investment Officer

A message from Advisor Perspectives and VettaFi: Prepare your bond portfolio for changing market conditions. Register today for the Fixed Income Symposium on Sept. 18, 2025, 11AM ET / 8AM PT.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially and should not be relied upon as such. The investment strategy and broad themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided "as is" without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by employees of Richard Bernstein Advisors, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Graphs, charts, and tables are provided for illustrative purposes only. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.