Takeaways

-

A surprisingly weak August jobs report has locked in expectations for a Federal Reserve rate cut next week, shifting all market focus to this Thursday's key inflation (CPI) report

-

Consumer behavior is again in focus this week, with Kraft-Heinz announcing a major spinoff due to shifting preferences

-

Key earnings from Kroger and Restoration Hardware set to reveal the strength of spending on both essentials and larger ticket items

Labor Market Falters, Pushing Fed Rate Cut Probability to 100%

Last week's employment update seems likely to prompt a shift in the Federal Reserve's monetary policy. The August jobs report revealed a significant slowdown, with Nonfarm Payrolls (NFP) increasing by only 22,000, well below the 75,000 expectation from economists surveyed by Dow Jones. This pushed the unemployment to 4.3%, the highest rate in over a year.1

Worker confidence has taken a hit as well. The New York Fed’s August Survey of Consumer Expectations showed participants on average believed they had a 44.9% probability of finding another job if they lost their current one, the lowest reading in the survey’s history going back to 2013.2

Despite dismal labor market news, equity markets have been hanging in there, even moving higher in some instances, as worse-than-expected jobs data all but guarantees a rate cut at next week’s FOMC meeting. Since the release of the August NFP report, the CME Group’s FedWatch tool now shows a 100% probability of a rate cut on September 17. And while a majority of the interest rate traders polled are expecting a 25 basis point cut (88.2%), a new group has emerged that is expecting a 50 bp cut (11.8%).3

One other thing that could sway rate cut probabilities is the August Consumer Price Index (CPI) report this Thursday. Inflation has remained hot, and the Fed has tried to balance the risks brought about by high inflation, and now a weakening employment situation. At his annual Jackson Hole speech a couple of weeks ago, Federal Reserve Chairman Jermone Powell sounded slightly more dovish than usual. “With policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance,” Powell said. He noted that while the US labor market remains resilient, those risks are creeping up, as are the risks of tariff inflation.4

Unraveling a Merger: Kraft-Heinz Announces Spinoff After Years of Struggle

Last week also saw one of the biggest spinoff announcements in recent history. Consumer Staples giant, Kraft-Heinz, announced on Tuesday their intention to split into two independent, publicly traded companies.5 Investors weren't happy, initially taking the stock down 7%, but settling to a decline of 2.4% by market close on Friday.

Someone else that wasn’t happy was legendary investor Warren Buffet, as his Berkshire Hathaway owns a 27.5% stake in the company. In fact, Buffet along with 3G Capital collaborated on the Kraft Food and H.J. Heinz merger back in 2015, creating Kraft Heinz. However, following the announcement of the spinoff Warren Buffett commented, "It certainly didn't turn out to be a brilliant idea to put them together, but I don't think taking them apart will fix it," in an interview with CNBC.6 The company has struggled for sometime, with shares down 13% YTD, as consumer preferences have shifted to healthier foods.

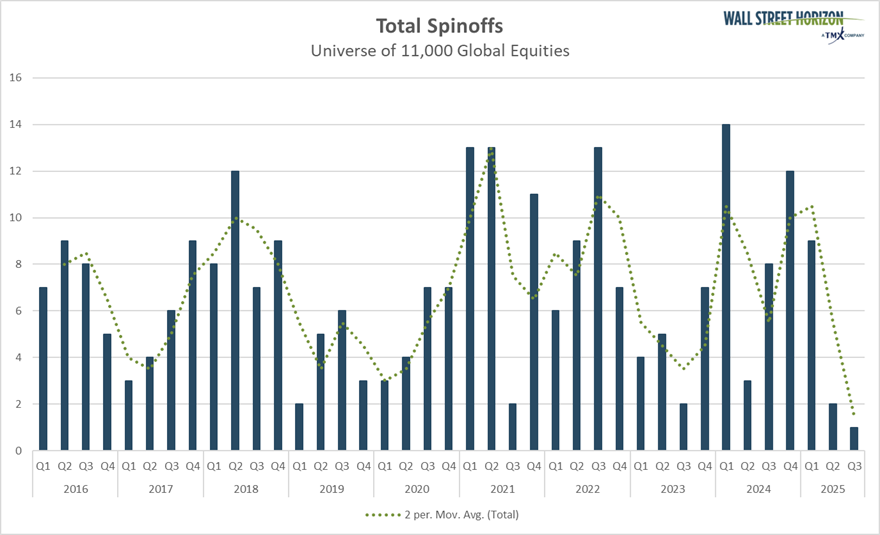

Separations like this don’t happen often. This is the only spinoff in Q3 thus far, and brings the yearly total to 12. In the last 10 years the largest number of spinoffs in a given year came in 2021 with 39, and the lowest was seen in 2023 when only 18 were announced.

Source: Wall Street Horizon

Kroger, Restoration Hardware Earnings on Deck

We’ll get another peek at how consumers are spending when Kroger and Restoration Hardware report earnings on Thursday, September 11.

Kroger has been doing well in the current environment as consumers become more value-driven. In their Q1 report, the grocer mentioned they were winning over customers that were looking for lower price points, and cooking more meals at home rather than eating out. As a result they lifted their full-year sales outlook.7 For Q2 the sell side expects Kroger to post YoY earnings growth of 6% and flat revenue growth.

Restoration Hardware is a different story. Somewhat surprisingly, the home goods and furnishings space hasn’t done as poorly as expected given the current headwinds. Higher income consumers are still shopping, and perpetually high home prices and mortgage rates mean many are staying put and instead investing in their current homes. Results from Williams Sonoma showed that last month when their EPS grew 15% YoY. Even Home Depot, which continued to see customers defer large home improvement projects in the second quarter, also noted that large ticket sales (purchases $1k and over) were up 2.6% during the quarter.

What could put a wrench in it for the likes of RH is potential tariff headwinds. Late last month, president Trump announced that he’d be investigating the furniture coming into the US, and that furniture coming from other counties would be subjected to tariff rates yet to be determined. That comment caused a sell-off in names such as Restoration Hardware, Williams Sonoma and Wayfair.

The Bottom-Line

This week promises to be dynamic, with significant macro and corporate developments. Investors should closely monitor these events —economic indicators, spinoffs, and corporate earnings—as they all have the potential to introduce market volatility.

1 August Employment Situation, US Bureau of Labor Statistics, September 5, 2025, https://www.bls.gov

2 “Short-Term Inflation Expectations Tick Up, Job Finding Expectations Reach Series Low,” Federal Reserve Bank of New York, September 8, 2025, https://www.newyorkfed.org

3 CME Group, FedWatch Tool, September 9, 2025, https://www.cmegroup.com

4 “Powell indicates conditions ‘may warrant’ interest rate cuts as Fed proceeds ‘carefully’”, CNBC, Jeff Cox, August 22, 2025, https://www.cnbc.com

5 “The Kraft Heinz Company Announces Plan to Separate into Two Scaled, Focused Companies to Accelerate Profitable Growth and Unlock Shareholder Value,” September 2, 2025, https://news.kraftheinzcompany.com

6 “Warren Buffett’s public Kraft Heinz criticism is extremely unusual for the typically passive owner,” CNBC, Alex Crippen, September 6, 2025, https://www.cnbc.com

7 “Kroger Reports First Quarter 2025 Results,” June 20, 2025, https://ir.kroger.com

Copyright © 2025 Wall Street Horizon, Inc. All rights reserved. Do not copy, distribute, sell or modify this document without Wall Street Horizon's prior written consent. This information is provided for information purposes only. Neither TMX Group Limited nor any of its affiliated companies guarantees the completeness of the information contained in this publication, and we are not responsible for any errors or omissions in or your use of, or reliance on, the information. This publication is not intended to provide legal, accounting, tax, investment, financial or other advice and should not be relied upon for such advice. The information provided is not an invitation to purchase securities, including any listed on Toronto Stock Exchange and/or TSX Venture Exchange. TMX Group and its affiliated companies do not endorse or recommend any securities referenced in this publication. This publication shall not constitute an offer to sell or the solicitation of an offer to buy, nor may there be any sale of any securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction. TMX, the TMX design, TMX Group, Toronto Stock Exchange, TSX, and TSX Venture Exchange are the trademarks of TSX Inc. and are used under license. Wall Street Horizon is the trademark of Wall Street Horizon, Inc. All other trademarks used in this publication are the property of their respective owners.

A message from Advisor Perspectives and VettaFi: Interested in learning more about how bond ETFs can help diversify your portfolio? Click here to read more.

© Wall Street Horizon

Read more commentaries by Wall Street Horizon