Gold Miners Are Striking It Rich as the World Turns to Safe Havens

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGold mining equities are having a blockbuster 2025. Prices for the precious metal have hit one all-time high after another, and the miners who pull it from the ground are rewarding investors with some of the best returns in the market today.

I’ve rarely seen such a powerful convergence of factors favoring this industry. From central bank buying to political uncertainty to disciplined corporate behavior, everything appears to be lining up for gold and the miners who produce it.

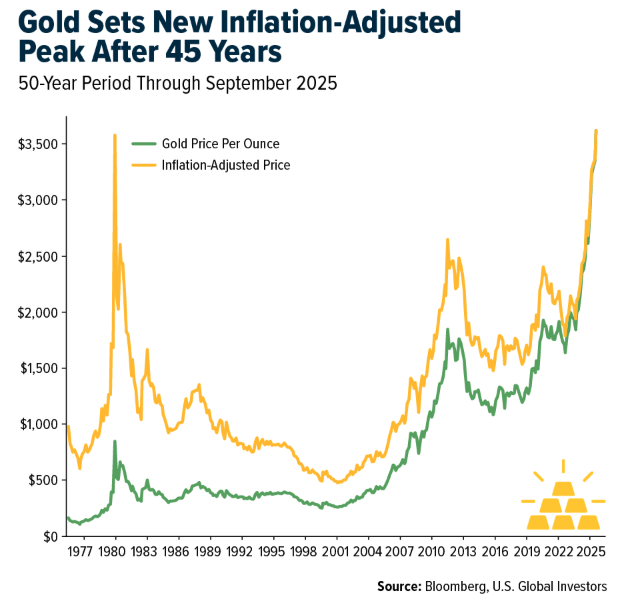

In the first week of September, the metal recorded its sixth fresh record high in just seven trading days. Having surpassed its inflation-adjusted record, set in 1980, gold has made all-time highs not just in U.S. dollars but in euros, pounds, yuan and nearly every major currency.

The Flight to Precious Metals

What’s driving this? In short, fear and uncertainty. Central banks around the world have been consistent buyers, topping up their reserves with bullion in record amounts. Gold-backed ETFs have seen nearly $50 billion in inflows so far this year, their second-strongest run on record, according to the World Gold Council (WGC).

Ray Dalio, the legendary founder of Bridgewater Associates, put it plainly this month: A well-diversified portfolio should have 10–15% in gold, which exceeds my own recommendation of 10%. He likens U.S. debt to plaque clogging an artery, warning that a financial “heart attack” may be looming. Gold, he says, could be an antidote.

While gold has stolen the spotlight, silver is staging its own rally, up more than 40% this year and trading at 14-year highs. Some analysts predict it could reach $100 an ounce, driven by both investor demand and industrial applications in solar panels and electronics. For those who like leverage on leverage, silver mining equities could offer even more torque.

Mining Stocks Surge Past Highs

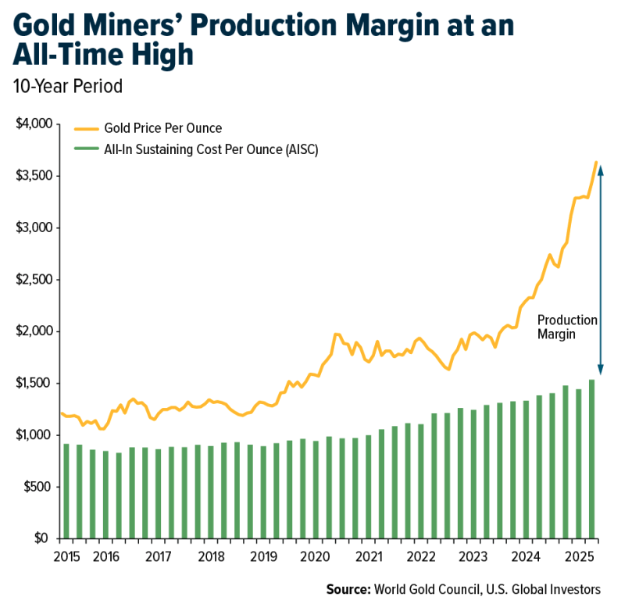

As I’ve pointed out many times before, when gold rises, miners tend to rise faster. That’s because their costs are relatively fixed: Once you’ve paid to dig, crush and process ore, the value of each extra ounce flows straight to the bottom line. At $1,800 gold, many mines were just scraping by. At $3,600 gold, they’re minting money.

Consider the numbers. Average all-in sustaining costs (AISC) for major producers hover between $1,080 and $1,220 per ounce. With spot prices more than triple that, the margins are extraordinary.

It’s no wonder, then, that mining indices have exploded. The NYSE Arca Gold Miners Index hit a new all-time high this month, surpassing levels last seen in 2011. Individual names like Sibanye-Stillwater, AngloGold Ashanti and Gold Fields have each gained more than 150% year-to-date, while SSR Mining has risen an extraordinary +220%.

Free Cash Flow Fuels Dividends and Buybacks

Veteran investors might remember past gold bull markets where companies, flush with cash, chased growth at any cost. They spent recklessly on acquisitions, overbuilt mines and diluted shareholders. Not this time.

In 2025, miners are showing discipline. Management teams are focused on operational efficiency, strong balance sheets and shareholder returns. They’re channeling cash into dividends and buybacks.

Free cash flow has surged across the industry, and return on invested capital is at multi-year highs.

This new culture of restraint makes the current rally very different from the last one. The fundamentals are healthier, and balance sheets are stronger.

Recession Warnings Are Growing Louder

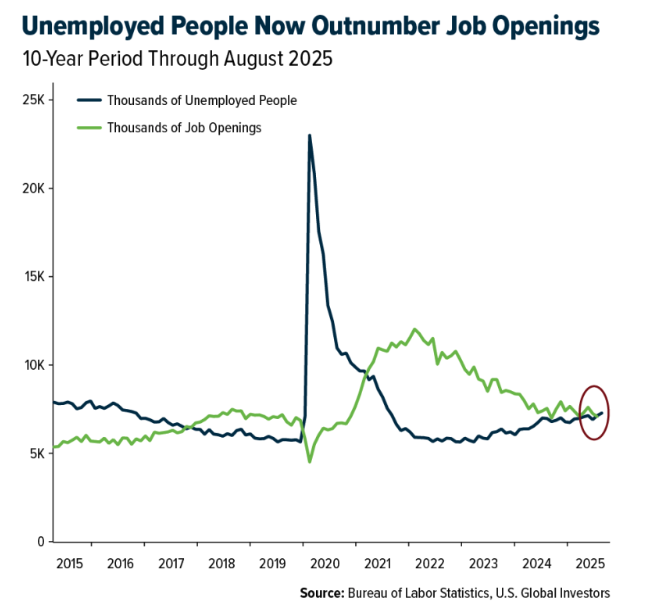

We can’t ignore the broader macroeconomic backdrop. The U.S. economy is showing unmistakable signs of strain. The Labor Department recently revised job growth lower by 911,000 positions through March, the largest adjustment in more than two decades. The country now has more unemployed workers than job openings for the first time since 2021. Consumer inflation remains sticky at 2.9%, even as wholesale prices briefly dipped.

Economists warn the economy could tip into recession by year-end. JPMorgan CEO Jamie Dimon says he thinks the economy is “weakening,” while Moody’s chief economist Mark Zandi, who forecast the 2008 financial crisis, expresses concern about stagflation, describing it as “pernicious.”

Layer onto this the political noise. President Trump’s moves to exert control over the Federal Reserve—such as efforts to oust Governor Lisa Cook—have many investors on edge. Goldman Sachs warns that if Fed independence is compromised and just 1% of the $27 trillion Treasury market flows into gold, the price could soar to $5,000 per ounce.

A Golden Opportunity

Gold is on fire. It’s making new records in nearly every currency, fueled by central banks, ETFs and private investors.

Miners are leveraged winners right now. With costs around $1,100 and gold above $3,600, margins are the fattest in decades. Again, I recommend a 10% weighting, with 5% in physical bullion (bars, coins, jewelry) and the other 5% in high-quality gold mining equities. Rebalance on a regular basis.

As the old saying goes, “Don’t wait to buy gold. Buy gold and wait.” And don’t overlook the miners.

They’re striking it rich and bringing shareholders along for the ride.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.95%. The S&P 500 Stock Index rose 1.59%, while the Nasdaq Composite climbed 2.03%. The Russell 2000 small capitalization index gained 0.25% this week.

- The Hang Seng Composite gained 4.07% this week while Taiwan was up 4.00% and the KOSPI 5.94%.

- The 10-year Treasury bond yield fell 1 basis point to 4.065%.

Airlines and Shipping

Strengths

- The best performing airline stock for the week was Sabre, 9.4%. According to RBC, Boeing reported 57 commercial deliveries in August, up 43% year-over-year. Across the company’s 57 deliveries, Boeing delivered 42 MAX aircraft, 1 737 NG, 1 767, 4 777s, and 9 787s.

- According to Bank of America, for Scorpio Tankers, rate increases are driven by counter-seasonal strength in product tanker rates, which more than offsets a decrease in net revenue days.

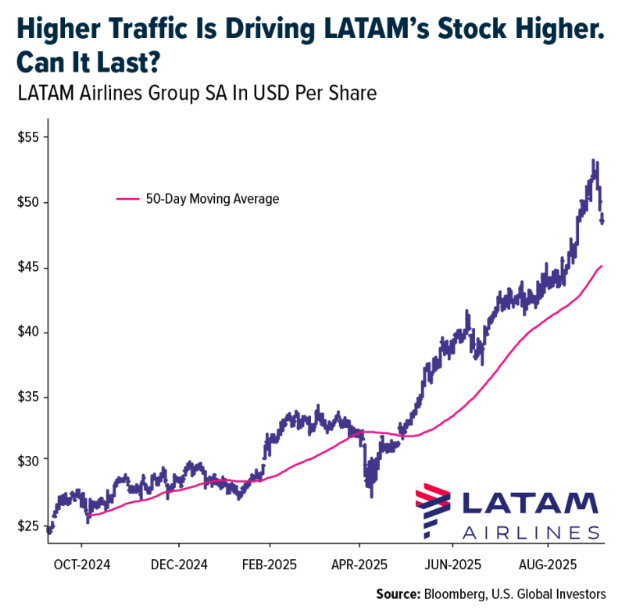

- LATAM’s total traffic (RPK) increased 10.8% year-over-year in August, reports Morgan Stanley. Quarter-to-date traffic is up 10.7%, which compares to the third quarter 2025 consensus of +9.7%. Domestic Brazil (up 15.9% year-over-year) outperformed International (up 11.2% year-over-year).

Weaknesses

- The worst performing airline stock for the week was SkyWest, down 9.7%. For Air Canada, the wage decision will go to an arbitration process. The union does not have the ability to strike again, so the airline’s operations will continue uninterrupted. Flight attendants voted 99.1 percent against, with a voter turnout of 94.6 percent.

- Laden vessels from China to the U.S. dropped sequentially by 14% and were down 32% on a year-over-year basis, reports Goldman. Data suggests mid-September is shaping up to be up and down based on Port of LA data, following late August and early September readings that were generally weak, continuing the uncertain trends post the initial China surge.

- According to Morgan Stanley, Grupo Aeroportuario del Sureste’s total passenger traffic increased 0.6% year-over-year in August. Quarter-to-date traffic is up 1.1% year-over-year, which compares to third quarter 2025 consensus of 2.9%. In August, international traffic was up 2.9% year-over-year, while domestic traffic was down 0.5% year-over-year.

Opportunities

- Goldman’s analysis of Spirit cutbacks screens positively for Alaska Air, which sees the largest drop among the airlines they track in the proportion of its network competing with Spirit. This is driven in part by a 65% decrease in Spirit capacity in Alaska’s markets in the fourth quarter of 2025.

- According to Morgan Stanley, regarding changes to de minimis rules, a sizeable majority of shippers (82%) reported not using the de minimis rule for importing goods. Among those who do use it, there was an even split between shippers who said they will pay higher duties and those who expect to take other actions in response to the rule’s removal.

- Competition for Spirit’s market share has already begun, reports Bank of America, with Frontier and United Airlines announcing new routes and additional flights into Spirit’s top airports (Fort Lauderdale, Orlando, Las Vegas), as well as airports Spirit recently exited.

Threats

- Bank of America believes Spirit will likely retrench at the airports from which they fly the most and have the highest market share. These include top airports by share of flights—Fort Lauderdale, Orlando, and Las Vegas—as well as airports where they have been growing service in recent years, such as Detroit, New Orleans, and Nashville. Among their top airports, Fort Lauderdale (26%), Orlando (11%), and New Orleans (10%) are the only airports where Spirit has more than a 10% market share.

- The National Retail Federation projects that container imports to North America from September 2025 through year-end will decline by 20% year-over-year. Pressure from new vessel supply also continues, according to Morgan Stanley.

- According to TD, the major airports in Florida—Orlando, Miami, Fort Lauderdale, and Tampa—saw steep year-over-year declines for much of the year, but Orlando is seeing sustained improvements. Miami and Tampa have been volatile, while Fort Lauderdale has consistently declined.

Luxury Goods and International Markets

Strength

- British luxury fashion house Burberry Group plc is set to re-enter the FTSE 100 index on September 22, 2025, after spending a year outside the benchmark blue-chip index. Burberry’s return is driven by a sharp rebound in its market value, with the stock rising over 70%. The recovery reflects CEO Joshua Schulman’s strategy to refocus on outerwear and reduce costs, helping the brand regain its place in the index.

- Ermenegildo Zegna, the Italian luxury fashion house, reported a 53% increase in profit for the first half of 2025, reaching €47.9 million. The strong performance highlights the brand’s ability to capture growing demand, manage costs effectively, and expand its market presence. The profit growth also reflects Zegna’s success in balancing its luxury heritage with modern consumer trends.

- Cettire, an Australian online marketplace for luxury goods, led the S&P Global Luxury Index with a 13.0% gain this week. The stock rallied early in the week without a clear news catalyst, although it remains down 72% year-to-date.

Weaknesses

- Initial jobless claims in the U.S. rose to 263,000 last week, up from 236,000 the month before and exceeding expectations of around 235,000. At the same time, inflation climbed to 2.9% in August from 2.7% in July, with core inflation remaining elevated at 3.1%. Rising jobless claims and persistent inflation add pressure on consumers.

- Investor confidence in the Eurozone dropped sharply in September, according to Sentix. The index fell to -9.2 from -3.7 in August, significantly worse than expected. Both the current situation assessment and future expectations declined notably.

- CityChamp Watch & Jewellery, a Hong Kong–listed jewelry and watch retailer, was the worst-performing stock in the S&P Global Luxury Index, falling 21.7%. This marks the second consecutive week as the index’s weakest performer, following revelations that one of its subsidiaries reported losses instead of profits.

Opportunities

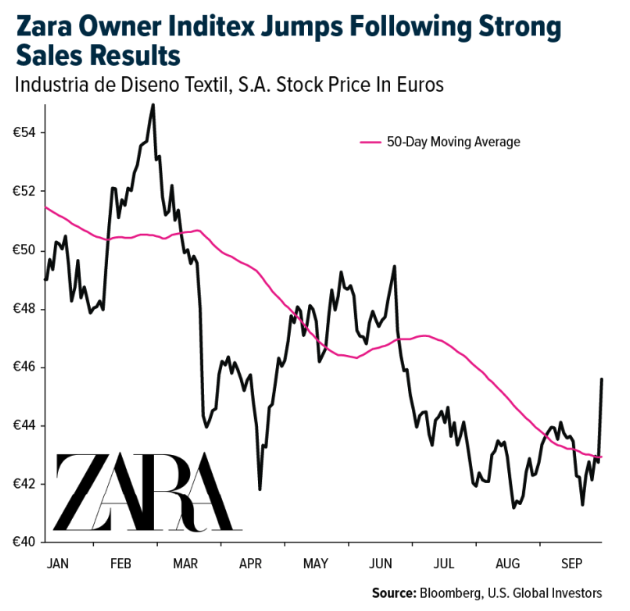

- ITX, the parent company of Zara, reported strong sales over the past five weeks, signaling resilient consumer demand and strong momentum in its fashion lines. Recent collections have been well-received, supporting revenue growth and boosting investor sentiment. With the share price breaking above its 50-day moving average, the stock shows potential for further upside.

- Volkswagen is investing €1 billion in artificial intelligence to improve efficiency and enhance its competitiveness. The company expects AI to streamline operations, optimize production, and drive innovation across its business. This investment could lead to significant cost savings, with potential benefits estimated at up to €4 billion by 2035.

- The U.S. job market is showing signs of weakening, with slower hiring and growing concerns about economic momentum. This trend increases the likelihood that the Federal Reserve will cut interest rates, as softer labor data strengthens the case for easing monetary policy. Investors now view rate cuts as more likely in the near term.

Threats

- Geopolitical tensions have escalated after Russian drones entered Polish airspace, prompting a swift military response. Fighter jets intercepted and shot down 19 drones, highlighting growing security risks along Europe’s eastern flank. The incident underscores rising regional instability and the potential for further escalation.

- Political tensions in France may increase volatility on the Paris Stock Exchange, where many major luxury companies are listed. The government recently survived a no-confidence vote, avoiding a leadership change but exposing deep divisions in parliament and raising concerns about policy stability. In response, President Emmanuel Macron appointed a new prime minister to reset his agenda, rebuild political support, and restore investor confidence—signaling efforts to stabilize both the government and the markets.

- India’s new consumer tax reform, which introduces higher taxes on global fashion brands such as PVH, Zara, and Levi Strauss, poses a challenge for some luxury and premium labels. The increased tax burden could raise prices, reduce affordability for middle-class consumers, and slow sales growth in one of the world’s fastest-growing retail markets, pressuring margins and limiting expansion opportunities.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was coffee, up 6.21% The strong market demand for Black Rock Coffee Bar’s IPO, which was priced above its marketed range and raised $294.1 million, reflects robust investor confidence in the coffee sector. This enthusiasm for coffee equities highlights the sector’s resilience and growth potential, as Black Rock’s expansion plans and positive same-store sales growth underscore the industry’s strength and ongoing consumer spending support.

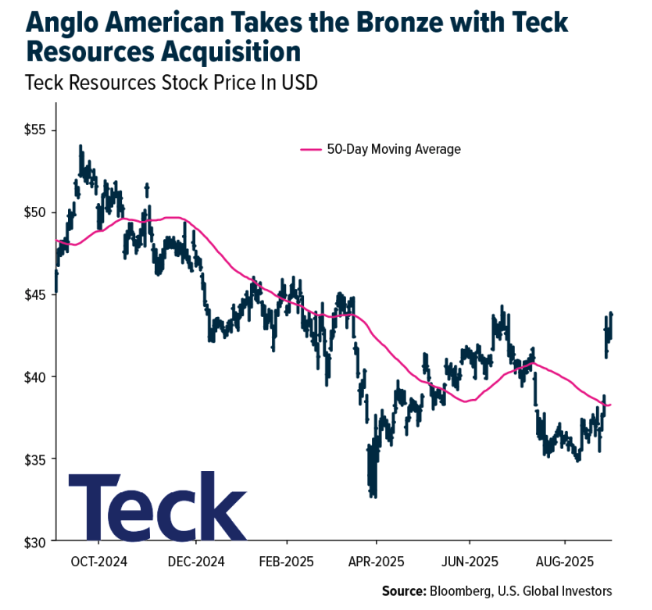

- Anglo American’s bold move to acquire Teck secures a world-class portfolio of copper assets at a time when demand for the metal is set to soar with the global energy transition. By integrating Teck’s flagship Quebrada Blanca project with its own Collahuasi mine, Anglo strengthens its position as a copper powerhouse with scale and synergies that rivals like BHP and Rio cannot easily replicate.

- A long-awaited partnership between the UK and U.S. could significantly benefit the market by reducing tariffs, lowering costs for producers and boosting trade flows. Additionally, this collaboration could strengthen transatlantic economic ties, support domestic steel industries, and promote investment in greener, more sustainable steel production technologies, Bloomberg reports.

Weaknesses

- The worst performing commodity for the week was lithium carbonate, down 4.57%. Lithium miners sank after CATL said it would restart operations at its Jianxiawo mine in China earlier than expected, adding supply pressure to an already weak market. Prices have collapsed from pandemic-era highs, weighed down by slower EV demand and a wave of new global production. Still, strategic deals such as Codelco’s partnership with SQM and Jindalee Lithium’s U.S. listing plans show long-term confidence in lithium’s role in the energy transition.

- The EU’s top court annulled a decision approving Hungary’s state aid for the Russian-led expansion of its nuclear plant, putting the decade-old project in uncertain territory. The ruling underscores ongoing tensions between Hungary and the EU, with the project now facing possible delays amid legal and political disputes.

- The U.S. solar industry faces major challenges from recent hostile White House policies, causing project delays and a projected 20% drop in the residential market. This political and regulatory environment has led to sector consolidation and weakened investor confidence, threatening the industry’s long-term growth and goal of becoming the world’s fastest, cheapest power source.

Opportunities

- Oil-field service companies are shifting focus to off-grid power solutions for tech firms, especially data centers driving AI growth, amid declining oil-field activity. These modular units enable quick deployment and avoid long grid connection delays but face risks like cost fluctuations and ongoing fossil fuel dependence, Bloomberg reports.

- The goal to triple nuclear energy capacity by 2050 creates major opportunities for uranium and nuclear fuel miners. Increased demand will require expanding and securing fuel supplies, likely driving higher nuclear fuel prices—benefiting miners who can meet this growing need, as highlighted at the World Nuclear Association conference.

- A multiyear LNG supply glut starting in 2026 offers LNG exporters and infrastructure developers a chance to capture market share as prices are expected to drop below $10 per million Btu. This will make natural gas more competitive globally and could boost LNG adoption in emerging Asian and African markets if import infrastructure develops, Factset reports.

Threats

- An Indonesian task force has seized land from nickel miners PT Weda Bay Nickel and PT Tonia Mitra Sejahtera for missing forestry permits. This move aims to curb illegal resource exploitation, with the government identifying 4.2 million hectares lacking proper permits across 51 companies, Reuters reports.

- The election outcome in Buenos Aires, Argentina, affects its attractive tax regime by reducing confidence in Milei’s reform agenda, which seeks to minimize government involvement and boost private investment. A significant defeat could slow or weaken efforts to overhaul the tax system and attract investment.

- The unexpected restart of CATL’s lithium mine caused lithium and related stock prices to fall sharply, showing how news can impact prices and investor sentiment. Such events often increase volatility as companies scale up amid price fluctuations, affecting overall lithium market dynamics, Bloomberg reports.

Bitcoin and Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was MYX, rising 1,280%.

- BlackRock is exploring how to make ETFs available as tokens on the blockchain. The firm is working on tokenizing funds tied to real-world assets such as stocks, subject to regulatory considerations. Tokenization could enable trading beyond Wall Street’s set hours, improve access to U.S. products abroad, and create potential use as collateral in crypto networks, Bloomberg reports.

- Crypto exchange Kraken has opened trading of tokenized U.S. securities to its customers in the European Union, expanding access to this emerging asset class. The offering includes more than 60 tokenized equities—blockchain-based certificates designed to track the price of companies like Apple, Meta, and GameStop—for trading in the region, Bloomberg reports.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Form, down 27.31%.

- Zodia Custody has dissolved its Japanese joint venture with SBI Holdings Inc., two years after its launch, following a strategic reassessment. SBI Zodia Custody had been in discussions with Japan’s Financial Services Agency about applying for local registration but had not proceeded before deciding to terminate the business, according to Bloomberg.

- Coinbase has filed a complaint against Dynapass Inc., seeking a declaratory judgment that it does not infringe a user authentication patent and that the patent is invalid. Coinbase claims Dynapass baselessly accused it of infringing a U.S. patent by requiring two-factor authentication for its users, Bloomberg reports.

Opportunities

- The stablecoin boom has triggered a talent war, making it both difficult and costly for companies like Dfns to fill open roles. Salaries in the space have surged, with head of stablecoin strategy positions in the U.S. typically offering base salaries between $250,000 and $400,000, according to Bloomberg.

- Eightco Holdings Inc. soared over 3,000% after announcing plans to purchase digital tokens backed by OpenAI’s Sam Altman and appointing Wall Street analyst Dan Ives as chairman. The company agreed to sell approximately 171.2 million shares at $1.46 each in a private placement to fund Worldcoin acquisitions and may also adopt Ether as a secondary reserve currency, Bloomberg reports.

- Gemini Space Station increased the potential size of its IPO offering to $433.3 million. The company raised its price range to $24–$26 per share, up from $17–$19, while still offering 16.7 million shares. At the top of the new range, Gemini would have a market value of $3.1 billion based on the outstanding shares listed in its filing, Bloomberg reports.

Threats

- Shares of digital-asset treasury companies are falling, and market confidence is slipping. Among the 15 DATs tracked by Architect Partners, the average decline last week was 15%. Many of these firms launched this year, with over 100 companies buying cryptocurrencies for their treasuries. Some are now struggling due to limited differentiation and high risk, according to Bloomberg.

- Digital assets and related equities extended losses on Thursday, with some of the steepest declines hitting tokens and companies linked to ventures associated with President Trump’s family. The drop in treasury company shares is also dragging down the prices of the underlying tokens, Bloomberg reports.

- Coinbase has accused the SEC of damaging public trust by deleting texts from Chair Gary Gensler. In a court filing on Tuesday, Coinbase alleged that the SEC failed to comply with prior orders to disclose communications related to Ethereum and other digital assets, according to Coinpedia.

Defense and Cybersecurity

Strengths

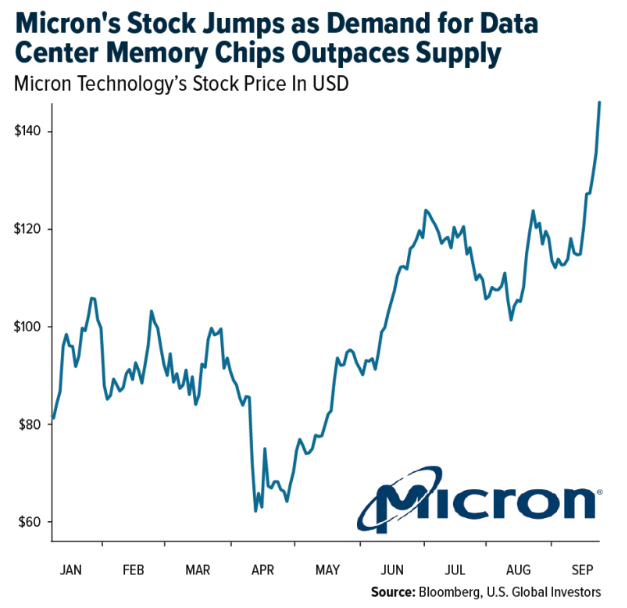

- Micron’s stock jumped as demand for its memory chips in AI-driven data centers is outpacing supply. Investors are betting on stronger guidance ahead of the company’s upcoming earnings as inference workloads fuel even greater need for DRAM and NAND.

- Seagate Technology has overtaken Palantir Technologies as the top-performing stock in the S&P 500, fueled by surging demand for AI data centers and storage solutions—even as Palantir continues to post strong gains.

- The best performing stock in the XAR ETF this week was Rocket Lab Corp., rising 16.41%, after the company successfully completed its 70th Electron mission. This highlights progress on its new Virginia launch complex for the Neutron rocket and drew fresh analyst optimism.

Weaknesses

- Russia launched its largest aerial barrage of the war this week, setting a government building in Kyiv ablaze for the first time. Simultaneously, about 19 Russian drones crossed into Polish airspace, marking a serious breach of NATO territory.

- Israel’s first-ever strike in Qatar killed six Hamas leaders and derailed hopes for Gaza hostage talks. Netanyahu declared Gaza belongs to Israel and ruled out a future Palestinian state, as tensions rise with continued strikes on Yemen and talk of a West Bank offensive—fueling a dangerous regional escalation.

- This week’s worst-performing stock was Boeing Corp, down 5.95%, after the company was hit with a $3.1 million FAA fine for safety violations, warned of new 777X certification delays, faced an extended defense worker strike, and remained under a production cap on its 737 MAX jets.

Opportunities

- CBRE reports that data center vacancy in top North American markets fell to a record low of 1.6% in the first half of 2025, as hyperscaler demand, power constraints, and AI-driven growth push rents higher—particularly for large-scale deployments.

- Intel’s new Core Ultra 3 205 outperformed the i3-14100 in benchmarks, running up to 75% faster in Cinebench R23 and already selling at a competitive price in some regions. Additionally, Intel’s Arc Pro B60 GPUs beat NVIDIA by up to 4x in performance-per-dollar on MLPerf AI tests in Linux, showcasing the platform’s efficiency for AI workloads.

- AeroVironment’s acquisition of BlueHalo significantly boosted revenue, with a 140% year-over-year increase, but also resulted in a net loss of $67.4 million due to related costs. Despite integration challenges, the company expects to generate up to $2 billion in fiscal 2026.

Threats

- Ukraine reports that Russia now has nearly 700,000 troops on its territory, primarily in Donetsk, with reinforcements and North Korean support maintaining pressure on Ukrainian defenses despite over a million Russian casualties.

- China recently unveiled its new LY-1 naval laser during a major military parade—a high-power system mounted on an HZ141 vehicle that suggests future shipboard deployment. Cooling technology breakthroughs may allow continuous fire capable of disabling drones, missiles, and enemy sensors at very low cost.

- The U.S. and allied militaries are facing dangerously low missile and rocket stockpiles, with production shortfalls and fragile supply chains failing to meet wartime demand. Without urgent modernization and expanded capacity for propellants and rocket motors, any prolonged near-peer conflict could rapidly deplete munitions and erode sustained firepower.

Gold Market

This week gold futures closed at $3,683.60, up $30.30 per ounce, or 0.83%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5.08%. The S&P/TSX Venture Index came in up 2.57%. The U.S. Trade-Weighted Dollar fell 0.17%.

Strengths

- The best performing precious metal for the week was palladium, up 10.55%. ETFs have now added palladium for eight consecutive days, with 1,777 troy ounces purchased, signaling ongoing institutional demand. Strategic moves like Sprott Asset Management’s $100 million issuance highlight strong fundamentals, driven by palladium’s key role in catalytic converters and resilient industrial demand.

- Precious metals refiner Heraeus notes that the Saudi Central Bank has moved into silver by acquiring $40.6 million worth of shares in the iShares Silver Trust and Global X Silver Miners ETF. These investments likely reflect a broader strategy by the country’s sovereign wealth fund. While the ETFs are backed by physical metal, this does not represent a direct bullion purchase.

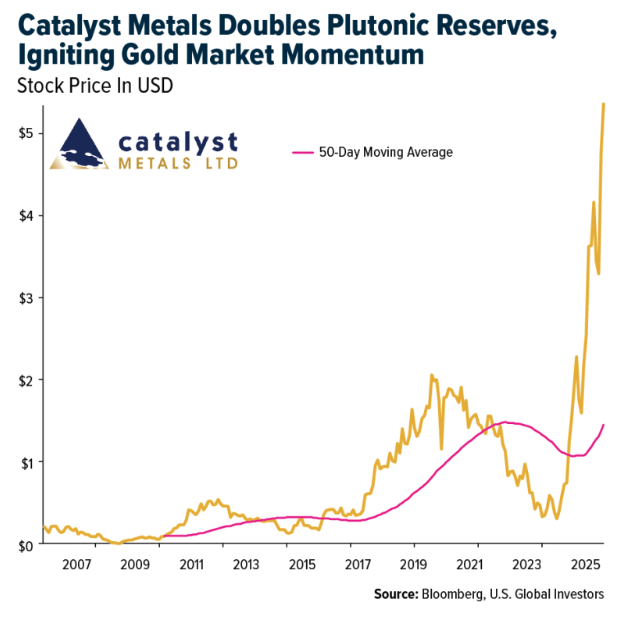

- Catalyst Metals has supercharged the gold market, announcing a 100% increase in reserves at its Plutonic Gold Belt to 1.5 million ounces. With a new 10-year mine plan and a 200,000-ounce annual production target, the company is helping drive the rally. Shares hit an all-time high, showing how reserve growth can boost both investor confidence and market momentum.

Weaknesses

- Gold was the worst performing precious metal of the week, though still up 0.83%. China’s move to ease gold import/export rules aims to diversify reserves away from the U.S. dollar and boost trade. While this increases market liquidity, it may reduce gold’s role as a traditional haven asset during geopolitical uncertainty.

- Following Pan African’s trading statement and operational update, the company reported its fiscal 2025 results with in-line production, slightly higher costs, and lower-than-expected earnings, according to BMO.

- According to Scotia, Pan American Silver updated its Reserves and Resources to include 452 million ounces of silver and 6.3 million ounces of gold—a 3% and 8% decrease, respectively—due to mining depletion and the divestment of La Arena. Silver and gold resources were down 2% and 36%, largely driven by the sale of the La Arena mine and the Joaquin property.

Opportunities

- Bank of America examines the meteoric rise in the global gold sector’s total market capitalization, now around 2x previous cycle peaks. However, as a percentage of total world equity market capitalization, the gold sector remains well below prior highs. In terms of valuation, the sector also trades below historical peak levels.

- Barrick Gold announced the sale of the Hemlo gold mine for up to $1.09 billion, including an upfront cash payment of $875 million. They see the deal as accretive to Barrick’s NAV and another significant non-core asset sale this year.

- BMO views Wheaton’s acquisition of a $400 million gold stream on Hemlo as having a strong internal rate of return (IRR) of over 6% at spot prices. They favor deal features such as delivery rate upside if production misses plan and reduced stream rates on Franco-Nevada’s 50% NPI royalty land to maintain an economic mine plan at Hemlo. The stream could be reduced by 25% if gross proceeds from the upcoming private placement exceed $300 million.

Threats

- According to the Swiss Association of Precious Metals Producers and Traders (ASFCMP), “Historically, gold trade volumes between Switzerland and the USA were well balanced and are likely to continue on that basis in the long term.” The association will now analyze the details of the executive order to determine the best way forward for its members and partners. Nevertheless, the ASFCMP welcomes the opportunity to resume the longstanding and trusted gold trading relationship between Switzerland and the United States on a secure and stable basis.

- Centerra has less leverage to higher prices compared to peers due to declining Oksut production, stream-impacted Mount Milligan output (30% discount to spot), and below-average gold exposure (65% in 2028E versus peers above 90%), according to RBC.

- Centerra Gold reported the results of a prefeasibility study on its Mount Milligan copper-gold mine in British Columbia, Canada. The average all-in sustaining costs and total capex are 75% and 39% higher, respectively, than Bank of America’s expectations.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2025):

Zara

Volkswagen

Boeing

LATAM Airlines Group SA

Scorpio Tankers

Air Canada

Grupo Aeroportuario del Sureste

Alaska Air Group

United Airlines

Frontier Group Holdings

Catalyst Metals

Pan African Resources

Barrick Mining Corp.

Wheaton Precious Metals

Franco-Nevada Corp.

Centerra Gold Inc.

Sibanye Stillwater Ltd.

Anglogold Ashanti Plc

Gold Fields Ltd.

Seagate Technology

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

A message from Advisor Perspectives and VettaFi: Did you know that we provide daily updates when key market and economic indicators change? Visit the AP Charts and Analysis site to get our expert insights.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All