Personalized separately managed accounts (SMAs) have evolved into an effective customized solution that seeks to meet a client’s unique financial objectives. Historically in the fixed income space, those customizations have focused on interest rate risk tolerance, geographical preference and credit quality minimums. Now customization can be leveraged to target after-tax yield based on an investor’s federal tax rate, state tax rate and state of residence. At Parametric, we believe the focus shouldn’t just be on what an investor earns, but also on what they keep.

Taxes can take a bite of an investor’s return. Every basis point counts. Our strategy seeking to enhance after-tax yield and performance involves capitalizing on opportunities across multiple fixed income sectors. With this approach, investors can let their individual tax considerations and relative value in the market help them select a better after-tax option.

A traditional municipal bond buyer is often an investor in an upper tax bracket, who steers toward tax-exempt municipal bonds as a common fixed income allocation. Why? Because tax-exempt munis are more likely to provide the highest level of after-tax return most of the time. But this may not be true all the time. Parametric’s tax-optimized ladders (TOL) solution may help to enhance and balance a fixed income portfolio.

How do tax-optimized ladders work?

A TOL solution aims to improve the allocation between tax-exempt and taxable bonds based on an investor’s federal and state tax rates. This method allows an investor to buy the bond with the highest after-tax yield.

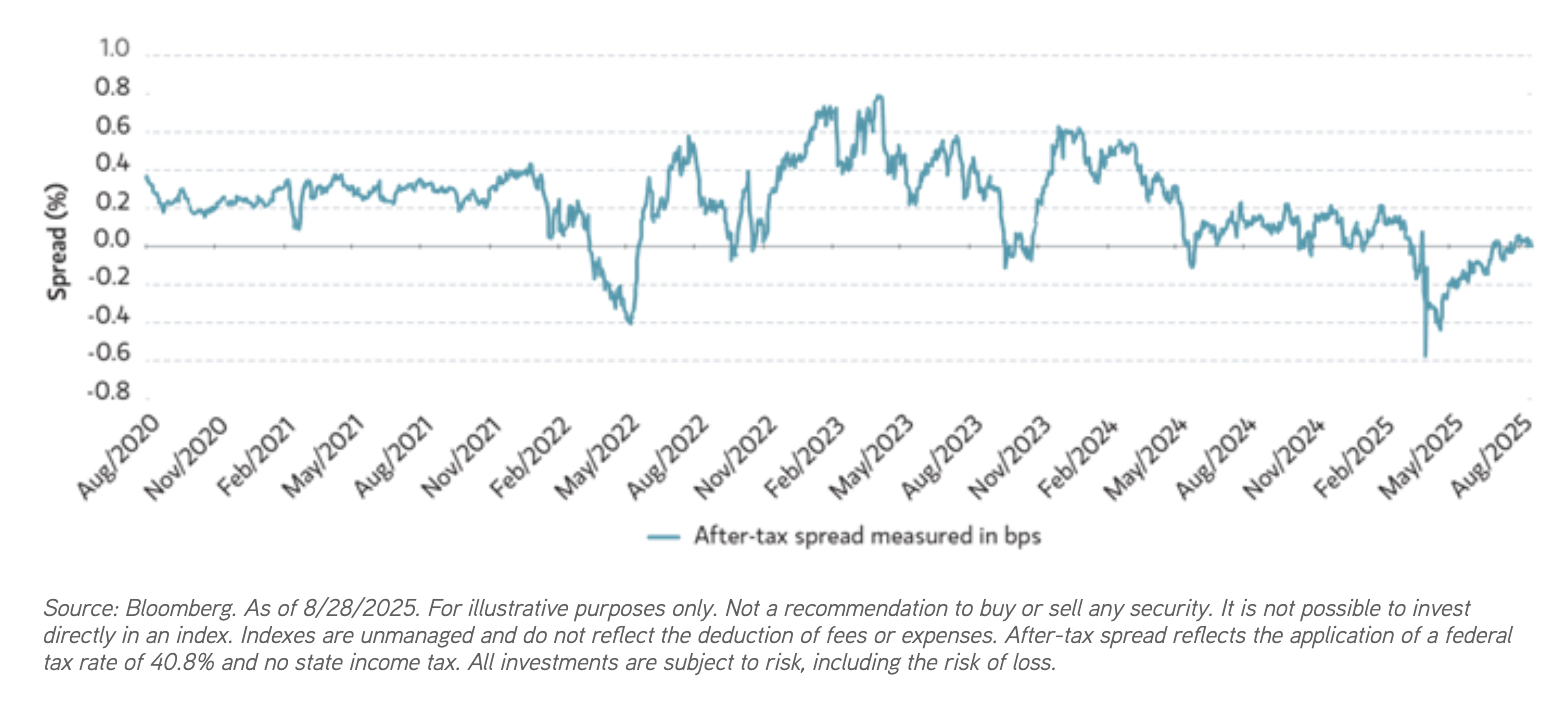

For example, consider this comparison of two prominent fixed income indexes. As of August 28, 2025, the Bloomberg Managed Money Short/Intermediate Municipal Bond Index would have a yield to worst of 2.68%, while the Bloomberg Intermediate Corporate Bond Index would have a yield to worst of 4.51%, or 2.67% after tax if we applied a federal tax rate of 40.8% and no state income tax. Based on these assumptions, there could be greater potential in municipals today because the yield to worst is one bps higher than the after-tax corporate index yield to worst.

After-Tax Intermediate Municipal and Corporate Bond Yields Over Five Years

When this spread is positive, or above zero, it would indicate that there is potential opportunity in the corporate bond asset class on an after-tax income basis. When the spread is negative, it would indicate that the municipal bond index yield to worst is greater than the after-tax yield from the corporate index.

This in a nutshell is the investment approach for Parametric’s tax-optimized ladder strategy. We consider an investor’s individual tax situation, and we compare the available investments across asset classes prior to purchasing securities. Instead of evaluating market index data, our team compares the individual securities available for purchase and allocates accordingly.

To help investors gauge what they may see in their portfolios based on today’s market conditions, we’ve added an additional TOL tab to our Fixed Income Ladder Tool. This tool allows investors to input their tax situation, state of residence and ladder customization options and see what type of investment allocation they may experience in a portfolio today. Investors can also see what their asset allocations could have looked like historically. Just because municipal bonds may offer the most after-tax income today, it rarely means they have been the highest yielding asset class throughout history.

Investment advisory services offered through Parametric Portfolio Associates LLC ("Parametric"), an investment advisor registered with the US Securities and Exchange Commission (CRD #114310). Parametric is also registered as a portfolio manager with the securities regulatory authorities in certain provinces of Canada (National Registration Database No. 42850) with regard to specific products and strategies. Parametric provides advisory services directly to institutional investors and indirectly to individual investors through financial intermediaries. The information on this website does not constitute an offer to sell, or a solicitation of an offer to purchase, securities in any jurisdiction to any person to whom it is not lawful to make such an offer. Investing entails risks, and there can be no assurance that Parametric (and its affiliates) will achieve profits or avoid incurring losses. All investments are subject to potential loss of principal. Parametric does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the disclosure page for important information about investments and risks.

S&P Dow Jones Indices are a product of S&P Dow Jones Indices LLC (“S&P DJI”) and have been licensed for use. S&P® indexes are registered trademarks of S&P DJI; Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); S&P DJI, Dow Jones, and their respective affiliates do not sponsor, endorse, sell, or promote Parametric and its strategies, will not have any liability with respect thereto, and do not have any liability for any errors, omissions, or interruptions of the S&P Dow Jones Indices.