Key Takeaways

- Pension surplus can be used strategically to benefit both participants and sponsors

- Uses include funding benefit enhancements, early retirement incentives, or future plan accruals

- Sponsors should balance participant security, fiduciary duties and organizational goals when using pension surplus

Trapped capital? Think again.

In recent years, pension funded status has markedly improved, with average funded ratios surpassing 100%.1 Many sponsors who once faced significant contribution requirements and PBGC premiums now manage well-funded plans with fewer complications. Historically, the primary goal for many sponsors was to achieve sufficient funding to enable either plan hibernation or plan termination. Today, however, an increasing number of sponsors are recognizing the range of potential opportunities surplus assets can provide.

Yet the traditional view often undervalues pension surplus beyond termination needs. It’s time to rethink that. Simply put, the industry expression of pension surplus as “trapped capital” is an exaggeration. Why? Because there are many ways to put plan surplus to work strategically (some are easier to implement than others). First and foremost, though, each option should be thoughtfully evaluated with the organization’s goals and fiduciary responsibilities in mind.

Hidden Value

First, when deciding how to value a pension plan’s surplus, sponsors should closely examine the range of available options and their alignment with organizational objectives. The potential value of surplus assets should not be underestimated, as using them wisely can lead to significant benefits.

The value attributed to surplus pension assets also affects how a sponsor chooses to invest. For example, a sponsor with a 120% funded plan with 90% of assets invested in liability-hedging fixed income may choose to reduce that allocation to 80% to build in more potential for asset growth, while keeping the liability hedge. This makes sense if value is placed on surplus and the chances of becoming underfunded again are low.

Once participant benefits are secured and fiduciary requirements met, sponsors can explore numerous ways to use surplus assets. These range from strategies that primarily benefit participants to those that favor plan sponsors, as well as approaches that deliver shared advantages to both.

Plan sponsors should be mindful of the role they are filling when making decisions regarding pension surplus. Fiduciaries act in the interest of participants in the plan, while settlors act in the interest of the business.

Benefit Boost

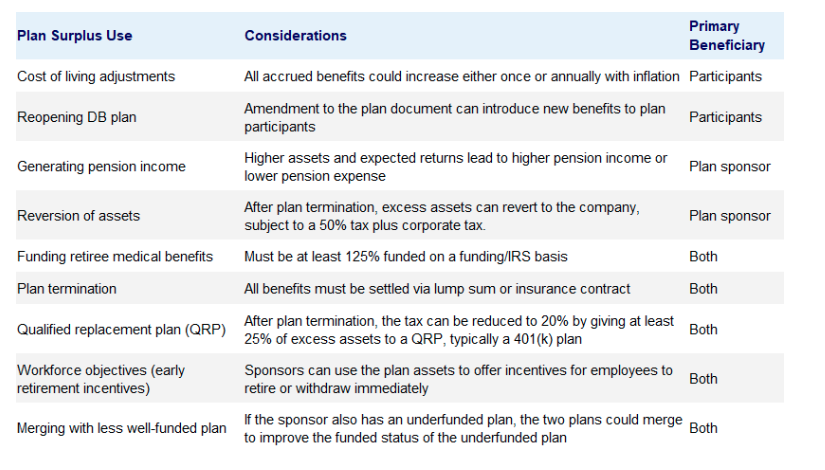

One of the simplest ways to use surplus for participants is by enhancing the plan to increase accrued benefits. Examples include granting ad hoc benefit increases above original plan commitments or—as seen in recent precedent (IBM in 2023)—reopening previously closed or frozen plans to new accruals.

Sponsors might also consider introducing one-time cost-of-living adjustments—a feature largely absent from U.S. corporate pension structures—or providing supplemental “13th check” payments to retirees. Each of these measures uses surplus assets to elevate participant outcomes while maintaining the plan’s full funded status.

Unlocking Sponsor Gains

Meanwhile, pension surplus can also directly help the sponsoring organization. From an accounting perspective, more surplus and a higher expected rate of return may result in increased pension earnings, which may be important to sponsors.

Following plan termination, a part of the excess assets may be returned to the sponsor. However, this reversion is subject to a substantial tax rate of 50%, plus applicable corporate taxes. If at least 25% of the surplus is used to benefit 401(k) participants, the tax rate on the reverted amount may be reduced to 20%. For sponsors of non-frozen plans, pension surplus can be used to fund future ongoing benefit accruals.

Mutual Benefits

In addition, some uses of pension surplus could potentially benefit both the participants in the plan and the sponsoring organization. If the company sponsors a separate underfunded plan, they could merge it with the fully funded plan. This could potentially increase the benefit security for participants in one plan while maintaining it in the other. Participants could receive early retirement incentives, helping the sponsor with workforce objectives while supporting participants ready for retirement.

Here are some key uses of pension surplus, along with considerations.

Unlocking Pension Surplus

Sponsors can use pension surplus to benefit participants, the company or both

Applications, key considerations and beneficiaries of pension surplus

Breaking the Mold

For many years, plan sponsors with underfunded pension plans focused on achieving full funding. Most closed or frozen plans followed a glidepath approach—reducing exposure to return-seeking assets in favor of liability-hedging assets—to help secure gains in funded status.

Now, as many sponsors find themselves with fully funded plans but without immediate plans to terminate, it is time to reconsider the potential value of surplus assets. There is no need to compromise benefit security, and several practical options exist that may deliver tangible value. It is worth re-examining whether plan surplus truly is “trapped capital.”

1 Source: Milliman’s Pension Funding Index

A message from Advisor Perspectives and VettaFi: Ready to level up your skills? Explore our library of on-demand webcasts.

Important information pertaining to the hypothetical example: Past performance does not predict future returns. Return level is proportionately scaled in line with cash level to be overlaid. Source: Russell Investments. Assumptions: Average cash level 1.0%, 10-year history from 12/31/2023, gross of fees. Opportunity cost from not securitizing cash varies by asset allocation and time period, and is represented by horizontal bars as marked within the chart legend. Target asset allocation used: 0% cash, 74% MSCI World, 26% Global Aggregate (GBP Hedged). For illustrative purposes only. Does not represent any actual investment. Indexes are unmanaged and cannot be invested in directly. Performance benefit (net) of overlaying cash by last 5 individual calendar year is as follows: 2023:20 bps, 2022:-17bps, 2021:16bps, 2020:14bps, 2019:23bps.

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Diversification and strategic asset allocation do not assure a profit or guarantee against loss in declining markets.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The Russell Investments logo is a trademark and service mark of Russell Investments

The information, analyses and opinions set forth herein are intended to serve as general information only and should not be relied upon by any individual or entity as advice or recommendations specific to that individual entity. Anyone using this material should consult with their own attorney, accountant, financial or tax adviser or consultants on whom they rely for investment advice specific to their own circumstances.

Products and services described on this website are intended for United States residents only. Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained on this website should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional. Persons outside the United States may find more information about products and services available within their jurisdictions by going to Russell Investments' Worldwide site.

Russell Investments is committed to ensuring digital accessibility for people with disabilities. We are continually improving the user experience for everyone, and applying the relevant accessibility standards.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates Management, L.P., with a significant minority stake held by funds managed by Reverence Capital Partners, L.P. Certain of Russell Investments' employees and Hamilton Lane Advisors, LLC also hold minority, non-controlling, ownership stakes.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

© Russell Investments Group, LLC. 1995-2025. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

© Russell Investments

Read more commentaries by Russell Investments