From the lack of conviction in the previous meetings to last week’s “risk management cut,” Federal Reserve (Fed) officials continue to walk a very fine line, hoping for the effects of tariffs to be transitory while, at the same time, trusting that the recent weakness in the labor market is more of a combination of lower supply of labor (due to a declining labor force and deportations) as well as weakening demand for workers. Both of which are keeping the rate of unemployment near full employment, but in an environment of an economy that is showing signs of weakening.

Up until last week, a still historically low rate of unemployment meant that the labor market was strong and thus did not allow it to lower interest rates without risking even higher, and more lasting, inflation. However, it seems that the latest downward revisions to employment (and increased political pressure?) have convinced Fed FOMC members that they should lower interest rates just in case, or, as they called it, as a ‘risk management cut.’

The Fed Chairman argued that the revisions to the employment numbers had to do with the model the Bureau of Labor Statistics (BLS) uses to measure the ‘birth-death’ rate of new/old businesses in the US economy. He argued that the COVID-19 pandemic had messed up the accuracy of the model and that the BLS knew it and was working on improving its accuracy.

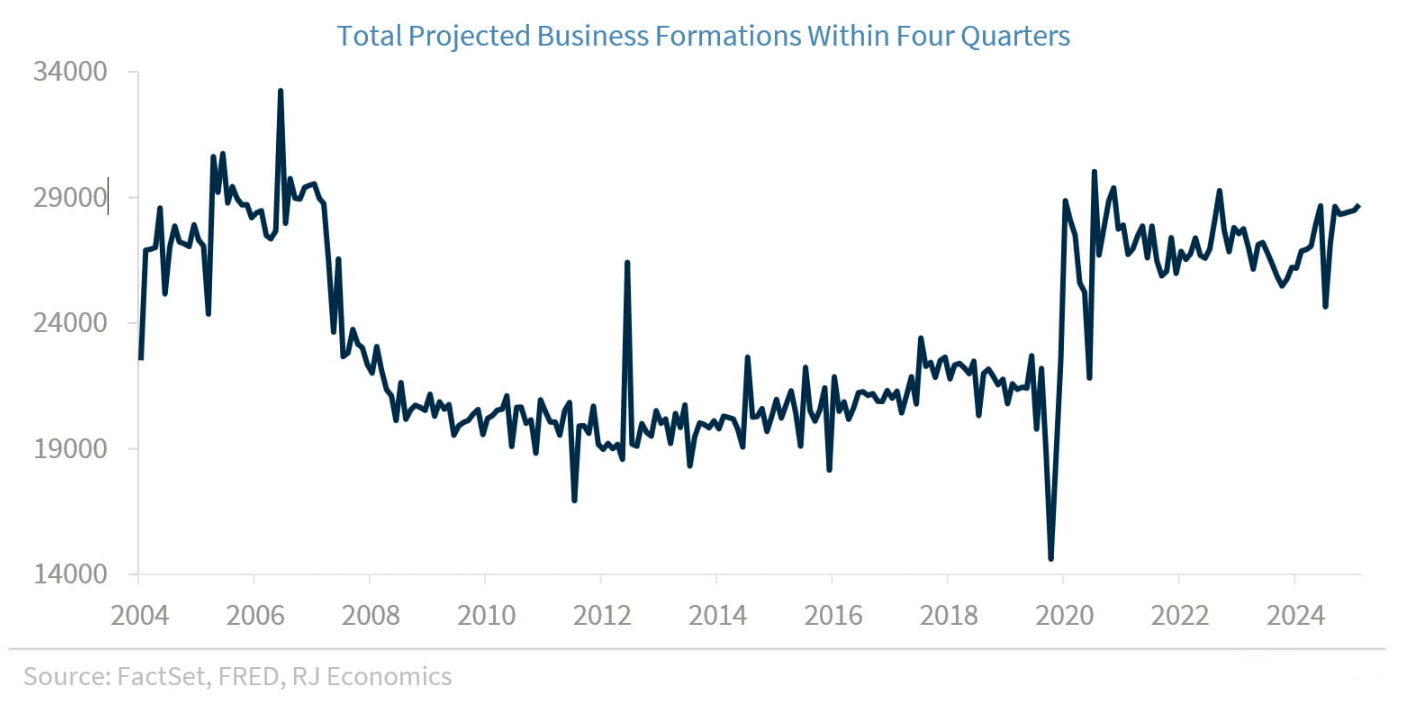

Part of the issue has to do with business formations, which is the estimate the BLS uses to account for job creation by new businesses. As the graph below shows, there was a clear structural shift in business formations after the Great Recession and another structural shift in business formations after the COVID- 19 pandemic, to which BLS statisticians are still trying to adapt their models to capture these changes.

But what the Fed Chairman did not say during the press conference and what the September FOMC Summary of Economic Projections (SEP) seems to be showing is that the NAIRU1 (the Non-Accelerating Inflation Rate of Unemployment) seems to have changed. That is, it seems that the current 4.3% rate of unemployment is higher than the NAIRU, meaning that there is slack in the labor market. This is also probably in line with Powell’s argument since early this year that wage pressures are no longer an inflation concern. If that is the case, then this is what has finally changed Fed members’ views of how much they could cut the federal funds rate without adding more fuel to the inflation fire brought by tariffs.

It is, of course, a ‘risk management cut’ because the Fed is not completely sure that the rate of unemployment is above the NAIRU and that there is slack in the labor market but is willing to cut rates if this turns out to be the case.

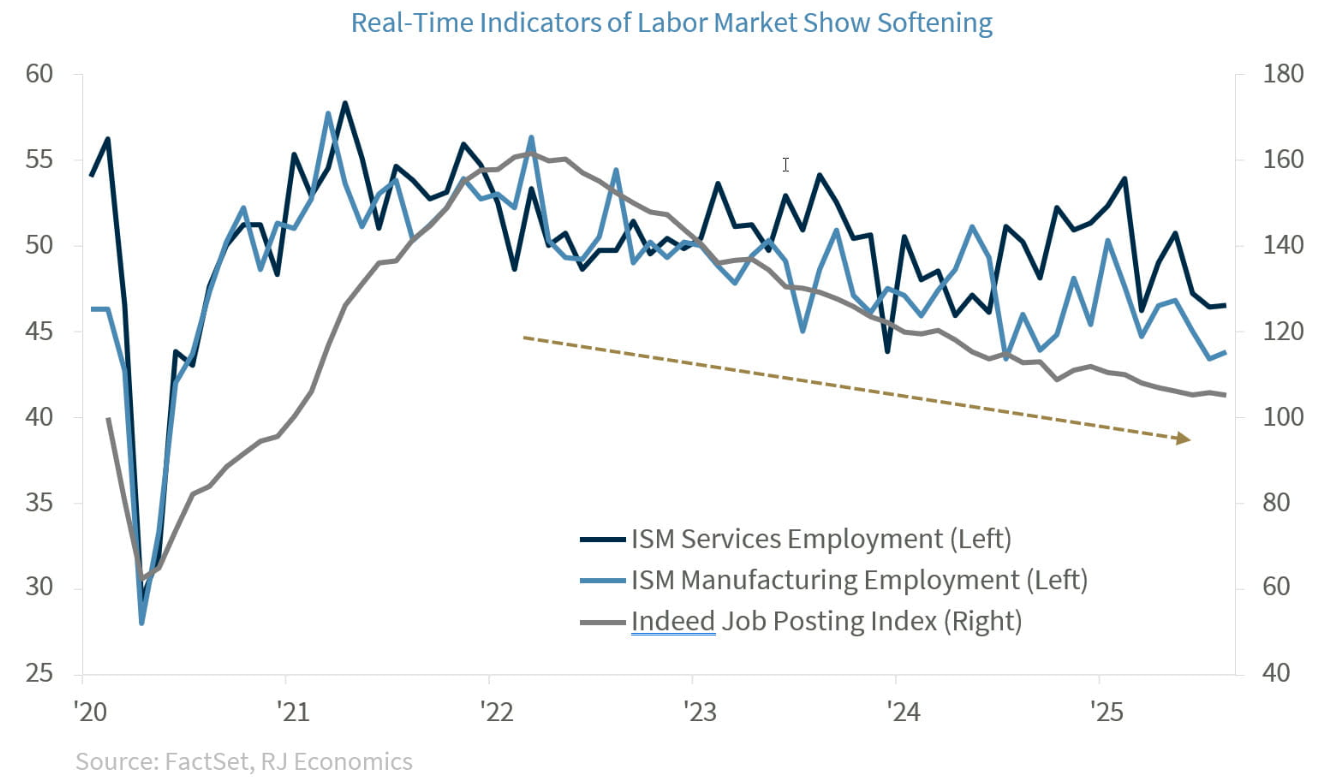

From the graph above, it has been clear for a while that the labor market has been weakening, and Fed members are finally, although grudgingly, getting on the economic/employment weakening bandwagon.

Perhaps the best news from the FOMC meeting and the SEP is that, although increased political pressure may have influenced the Fed’s decision, the group remains united with Stephen Miran as the only dissenter. That unity starts to dissipate when we look at the longer-term dot plot but that is understandable given the uncertainty surrounding future of economic activity and inflation.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.

Consumer Price Index is a measure of inflation compiled by the US Bureau of Labor Statistics. Currencies investing is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

Consumer Sentiment is a consumer confidence index published monthly by the University of Michigan. The index is normalized to have a value of 100 in the first quarter of 1966. Each month at least 500 telephone interviews are conducted of a contiguous United States sample.

Personal Consumption Expenditures Price Index (PCE): The PCE is a measure of the prices that people living in the United States, or those buying on their behalf, pay for goods and services. The change in the PCE price index is known for capturing inflation (or deflation) across a wide range of consumer expenses and reflecting changes in consumer behavior.

The Consumer Confidence Index (CCI) is a survey, administered by The Conference Board, that measures how optimistic or pessimistic consumers are regarding their expected financial situation. A value above 100 signals a boost in the consumers’ confidence towards the future economic situation, as a consequence of which they are less prone to save, and more inclined to consume. The opposite applies to values under 100.

Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® (with plaque design) in the United States to Certified Financial Planner Board of Standards, Inc., which authorizes individuals who successfully complete the organization’s initial and ongoing certification requirements to use the certification marks.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

GDP Price Index: A measure of inflation in the prices of goods and services produced in the United States. The gross domestic product price index includes the prices of U.S. goods and services exported to other countries. The prices that Americans pay for imports aren't part of this index.

Employment cost Index: The Employment Cost Index (ECI) measures the change in the hourly labor cost to employers over time. The ECI uses a fixed “basket” of labor to produce a pure cost change, free from the effects of workers moving between occupations and industries and includes both the cost of wages and salaries and the cost of benefits.

US Dollar Index: The US Dollar Index is an index of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners' currencies. The Index goes up when the U.S. dollar gains "strength" when compared to other currencies.

The FHFA HPI is a broad measure of the movement of single-family house prices. The FHFA HPI is a weighted, repeat- sales index, meaning that it measures average price changes in repeat sales or refinancings on the same properties.

Import Price Index: The import price index measure price changes in goods or services purchased from abroad by U.S. residents (imports) and sold to foreign buyers (exports). The indexes are updated once a month by the Bureau of Labor Statistics (BLS) International Price Program (IPP).

ISM Services PMI Index: The Institute of Supply Management (ISM) Non-Manufacturing Purchasing Managers' Index (PMI) (also known as the ISM Services PMI) report on Business, a composite index is calculated as an indicator of the overall economic condition for the non-manufacturing sector.

The ISM Manufacturing Index: The GDP Now Institute of Supply Management (ISM) Manufacturing Measures the health of the manufacturing sector by surveying purchasing managers at manufacturing firms. The survey asks about current business conditions and expectations for the future, including new orders, inventories, employment, and deliveries.

Consumer Price Index (CPI) A consumer price index is a price index, the price of a weighted average market basket of consumer goods and services purchased by households.

Producer Price Index: A producer price index (PPI) is a price index that measures the average changes in prices received by domestic producers for their output.

Industrial production: Industrial production is a measure of output of the industrial sector of the economy. The industrial sector includes manufacturing, mining, and utilities. Although these sectors contribute only a small portion of gross domestic product, they are highly sensitive to interest rates and consumer demand.

The NAHB/Wells Fargo Housing Opportunity Index (HOI) for a given area is defined as the share of homes sold in that area that would have been affordable to a family earning the local median income, based on standard mortgage underwriting criteria.

Conference Board Coincident Economic Index: The Composite Index of Coincident Indicators is an index published by the Conference Board that provides a broad-based measurement of current economic conditions, helping economists, investors, and public policymakers to determine which phase of the business cycle the economy is currently experiencing.

Conference Board Lagging Economic Index: The Composite Index of Lagging Indicators is an index published monthly by the Conference Board, used to confirm and assess the direction of the economy's movements over recent months.

New Export Index: The PMI New export orders index allows us to track international demand for a country's goods and services on a timely, monthly, basis.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

The Conference Board Leading Economic Index: Intended to forecast future economic activity, it is calculated from the values of ten key variables.

Source: FactSet, data as of 7/25/2025

J.D. Power 2025 U.S. Investor Satisfaction Study, which measures overall investor satisfaction with investment firms, was released 3/20/25, based on investors surveyed 1/24-12/24, who may be working with a financial advisor. Based on 7,876 responses from Advised Investors, 1 company out of 24 was chosen as the winner. The award is not representative of any one client’s experience, is not an endorsement, and is not indicative of an advisor’s future performance. The study is independently conducted, and the participating firms do not pay to participate. Use of study results in promotional materials is subject to a license fee. J.D. Power is not affiliated with Raymond James. For J.D. Power 2025 award information, visit jdpower.com/awards.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

© 2025 Raymond James Financial, Inc. All rights reserved.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® are registered trademarks of Raymond James Financial, Inc.

© Raymond James

Read more commentaries by Raymond James