Summary

- The substantial and steady free cash flow (FCF) generated by midstream MLPs and C-Corps sets them apart from the broader energy sector and other equities.

- Midstream is expected to continue generating FCF, even as some companies have growing project backlogs related to natural gas opportunities.

- Energy infrastructure companies are using excess cash to reward investors with dividend growth and strategic buybacks.

For years, midstream companies have generated significant free cash flow (FCF), which has differentiated them from the broader market. With balance sheets in good shape, excess cash has been used to reward shareholders with dividend growth and opportunistic equity repurchases. Even with some capex creep related to a robust outlook for natural gas demand, midstream is expected to continue enjoying free cash flow tailwinds.

Midstream Stands Out for Strong FCF Generation

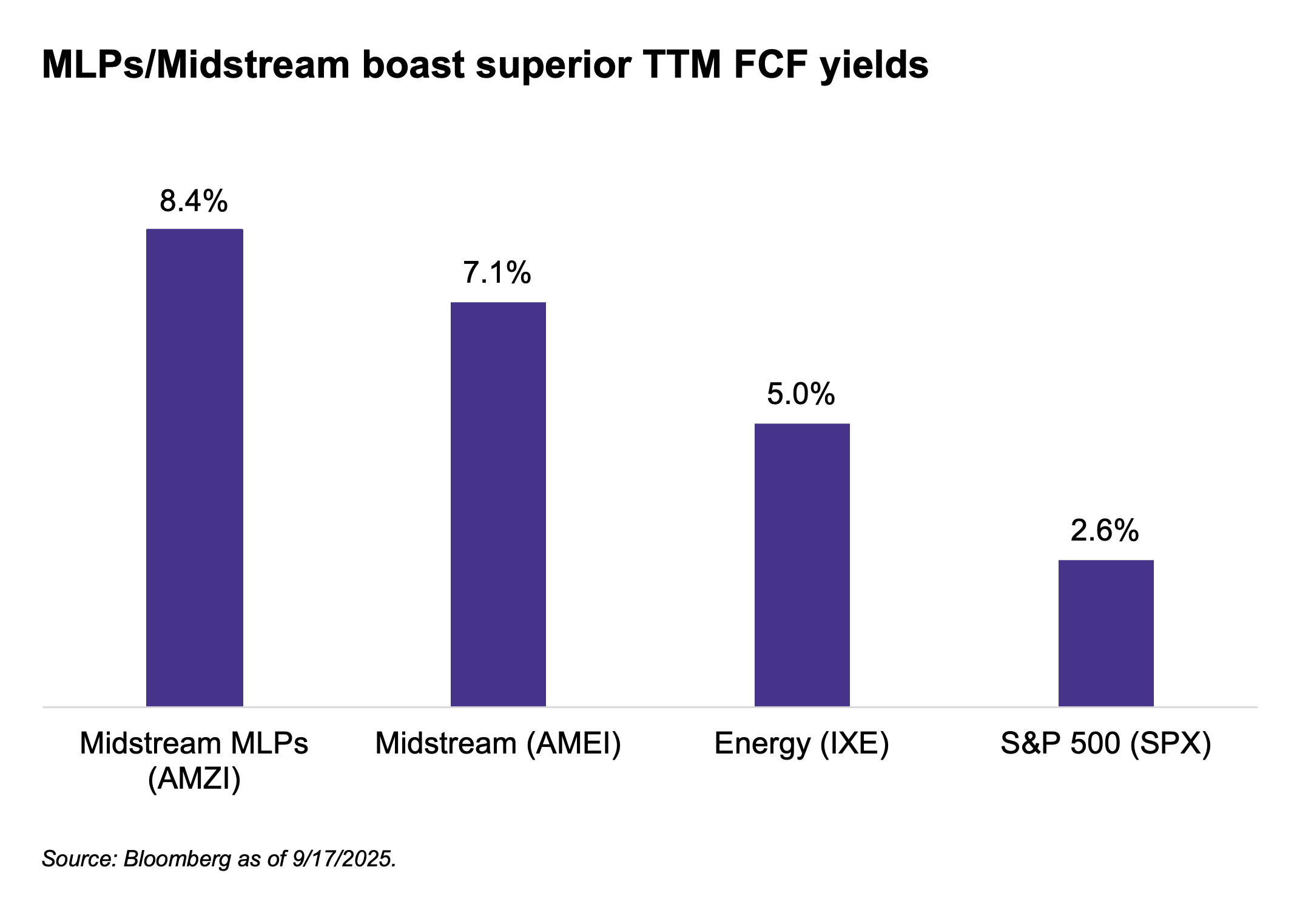

In contrast to the high-growth era of 2010–2020, when U.S. oil production more than doubled, midstream capital spending has generally moderated. This aligns with more measured oil and gas production growth in the U.S. For years, broader energy has been focused on capital discipline, free cash flow generation, and returns to shareholders. As of September 17, energy had the highest trailing 12-month FCF yield of any sector in the S&P 500 per Bloomberg.

For many energy companies, FCF generation will fluctuate somewhat with commodity prices. Higher oil and gas prices would lead to more excess cash. However, midstream’s FCF generation tends to be more sustainable and predictable. This is due to midstream’s fee-based business model backed by long-term contracts, which results in more stable cash flows. This is also why midstream companies can give year-ahead EBITDA guidance or multi-year expectations for EBITDA growth, in contrast to the rest of energy.

As shown below, midstream/MLPs have even higher trailing FCF yields than broader energy, represented by the Energy Select Sector Index (IXE). MLPs are represented by the Alerian MLP Infrastructure Index (AMZI). Midstream is represented by the Alerian Midstream Energy Select Index (AMEI), which is ~75% U.S. and Canadian midstream corporations and ~25% MLPs. From a valuation standpoint, higher FCF yields for midstream/MLPs also can serve as an indication that this space has not become expensive on a relative basis.

Midstream MLPs and corporations have used excess cash to grow their dividends. Dividends are also generous relative to the broader market and IXE. As of September 17, AMZI and AMEI were yielding 7.6% and 5.4%, respectively. While midstream companies tend to prioritize dividend growth, companies have also deployed buybacks as a tool for returning excess cash to investors.

Free Cash Flow Tailwind to Remain Intact

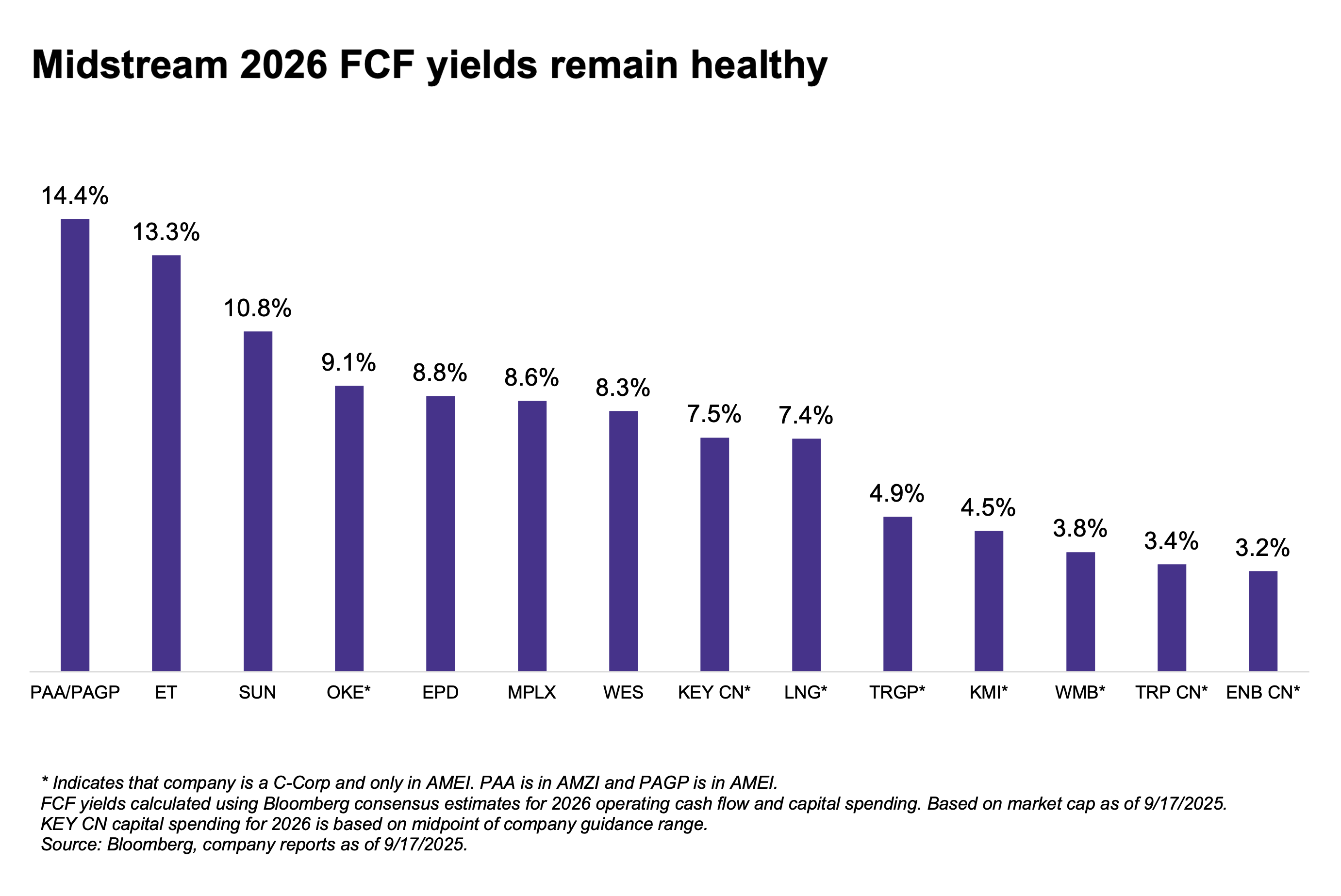

Digging a bit deeper, the chart below shows FCF yields for some of the larger constituents of AMZI and AMEI. It uses 2026 consensus estimates from Bloomberg. Consistent with the index-level TTM FCF yields, MLPs tend to have higher 2026 FCF yields than their C-Corp counterparts. This in part reflects last year’s strong gains for C-Corps with natural gas infrastructure, as well as healthy capital spending as these companies pursue natural gas pipeline projects. Even with solid gas-related project backlogs, free cash flow generation is expected to remain intact.

Notably, 10 of the 14 companies included in the chart are expected to have positive free cash flow after dividends. Four names are estimated to have more than $1 billion in excess cash after dividends, including Energy Transfer (ET), Enterprise Products Partners (EPD), Cheniere Energy (LNG), and ONEOK (OKE).

Pending transactions could cause some movement in 2026 FCF estimates for some names as analysts update their models. Names with notable deals underway including Plains All American (PAA/PAGP), Keyera (KEY CN), Sunoco (SUN), and Western Midstream (WES).

PAA/PAGP’s sale of its Canadian NGL business to KEY for $3.75 billion is expected to close in 1Q26. SUN agreed to acquire Parkland Corporation (PKI CN) in May for $9.1 billion with closing anticipated in 2H25. SUN expects the pro-forma company to generate over $1 billion of run-rate FCF after distributions (defined as adjusted distributable cash flow less distributions). Finally, WES recently announced the acquisition of Aris Water Solutions (ARIS) in a $1.5 billion deal expected to close in 4Q25. WES expects the deal to be accretive to 2026 FCF.

Why does FCF matter?

FCF enhances the overall financial flexibility of midstream MLPs and corporations. Excess cash can be used to further reduce debt or pursue bolt-on acquisitions. With strong balance sheets in place, midstream corporations and MLPs often use excess cash for dividend growth and strategic buybacks. Midstream’s FCF yields stand out from the broader energy sector and equity market overall.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research:

Short-Term Energy Outlook: September 2025 Production Overview

Midstream Prepares for More Permian Natural Gas

Midstream/MLP Buybacks Jumped in 2Q25

2Q25 MLP/Midstream Dividend Recap: MLPs Deliver Growth

Midstream/MLPs See Sustained Free Cash Flow

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, ENFR, and ALEFX, for which it receives an index licensing fee. However, AMLP, MLPB, ENFR, and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, ENFR, and ALEFX.

For more news, information, and strategy, visit the Energy Infrastructure Content Hub.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi