Summary

- The boom in artificial intelligence is driving unprecedented demand for energy to power new, large-scale data centers, creating a structural tailwind for domestic natural gas.

- With the traditional power grid unable to keep pace, midstream companies are developing critical infrastructure, including new pipelines and dedicated power plants in select cases, to provide reliable energy for tech companies.

- Midstream companies provided progress updates and new projects in 2Q25 earnings calls aimed at capturing what could become an 8.0 billion cubic feet per day (Bcf/d) incremental demand opportunity by 2030.

The rapid growth of artificial intelligence (AI) is fueling a massive buildout of power-intensive data centers, creating a significant new source of domestic energy demand. Because the traditional electric grid cannot meet the scale and speed of this new demand, tech companies are increasingly building their own dedicated power sources, with natural gas serving as a critical fuel. Midstream companies are capitalizing on this trend by developing new pipeline infrastructure and on-site power solutions, with 2Q25 earnings providing fresh updates. Today’s note provides an overview on data center spending and its implications for midstream and recaps recent updates from some of the key midstream beneficiaries.

Why data center growth is a game-changer for midstream

For the first time in two decades, U.S. electricity demand is on a sharp upward trajectory. For example, PJM Interconnection, which manages the grid for 13 states including Virginia, is forecasting peak summer electricity demand in 2035 that is 36% higher than what was anticipated for the summer of 2025. However, a struggling power grid is likely ill-suited for the speed and scale of this growth. One of the key drivers is the boom in AI, which requires massive, power-hungry data centers that need reliable, 24/7 electricity. This demand outpaces what intermittent renewables can supply alone or what the traditional grid can build quickly enough.

This has led tech giants to pursue “Bring-Your-Own-Power” solutions, where they develop dedicated, on-site power plants to ensure uninterrupted operations. Natural gas has emerged as a leading option for these facilities due to its reliability, scalability, and speed of deployment. Utilities are also turning to natural gas to support data centers. For example, Entergy (ETR) recently received approval to build over 2.2 GW (~0.39 Bcf/d) of new natural gas power plants to serve a $10 billion Meta data center in Louisiana.

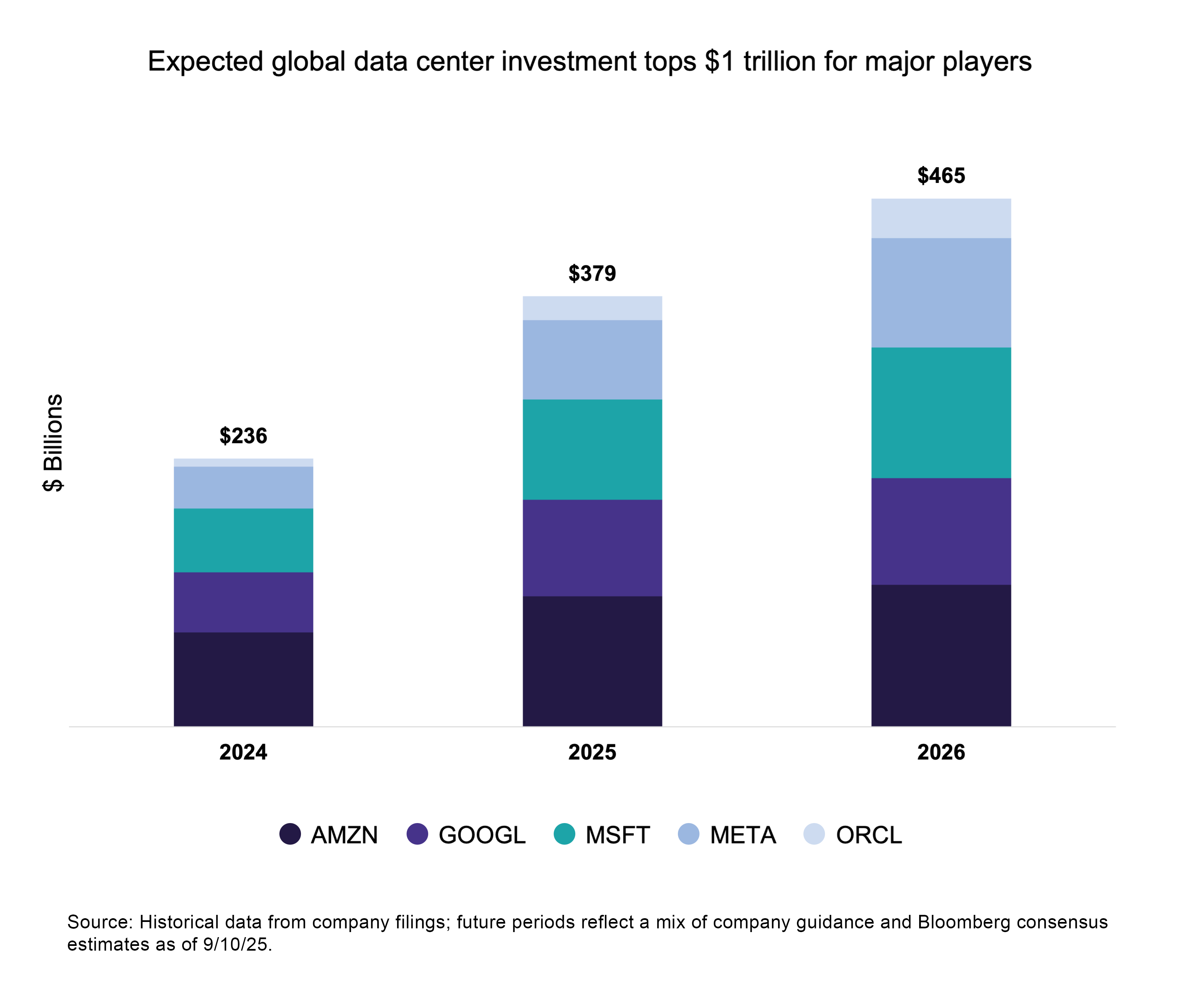

This trend is being driven by an unprecedented capital spending cycle from major tech companies. Data from the five largest players — Amazon, Google, Microsoft, Meta, and Oracle — shows a projected $1.08 trillion in collective capital expenditures from 2024 through 2026 alone. After stepping up capital expenditures by 61% in 2025, these firms are expected to increase investment by another 23% in 2026, as seen in the chart below.

Looking further ahead, analysts widely expect this spending cycle to continue growing, with McKinsey estimating that global data centers will require $6.7 trillion in capital expenditures by 2030 to keep pace with compute demand. Mega-projects like the OpenAI-led Stargate initiative, with its $500 billion U.S. investment plan through 2029, underscore the sheer scale of this capital deployment.

The potential impact on natural gas demand is significant. While estimates vary, an average of four analyst forecasts suggests AI data centers in the U.S. could require an incremental 8.0 billion cubic feet per day (Bcf/d) of natural gas by 2030. This directly benefits midstream companies, which will operate the pipeline infrastructure needed to deliver natural gas to data centers or the utilities supporting them. This data center boom represents a powerful domestic growth driver for natural gas that complements the well-established LNG export expansion (read more).

2Q25 Earnings: Updates on midstream data center strategies

2Q25 earnings provided significant new detail on how midstream is positioning to capitalize on the AI-driven data center boom. Strategies range from building dedicated behind-the-meter (BTM) power plants to undertaking pipeline expansions to serve utility customers, with each company leveraging its asset footprint.

Williams (WMB) is executing a dual strategy of direct power generation and pipeline expansions. WMB’s Power Innovation business is constructing the 400 MW (~0.07 Bcf/d) Socrates power project in Ohio backed by a 10-year agreement with Meta. During its 2Q call, WMB confirmed it has ordered equipment for two additional BTM projects and is targeting a total of 1 GW (~0.18 Bcf/d) of new capacity by 2027 from this next wave. These initiatives are part of a larger 6 GW (~1.07 Bcf/d) opportunity set of potential projects, as outlined in a recent company presentation. They are complemented by large-scale expansions on its strategically located Transco pipeline to serve broader power demand in the data center-heavy Southeast and Mid-Atlantic regions.

Energy Transfer (ET) confirmed on its 2Q call that it has now signed three deals with data centers/power plants in Texas and is close to finalizing two more. This builds upon its partnership with CloudBurst announced in February, which involves a 10-year agreement to supply up to 0.45 Bcf/d of natural gas to an AI-focused data center. A separate BTM hyperscaler contract was highlighted as having recently upsized its volume commitment almost five-fold to 0.38 Bcf/d, with the potential for further upside. Additionally, ET has reached a Final Investment Decision (FID) on its massive $5.3 billion Desert Southwest Pipeline. This 1.5 Bcf/d project will move Permian gas to high-growth markets in Arizona and the Southwest.

Enbridge (ENB CN) is capturing demand through both its renewable and natural gas businesses. On the renewables side, the company sanctioned the $900 million Clear Fork solar project in Texas for a Meta data center. On the natural gas side, ENB is focused on serving utility customers who are building new power generation. During its 2Q call, management reiterated that its gas systems are within 50 miles of 29 new data centers and numerous power plants. The company is expanding its Texas Eastern and Southeast Supply Header pipelines to help meet growing power demand, including from data centers.

Kinder Morgan (KMI) has announced large-scale pipeline projects as well. The company confirmed on its 2Q call that 50% of its $9.3 billion project backlog is dedicated to serving power demand. Projects include the South System Expansion 4 in the Southeast and the Mississippi Crossing project for the Tennessee Gas Pipeline.

TC Energy (TRP CN) is seeing significant inbound interest for its pipelines, confirming on its 2Q call that it’s in discussions with over 30 counterparties to serve data center-driven power demand. Its recently announced Northwoods project, a $900 million expansion in the Midwest, serves this market and is backed by a 20-year, take-or-pay contract with an investment-grade utility.

Pembina Pipeline (PPL CN) is developing an integrated power and natural gas solution to support a new data center in Alberta. Through its Greenlight Electricity partnership, the company is pursuing a 1.9 GW (0.34 Bcf/d) gas-fired power plant and is in active commercial discussions with a data center customer. This potential project could support an expansion of the nearby Alliance pipeline.

Investing in data centers through midstream

For investors looking to gain exposure to the growth in natural gas demand driven by data centers, midstream energy infrastructure offers a compelling option. Many of the key players at the forefront of this theme, including WMB, KMI, ET, ENB CN, TRP CN, PPL CN, and KMI, are constituents of the Alerian Midstream Energy Select Index (AMEI). Energy infrastructure also tends to offer attractive yields, supported by fee-based businesses that provide some insulation from commodity price fluctuations. AMEI was yielding 5.4% as of September 10.

Bottom line

The AI-driven data center boom is adding to a structural tailwind for U.S. natural gas demand driven by rising electricity needs. Paired with the ongoing buildout of LNG export capacity, this powerful, dual-engine growth narrative represents an important tailwind for midstream, which stands to benefit from rising natural gas demand and supply.

A replay is now available on-demand for our recent 60-minute webcast, “Checking MLP/Midstream Fundamentals as 2026 Approaches.”

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research:

Sizing Up the Next Wave of U.S. LNG Export Projects

MLP/Midstream Earnings So Far: Gas, Dividends, OBBBA & More

Kinder Morgan Q2 Results: Natural Gas Trends Drive Constructive Outlook

Rising Electricity Demand Needs Natural Gas & Midstream

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for ENFR and ALEFX, for which it receives an index licensing fee. However, ENFR and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of ENFR and ALEFX.

For more news, information, and strategy, visit the Energy Infrastructure Content Hub.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi