Getting emerging market exposure is a viable option in the current market environment. That's especially so given the global de-dollarization and prospect of further rate cuts by the Federal Reserve. China has long been a hallmark when it comes to getting EM exposure. But the economic and geopolitical challenges the country is facing creates a conundrum. Should investors include China, the top economy in EM, or simply avoid it?

U.S. Pension Funds Avoid China

The London Stock Exchange Group (LSEG) noted that institutional investors have increasingly divested their exposure to assets tied to the second-largest global economy, especially in the United States. For example, laws in the U.S. have mandated pensions funds to purge their holdings in China. That is an about-face compared to the $68 billion that went into China from the years 2021 to 2023.

As indicated by the LSEG, Indiana ordered its public retirement system to exit $1.2 billion of its China holdings last year. Likewise, an executive order in Texas called for state agencies to sell their China assets, including $1.4 billion in assets held by the state's Teachers Retirement System. Furthermore, it's not just pension funds being asked to lop off their China exposure.

"The scope of these efforts extends beyond pensions, with restrictions on areas such as Chinese-made technology, farmland purchases, and procurement contracts. In total, more than 20 states now have some form of restriction in place," noted Catherine Yoshimoto, LSEG director of product management/benchmark product development.

Should investors follow suit and look the other way when presented with an opportunity to invest in China? There are investment cases that counter, but also uphold the need for China exposure.

Yes, I'll Take China Exposure

China's gargantuan size is readily apparent in key data points like global population and gross domestic product (GDP). Furthermore, the economy is still growing, so it has immense potential in terms of future growth prospects. It's already a global economic powerhouse. That's thanks to its growing global manufacturing sector and advancements in technology, including AI.

"China’s sheer GDP size and capital market size have given the country a prominent position among the EM complex, to the extent that when China sneezes, emerging markets catch a cold," LSEG noted in another research report.

That theme of AI will play a critical role in China's economic dominance moving forward. According to research organization RAND, China is looking to become the global leader in AI by the year 2030.

"China’s AI industrial policy will likely accelerate the country’s rapid progress in AI, particularly through support for research, talent, subsidized compute, and applications," RAND noted.

From an investment standpoint, China offers diversification benefits that can complement a portfolio that's tilted heavily toward U.S. equities. China's equities march to the beat of its own drum, with data from Morningstar showing the discorrelation with U.S. markets.

"Over the trailing three-year period through May 2025, China’s equity market has had a correlation coefficient of just 0.12 when measured against the Morningstar US Market Index, compared with about 0.6 for the broader emerging market benchmark," Morningstar noted.

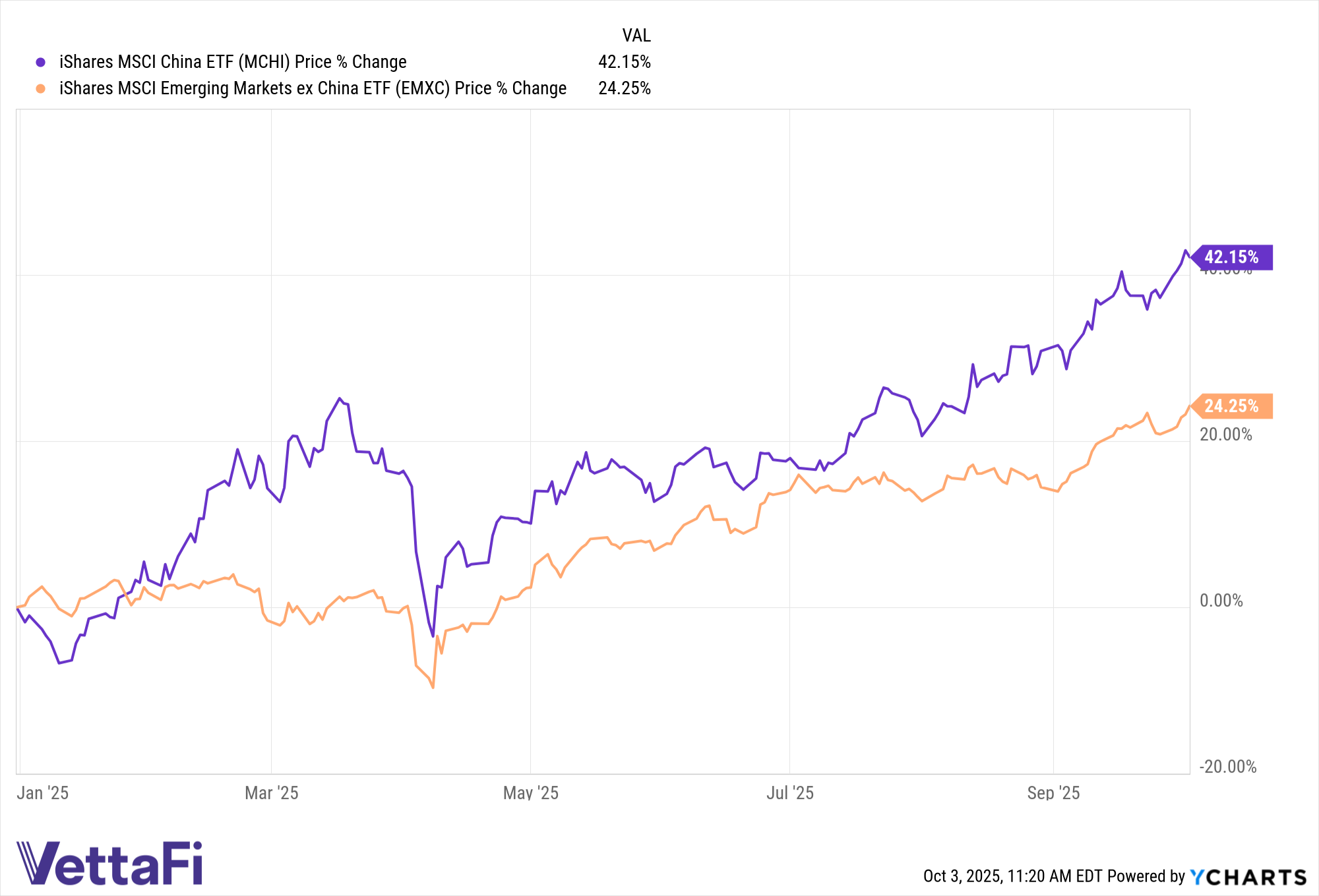

Last, but not least the investment performance is on the side of China exposure when looking at a pair of ETFs as a gauge. Comparing the YTD performance of the iShares MSCI China ETF (MCHI) and the iShares MSCI Emerging Markets ex China ETF (EMXC) underscores the outperformance of the former over the latter.

MCHI data by YCharts

Hold the China Exposure, Please

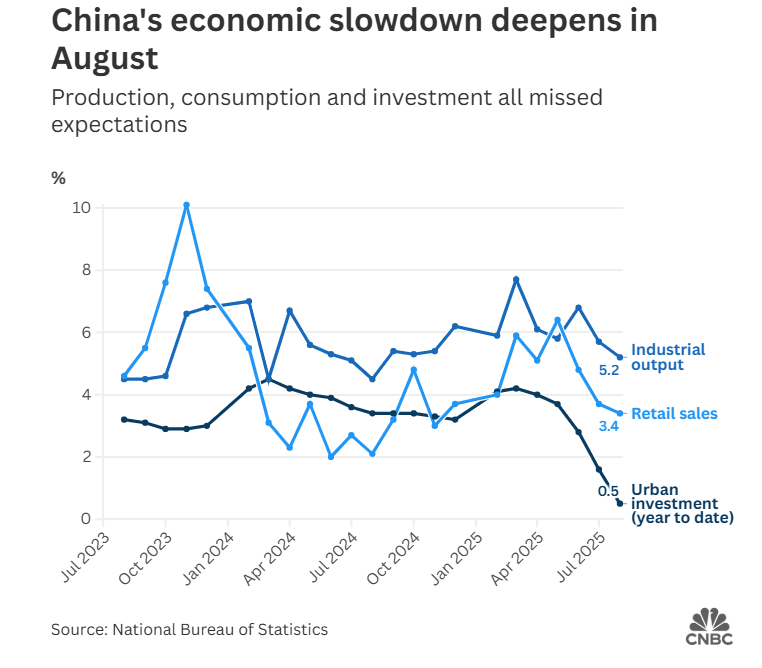

Of course, every argument has two sides. China continues to deal with the after-effects of a real estate development crisis back in 2021. However, the government continues to earmark funds for stimulus measures to resuscitate its economy. The fundamental outlook supports growth in the long-term investment horizon. But the country must still overcome the economic obstacles stagnating its growth today. That path to recovery doesn't get easier when factoring in tariff spats with the United States.

“We should be aware that there are many unstable and uncertain factors in (the) external environment, and national economic development is still confronted with multiple risks and challenges,” the National Bureau of Statistics told CNBC.

Also, size doesn't necessarily translate to market success, as Morningstar research expertly pointed out. A large portion of China's publicly traded firms are run by state-owned enterprises. Those SOEs carry their own unique set of risks.

"While less than a third of listed firms in China are state-owned, those companies account for a large percentage of the market based on market cap, revenue, and earnings," Morningstar said. "Related-party transactions, insider trading, questionable capital allocations, and complex ties between politicians and management teams have all been long-standing concerns."

Because of these reasons, some investors are opting to keep China out of their EM exposure, at least in the interim. China equities could offer investors a value-oriented play. But due diligence and patience are a must if they're willing to take that gamble.

"China’s growing weight and its unique risk and opportunity profiles have fueled the need for investors to better manage the risk that comes with an allocation to China," LSEG noted. "For these investors, this has necessitated the separation of China from the rest of the emerging markets investment opportunity set."

ETFs With or Without China Exposure

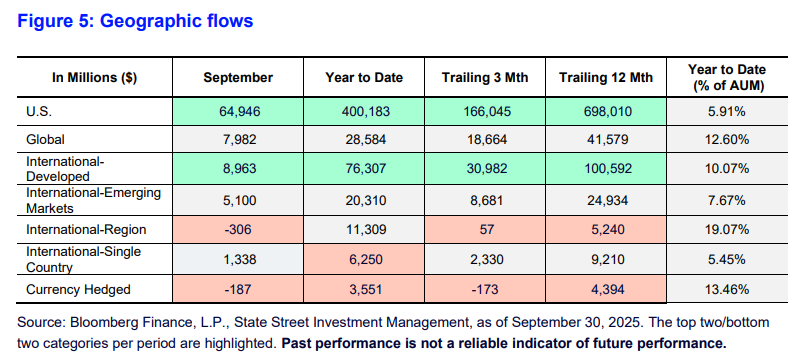

ETFs offer a window to exposure to EM equities whether investors are looking to retain or stay away from China. ETF inflows have been relatively strong for EM this year. They account for 7.67% of AUM, based on research data from State Street Investment Management. Furthermore, despite the country's macroeconomic challenges, China-focused ETFs saw strong inflows in September as well as the entire year.

"For single-country ETFs, China-focused ETFs led inflows (+$1.2 billion)—matching the interest for broad EM," noted State Street Investment Management Global Head of Research Matthew Bartolini. "Given the sizable recent rally (+20% over the past three months for Chinese equities), China-focused ETFs have taken in $3.4 billion over the past three months and are almost in positive territory for the year after witnessing large outflows around Liberation Day (-$4.2 billion in April)," he said.

Investors looking for broad China equities exposure will want to look at funds like the previously mentioned iShares MSCI China ETF (MCHI) and the Franklin FTSE China ETF (FLCH). ETFs like the iShares MSCI China Small-Cap ETF (ECNS) allow investors to tailor their exposure to market-cap sizes.

Investors also have the option to target their China exposure to specific sectors like technology with the Invesco China Technology ETF (CQQQ) or consumer discretionary with the MSCI China Consumer Discretionary ETF (CHIQ). KraneShares offers a plethora of ETFs for targeted China equities exposure in various sectors like healthcare, with the KraneShares MSCI All China Health Care Index ETF (KURE).

Those insistent on EM exposure without allocating to China can look at funds like the aforementioned iShares MSCI Emerging Markets ex China ETF (EMXC), the SPDR S&P Emerging Markets ex-China ETF (XCNY), and the KraneShares MSCI Emerging Markets ex China Index ETF (KEMX). And Vanguard debuted its Vanguard Emerging Markets ex-China ETF (VEXC) just recently.

Broader Is Better?

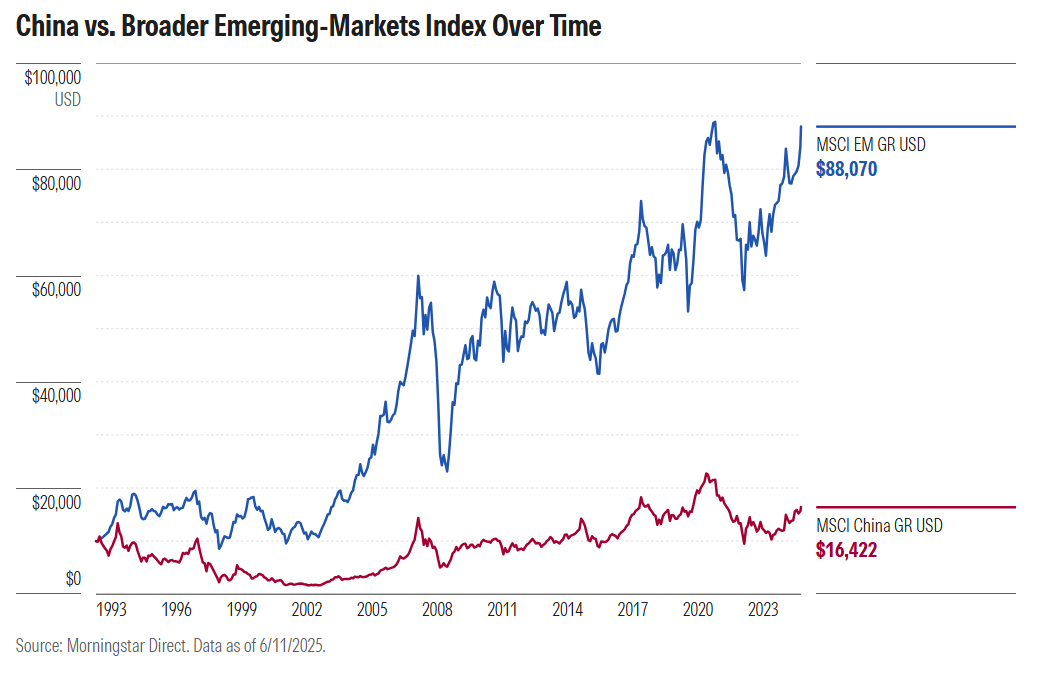

Of course, investors aren't relegated to choosing one or the other. Morningstar data showed that from 1993, broad exposure to EM can be more beneficial to investors when considering a hypothetical $10,000 investment to the MSCI Emerging Markets Index compared to the MSCI China Index.

Those who aren't discerning about China exposure can opt for broad-based EM options like the iShares Core MSCI Emerging Markets ETF (IEMG), the Vanguard FTSE Emerging Markets ETF (VWO), and the SPDR Portfolio Emerging Markets ETF (SPEM).

Prepare your bond portfolio for changing market conditions. Register today for the Fixed Income Symposium on Sept. 18, 2025, 11AM ET / 8AM PT.

Read more commentaries by VettaFi