Optimize Wealth Transfer with a Step-up in Cost Basis Strategy

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAs a result of the One Big Beautiful Bill Act, the lifetime exclusion for gifts and estates will increase permanently to $15 million next year with annual inflation adjustments to follow.

For the past few years, there’s been speculation on the exclusion amount, which was scheduled to be reduced roughly by half in 2026. The new law brings much-needed clarity for planning purposes, with the caveat that future legislation could bring changes. However, the absence of an expiration date, or “sunset” in the law is helpful. At this exclusion level, the overwhelming majority of estates will not be subject to federal estate taxes.

Should wealth transfer planning focus more on income taxes?

For those planning to transfer wealth to heirs, if estate taxes are not a concern, are there considerations for passing assets more efficiently from an income tax perspective? One of the most valuable features of the tax code is step-up in cost basis on certain property passed upon death, such as taxable investment accounts, real estate and other assets. Those inheriting appreciated assets at death may avoid significant capital gains taxes since the cost basis of the inherited asset is “stepped-up” to the value at the date of death.

Some assets do not receive a step-up in cost basis on the owner’s death. These include retirement accounts, IRAs, annuities, or assets held in an irrevocable trust, for example.

However, when a lifetime gift is made, the recipient of the gift generally inherits the original cost basis of the property. From a tax minimization perspective, it may be more beneficial to pass appreciated assets at death instead, subject to other factors based on the circumstances.

Reviewing estate plans may uncover tax savings opportunities

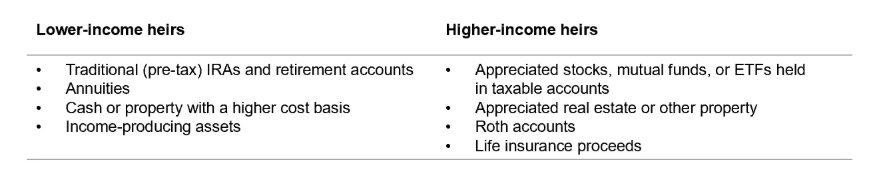

More tax-efficient wealth transfer may involve leaving assets or property to heirs based on their tax circumstances. For example, pre-tax, traditional retirement accounts and IRAs are taxed as ordinary income when distributed. Most non-spouse beneficiaries are forced to fully distribute these accounts within 10 years as a result of the SECURE Act. As a result, from an income-tax perspective, leaving these accounts to heirs in higher tax brackets may not be an efficient way to transfer wealth. Assets or property that may benefit from a step-up in cost basis may be much more tax efficient depending on the tax profile of the heir. Proceeds from a life insurance policy, which pass free of income taxes to beneficiaries, can also be a more tax efficient way to pass wealth. For this reason, an estate plan that contemplates which property or accounts to leave to specific heirs based on tax circumstances may result in a greater amount of post-tax wealth being transferred.

Considerations on which assets to leave to which heirs

Gifting appreciated property to older family members

Given the significant tax benefit of step-up in cost basis tax treatment at death, some may wonder if there may be a loophole to gift appreciated assets to an older family member with an eye toward eventually inheriting the asset back and benefitting from a step-up in cost basis. The IRS restricts these types of deathbed transfers for tax purposes. For step-up to apply on property that was gifted in this circumstance, the older family member has to live more than one year following the gift. There may be other concerns with this strategy. For example, the gifted asset would be considered part of the older family member’s estate, and there is no guarantee that the person who gifted the asset would inherit it back at death. The gifted asset could also be considered a countable asset for purposes of determining long-term care eligibility under Medicaid. Lastly, the “more than one year” limitation on step-up in cost basis also applies to gifts between spouses.

Understand how step-up applies to jointly owned property

Consider a married couple owning an appreciated asset as Joint Tenants with Rights of Survivorship (JTWROS) that was purchased for $100,000 years ago and is valued at $500,000 when one of the spouses passes away. Only the deceased spouse’s portion would receive step-up in cost basis treatment. The resulting cost basis on the property for the surviving spouse would be $300,000. This is comprised of their original portion of cost basis for the surviving spouse ($50,000, representing half of the purchase price) plus the stepped-up portion of the deceased spouse’s cost basis ($250,000). If the entire property was owned by the deceased spouse, and left to the surviving spouse upon death, the cost basis of the property would have been stepped-up to $500,000. This treatment would also apply to property owned as Joint Tenants by Right of Entirety. Property owned jointly in community property states may benefit from a full step-up in cost basis at the death of the first spouse. These states include Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin. Additional states may allow residents to opt in to community property treatment on certain jointly owned property. Specific state laws will vary.

Preserve option to apply step-up on property held in trusts

Appreciated property held in an irrevocable trust does not generally benefit from a step-up in cost basis at the death of the grantor. However, the tax code (under IRC Section 675(4)©) allows property within an irrevocable trust to be substituted with other property of equal value. With a swap power, a trustee can swap out low-basis assets held inside the trust with higher-basis assets owned by the grantor. After the swap, the low basis assets held outside of the irrevocable trust could benefit from a stepped-up cost basis upon the grantor’s death. The rules around incorporating swap powers within a trust are complicated, and because they may impact who is treated as the taxable party, it is critical to work with a qualified trust planning attorney.

Optimizing wealth transfer

Step-up in cost basis is a key provision that impacts the value and tax status of assets left to heirs. It is important to understand the different tax treatments of assets in identifying heirs and crafting a plan for wealth transfer. The rules around step-up cost basis are complex. It is important to seek professional advice and work with a qualified estate planner or trust planning attorney.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All