Key takeaways

- Benefit payments can help or hinder a pension’s plan funded status.

- Overfunded plans gain from “benefit payment lift,” which increases their funded status. Today, roughly half of all plans are overfunded.

- As funded status rises, the idea of plan hibernation may become more attractive, enabling strategic use of pension surplus.

I recently visited the Smithsonian Air & Space Museum with my 11-year-old son, where we saw the original plane flown by the Wright brothers in 1903. The plane was larger than I expected, and the first flight was shorter than I thought, but somehow, they managed to crack the code on how to make a machine fly. They did this by overcoming significant opposing forces.

A plane trying to take off has two main obstacles to overcome: weight and drag. Weight is forced by gravity and drag by air resistance. Planes overcome these factors with thrust and lift. Thrust comes from powerful engines and lift from the wings.

Ironically, both drag and lift are caused by air, which can either resist a plane’s motion or help it rise. Pension plans also face forces that either hold them back or propel them forward: obligations, contributions and investment returns.

The weight of obligations

The weight of a pension plan is the future obligation to pay benefit payments. It weighs less when rates are higher (as they were in 2022) but more when they are lower (protected by LDI strategies). Thrust comes from contributions and investment returns. A larger engine is like a more generous funding policy or aggressive asset allocation. Drag and lift also have their analogs, both arising from the payment of benefits. Most recently, more plans are experiencing the lift.

When payments hold you back

Underfunded pension plans face a significant challenge to becoming fully funded, simply because they are always paying out benefit payments. Pension risk transfer can magnify this problem. What we refer to as “benefit payment drag” comes from paying out a higher portion of assets than liabilities. Benefit payments are paid out at a 100% level whether the plan is fully funded or not. This means when an underfunded plan pays benefits, its funded status decreases.

Let’s take a simple example. A plan has $400 million in assets and $500 million in liabilities, or an 80% funded status. Now, what if it pays out $100 million in benefit payments? The plan is left with $300 million in assets and $400 million in liabilities. Its funded status percentage drops by 5% and is now 75% funded. That’s benefit payment drag, and it requires added “thrust” (i.e., returns or contributions) to overcome. The low funded status causes effective returns to be throttled down.

This illustrates one of the reasons it took so long for corporate pension plans to become fully funded again after the Global Financial Crisis. Plans typically pay out 5-10% of their plan assets each year in benefit payments, meaning the worse funded the plan is, the greater the impact of benefit payment drag.

For instance, an 80% funded plan paying out 7% of assets annually requires an additional 1.5% in return each year just to tread water (or pay the equivalent in contributions). That increases to 1.8% for a 75% funded plan. In short, the more underfunded you are, the harder it is to escape the cycle.

When payments push you forward

Now that about half of pension plans are overfunded, many plan sponsors are finding it relatively easy to maintain and improve their pension surpluses, due to “benefit payment lift.”

Let’s consider the same example as before but with a well-funded plan. The plan has $600 million in assets and $500 million in liabilities, or a funded status of120%. If it pays out $100 million in benefit payments, it’s left with $500 million in assets and $400 million liabilities—or a funded status of 125%, which is a 5% increase. This is equivalent to having an additional 1.5% in return just by letting the plan run its course. That’s benefit payment lift—and it means well-funded plans can improve their position simply by letting benefit payments work in their favor.

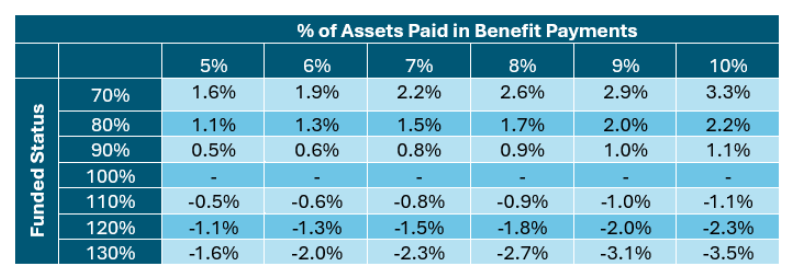

As the chart shows, there are a range of impacts on additional return needed (or underperformance that could be tolerated) for various levels of funded status and percentage of assets paid in benefit payments to maintain the current funded status.

Additional return needed due to the payment of benefit payments

In short, the higher the funded status, the more benefit payments work as a tailwind rather than a drag.

Considering the value of pension surplus

Where does this leave plan sponsors with overfunded plans? While plan termination is an option, plan hibernation can appear even more compelling if funded status is increasing. This opens the door to discussions on using plan surplus, which can lead to changes in asset allocation for overfunded plans. The overfunded plan has an additional buffer to perhaps take on a riskier portfolio to generate additional return.

Rather than a simple asset allocation at the end of the glidepath currently favored by many, newer investment strategies like LDI diversifiers that offer additional return can be more compelling. This excess return potential becomes more valuable if current proposals to use excess pension assets in defined contribution plans come to fruition.

Looking ahead

As sponsors shift from survival to optimization, recognizing the dual role of benefit payments—drag and lift—will be key. Those who harness the lift of surplus can better align their portfolios with both participant security and long-term corporate goals.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Important information pertaining to the hypothetical example: Past performance does not predict future returns. Return level is proportionately scaled in line with cash level to be overlaid. Source: Russell Investments. Assumptions: Average cash level 1.0%, 10-year history from 12/31/2023, gross of fees. Opportunity cost from not securitizing cash varies by asset allocation and time period, and is represented by horizontal bars as marked within the chart legend. Target asset allocation used: 0% cash, 74% MSCI World, 26% Global Aggregate (GBP Hedged). For illustrative purposes only. Does not represent any actual investment. Indexes are unmanaged and cannot be invested in directly. Performance benefit (net) of overlaying cash by last 5 individual calendar year is as follows: 2023:20 bps, 2022:-17bps, 2021:16bps, 2020:14bps, 2019:23bps.

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Diversification and strategic asset allocation do not assure a profit or guarantee against loss in declining markets.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The Russell Investments logo is a trademark and service mark of Russell Investments

The information, analyses and opinions set forth herein are intended to serve as general information only and should not be relied upon by any individual or entity as advice or recommendations specific to that individual entity. Anyone using this material should consult with their own attorney, accountant, financial or tax adviser or consultants on whom they rely for investment advice specific to their own circumstances.

Products and services described on this website are intended for United States residents only. Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained on this website should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional. Persons outside the United States may find more information about products and services available within their jurisdictions by going to Russell Investments' Worldwide site.

Russell Investments is committed to ensuring digital accessibility for people with disabilities. We are continually improving the user experience for everyone, and applying the relevant accessibility standards.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates Management, L.P., with a significant minority stake held by funds managed by Reverence Capital Partners, L.P. Certain of Russell Investments' employees and Hamilton Lane Advisors, LLC also hold minority, non-controlling, ownership stakes.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

© Russell Investments Group, LLC. 1995-2025. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

© Russell Investments

Read more commentaries by Russell Investments