Rare earth elements have become the latest flashpoint in the collision between geopolitics and markets. China’s surprise tightening of export controls on key rare earth minerals, used in semiconductors, electric vehicles, defense systems, and clean energy technologies, has rattled investors and reignited fears of a new trade war. While political tensions dominate headlines, the investment and macroeconomic implications are just as consequential.

A Fragile Equilibrium Between Growth and Geopolitics

For years, markets have grown comfortable navigating geopolitical noise. But in our view this latest move is different. Rare earths are not just another export category; they sit at the foundation of the modern economy.

China controls more than 70% of global production and over 80% of global processing capacity. By restricting access to these materials, Beijing is exercising one of its few remaining pressure points against the West.

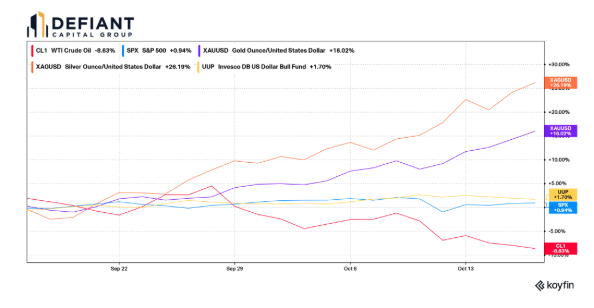

The timing of the recent announcement is notable (Bloomberg: Xi’s Rare Earth ‘Bazooka’ Sparks Global Alarm). The US economy has shown signs of slowing (2025 4Q Outlook: Shifting Gears), and inflation has moderated enough to put further rate cuts back on the table. Risk assets had rallied in response, until the sudden reminder that global supply chains remain vulnerable to political decisions rather than economic fundamentals. The result: a sharp reversal in equity markets, a flight to gold and the dollar, and heightened volatility across commodities and technology shares.

What It Means for Investors

While this episode may appear to be a temporary political maneuver, it underscores a longer-term investment theme: resource security as a macro driver. Countries are now competing not only for market share but for control over critical inputs that underpin innovation, defense, and clean energy transitions.

This has several implications for portfolios:

-

Reassessing Commodity Exposure: The rare earth shock highlights the fragility of supply chains concentrated in one geography. Investors should evaluate exposure to producers and processors outside China, particularly in Australia, Canada, and the U.S. These markets may see sustained capital inflows as governments provide incentives for domestic production.

-

Strategic Real Assets and Infrastructure: As the world reconfigures supply chains, demand for new infrastructure will rise. From mineral processing facilities to semiconductor fabs and energy storage plants, this transition creates opportunities across industrial and infrastructure investment themes.

-

Technology and Defense Implications: Semiconductors, EVs, and defense systems all rely heavily on rare earth materials. Any sustained disruption could create short-term earnings headwinds but also catalyze innovation in material science and recycling. Investors with a longer horizon should watch for emerging opportunities in alternative materials and next-generation technologies.

The Broader Macro Landscape

The macroeconomic backdrop complicates matters further. The Trump and has hinted at retaliatory tariffs and export restrictions, while central banks face a delicate balancing act between supporting growth and containing volatility-driven inflation risk. A full-blown trade escalation would dampen global trade volumes, tighten financial conditions, and potentially reignite inflation through higher input costs.

In the near term, volatility may remain elevated, particularly in sectors tied to global manufacturing and technology. However, much like previous trade flare-ups, the political incentives on both sides should eventually lead to a temporary truce. Still, the longer-term trend is clear: the world is moving toward a more fragmented, regionally self-sufficient economic order.

The Investment View: From Fragility to Resilience

We view this as a pivotal moment for investors to reassess global exposure and consider how political risks can ripple through portfolios. Diversification today means more than asset classes, it means geopolitical diversification. Portfolios overly concentrated in global supply chains or single-country dependencies face growing vulnerability.

While rare earth tensions may ease in the coming weeks, they serve as a reminder that strategic resources are becoming tools of diplomacy. Investors should anticipate continued volatility but also recognize that moments like these often reset valuations and create opportunities. Building resilience, maintaining liquidity, and positioning for real-asset exposure remain prudent strategies.

Please read important disclosures here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group