The tradeoffs, drivers, and management of the Federal Reserve’s balance sheet have come back into market focus this month with Chairman Powell shifting market expectations for the end of quantitative tightening. In an effort to anesthetize any discomfort from reading this article, we’ll summarize the most market-relevant points about the Fed balance sheet at this juncture:

- Discussions about an optimal size of the Fed’s balance sheet are increasingly at odds with the diverse drivers of how this ledger interacts with a shifting regulatory environment. Changes in the composition of Fed assets and liabilities – arising from the rapidly shifting incentives of market participants – are much more market-relevant than any arbitrary size target expressed in terms of trillions of dollars or % of GDP.

- There has been a material tightening of US banking sector liquidity this autumn that—awkwardly—can be most directly attributed to the cash holding preferences of the US Treasury. The Treasury General Account (TGA)1 has been an increasingly important determinant of US financial conditions in the last few debt ceiling standoffs in a way that is undermining the Fed’s control of reserve levels in the commercial banking system.

- There appears to be a deteriorating consensus at the FOMC around the current balance sheet tradeoffs. Policymaker speeches indicate a wide range of views on the relevant metrics, areas for policy focus, and future target states; this could create market uncertainty in the next financial market disruption or economic downturn.

We see the current state of Fed balance sheet management and communication challenges as an additional symptom of fiscal-monetary entanglement, where operational central bank independence is being eroded by the US Treasury. Given the rising dominance of fiscal policy as a driver of the economy and markets, we’ve developed a suite of fiscal policy signals in recent years have helped to inform portfolio positioning in this complex policy environment. In September, the sharp tightening of US liquidity conditions from the TGA re-build helped to inform our reduction of directional equity exposure in the Tactical Opportunities Fund.

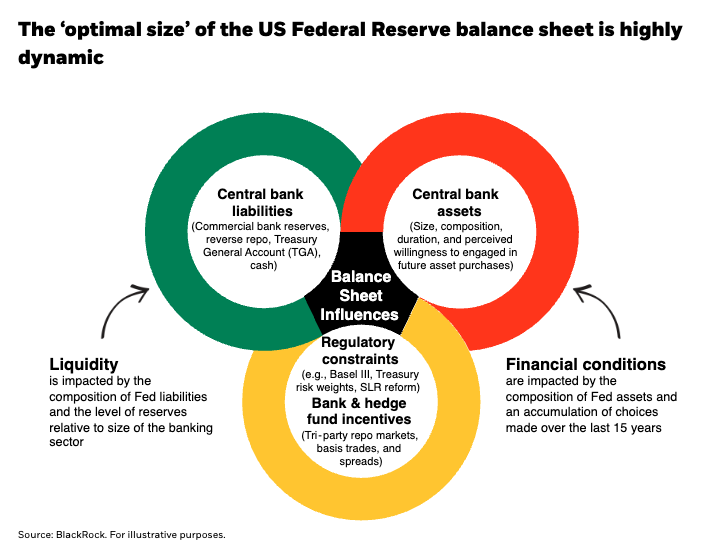

Size is an increasingly unstable target variable

The Federal Reserve’s messaging about the balance sheet is typically framed in terms of notional amounts of asset purchases, sales, levels of reserves, and overall size – targets and timelines of $trillions and $billions. Instead, we model the influence of the balance sheet on markets and the economy as a dynamic and complex interaction between the composition of assets, composition of liabilities, and changes in financial market regulation/incentives – it’s not the size that matters. The visual below describes some of these interlinkages and distinguishes between the financial conditions impact of the asset holdings versus the liquidity role of the liabilities side of the balance sheet.

Last year we discussed the shortcomings of the Fed’s size-based QT framework as it related to the asset side of the Fed’s balance sheet; QT2’s asset runoff of short-dated securities maintained relatively loose US financial conditions because the duration footprint of the balance sheet did not decline by much.2 This summer our focus shifted to the liability side of the ledger and the large swings in the composition stemming from the debt ceiling standoff and the ongoing US government shutdown; as we head into the end of 2025 a rapid decline in US bank reserves and tightening liquidity conditions have been our main area of focus.

US Treasury’s increasing influence on US commercial bank liquidity

The US Federal Government, like any going concern, needs to maintain working capital and a cash balance to manage its ongoing operations. Prior to 2008, when the Federal Reserve implemented monetary policy under a scarce reserves regime, the US Treasury dispersed its cash holdings throughout the commercial banking sector. With the inception of large-scale asset purchases and the adoption of an abundant reserves monetary policy regime in 2008, Uncle Sam had a financial incentive to shift its checking account to the Fed. That meant that the TGA transitioned from a stable line item to an increasingly volatile liability on the Fed’s balance sheet.3 Over the last 16 years these TGA cash balances have become larger and more variable and thereby an increasingly meaningful determinant of the composition of the Fed’s liabilities and US banking sector liquidity.

The impact of swings in the TGA can be most clearly identified during the seven debt ceiling standoffs over the past decade. These events have catalyzed US Treasury cash drawdowns and builds that have resulted in 5-20% swings in the liabilities composition of the Fed balance sheet. These TGA changes mechanically crowd out US commercial bank reserve balances at the Fed and determine the amount of liquidity in the commercial banking system. A larger US fiscal policy footprint in the economy, a more short-dated Treasury debt maturity structure, and a smaller Fed balance sheet means that the TGA can be a first order driver of commercial bank liquidity for the economy.4

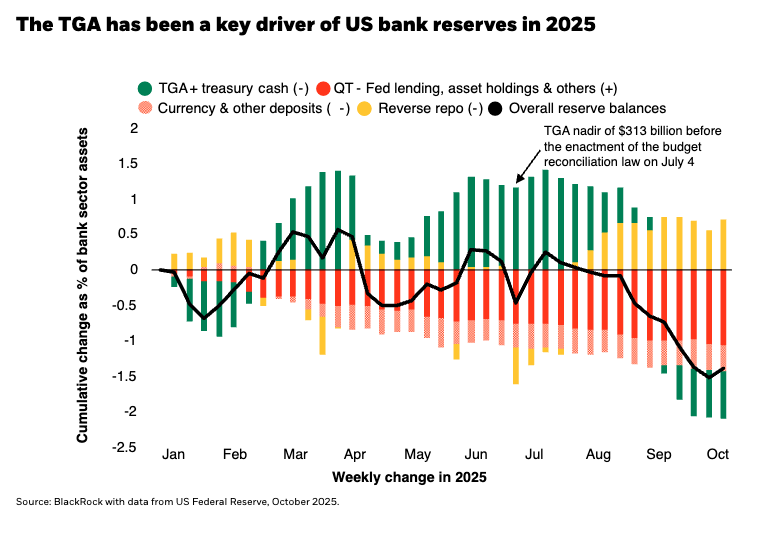

The latest instance of the TGA driving bank liquidity can be seen in the chart below where the Treasury’s TGA drawdown (represented by rising green bars) in the first half 2025 more than fully offset the bank reserve tightening effects of the Fed’s QT program (represented by the red bars). The passage of the OBBBA ended this latest debt ceiling standoff and the US Treasury initiated a rapid rebuild of the TGA in the late summer that has increased its size to nearly $1 trillion. That catalyzed a sharp 2% decline in US banking system reserves that has rapidly tightened US liquidity conditions over the last couple of months.

Sterilize the TGA

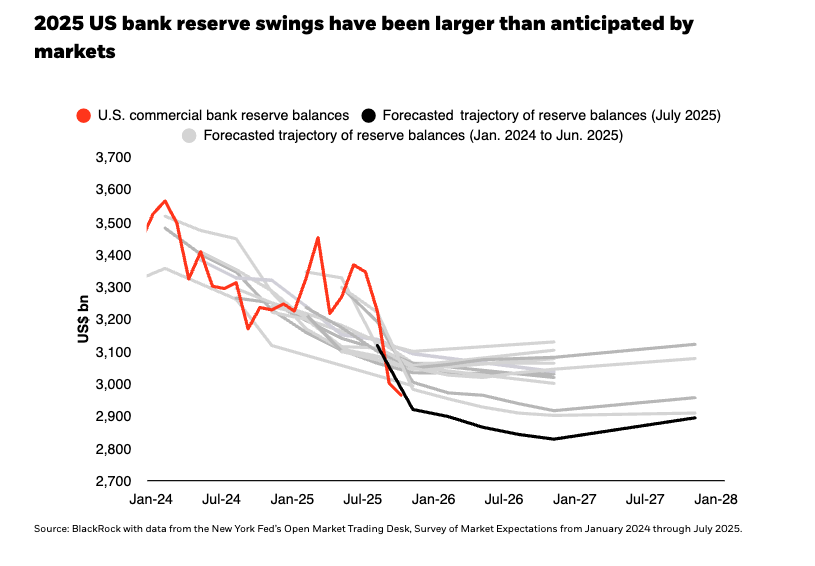

Another way to visualize the outsized swings of 2025 banking sector liquidity can be seen in the chart below that compares US bank reserve balances with the rolling series of market expectations. Both the jump in reserves in the first half of the year and the more recent collapse in reserves this autumn caught forecasters by surprise. The fiscal origins of this high velocity tightening of bank liquidity was described in the September FOMC meeting minutes as, “Reserves fell sharply on September 15 in response to an increase in the TGA, driven by tax receipts and significant net issuance of Treasury coupon securities…There were some signs of upward pressure on rates.”5

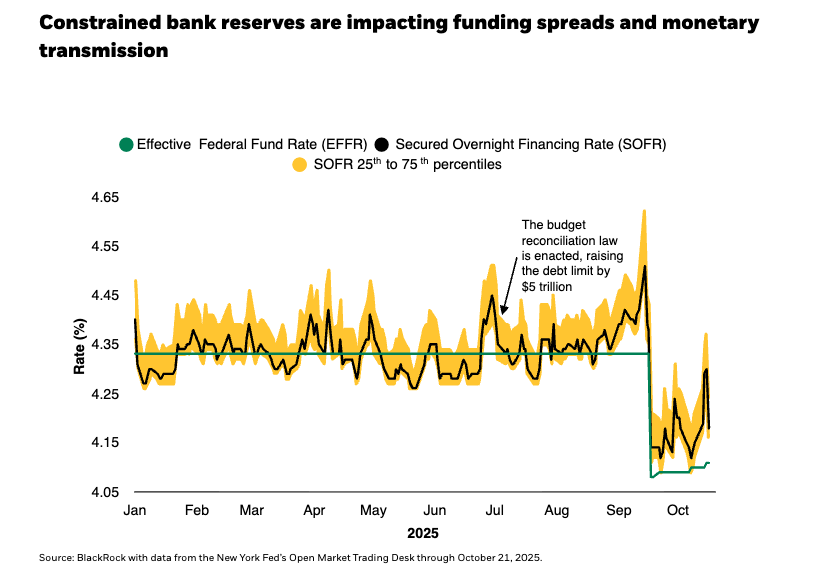

The upward pressure on interest rates stemming from the TGA build and the crowding out of reserves on the balance sheet can be seen in the visual below. Despite the Fed having cut its policy rate by 25bps last month, there has been a more muted decline in interbank and funding market interest rates. We also plot the 25th and 75th percentile spreads of SOFR; the widening of the distribution indicates that the marginal financial institution is now having more challenges securing funding. The knock-on effects of a more constrained balance sheet on term funding markets likely inform the timing of Chairman Powell’s dentist speech to foreshadow to markets an earlier-than-anticipated end to QT to assuage some of this TGA-catalyzed tightening of liquidity across funding markets.

An unsterilized TGA allows the US Treasury to control US banking system liquidity so long as the Federal Reserve choses to maintain a balance sheet policy constrained by a shifting notional size target.6 This policy entanglement is self-imposed insofar as the Fed has failed to evolve its balance sheet principles to the changes in fiscal and regulatory policy. Understanding how balance sheet management might evolve is all the more challenging for market participants given a recent set of speeches by FOMC members that describe a contradictory set of views on the current role and desired future states of the Fed’s balance sheet.7 These operational and communication challenges could transform into a source of rising uncertainty and market risk during the next financial market disruption or economic downturn. To extend Chairman Powell’s dentist analogy, we sincerely hope that the balance sheet isn’t poised to become an abscess for markets and policymakers.

So what does it all mean for portfolios?

The entanglement of fiscal and monetary policies has been an increasingly central feature of post-pandemic markets. The US Treasury-induced tightening of liquidity last month along with signs of relative market complacency led us to reduce directional equity risk in the Tactical Opportunities Fund coming into October. We also reduced directional duration shorts and relative value US Treasury underweights as market pricing and policy signals shifted more neutral on US duration in the global cross-section. Consistent with our investment process to deploy risk when there are dislocations between macro fundamentals and market pricing, we maintain low overall risk in this conflicted investment landscape.

1 The Treasury General Account is the U.S. government’s operating account that is maintained by designated depositaries, primarily Federal Reserve Banks and their branches, to handle daily public money transactions. These transactions include deposits of taxes, customs duties, public debt receipts, proceeds from the sale of securities, and disbursements of U.S. Government payments.

2 In 2025 the Fed has been increasing its ownership share of outstanding US Treasury duration despite ostensibly maintaining a quantitative tightening stance.

3 See Santoro (2012) “The Evolution of Treasury Cash Management during the Financial Crisis,” Federal Reserve Bank of New York, Vol. 18, Number 3 for an in-depth discussion of this change.

4 A recent speech by US Treasury PDO Assistant Secretary Hunter McMaster discussed how the size of the TGA may need to grow further to manage the magnitude of the US T-Bill debt issuance profile given the frequency of settlements of these historically large auctions; “Our cash need is defined as net fiscal outflows plus the gross volume of maturing marketable debt.”

5 Minutes of the Federal Open Market Committee September 16–17, 2025.

6 A recent piece by Vissing-Jorgensen, Annette (2025). "Fluctuations in the Treasury General Account and their effect on the Fed's balance sheet," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, presents a sensible proposal to sterilize TGA swings on the Fed’sbalance sheet by backing them dynamically with changes in T-Bill asset holdings. This would accord with standard banking practices and be a sensible evolution to the Fed’s balance sheet management.

7 Governor Bowman (https://www.federalreserve.gov/newsevents/speech/bowman20250926a.htm), Dallas Fed President Lori Logan (https://www.dallasfed.org/news/speeches/logan/2025/lkl250825), and Governor Waller (https://www.federalreserve.gov/newsevents/speech/waller20250710a.htm) have all presented differing and somewhat conflicting perspectives on navigating balance sheet tradeoffs.

Carefully consider the investment objectives, risks, charges and expenses of the fund carefully before investing. The prospectus and summary prospectus contain this and other information about the fund and are available, along with information on other BlackRock funds, by calling 800-882-0052 or at blackrock.com. The prospectus and, if available, the summary prospectus should be read carefully before investing.

Important risks: The funds are actively managed and its characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to political risks, currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Asset allocation strategies do not assure profit and do not protect against loss.

The opinions expressed are those of Tom Becker and Simon Wan and are subject to change. There is no guarantee that the forecasts made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. Investment involves risk. Information and opinions are derived from proprietary and non-proprietary sources.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change.

Prepared by BlackRock Investments, LLC, member FINRA.

©2025 BlackRock, Inc. or its affiliates. All rights reserved. BLACKROCK and iShares are trademarks of BlackRock or its affiliates. All other trademarks are those of their respective owners.

USRRMH1025U/S-4917048

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© BlackRock

Read more commentaries by BlackRock