Summary

- An investment-grade credit rating materially lowers the cost of debt needed to fund large-scale projects or acquisitions.

- Larger midstream companies tend to have strong credit ratings, causing major midstream indexes to be heavily weighted towards high-quality, investment-grade names.

- The midstream sector offers generous yields, largely from companies with strong credit profiles.

Strong credit ratings remain a key feature for midstream companies, providing significant cost savings on debt. The subsector is largely dominated by investment-grade players, which also offer attractive dividend yields. Learn more below about the importance of an investment-grade rating and why midstream indexes are skewed towards these creditworthy names.

Why Are Credit Ratings Important for Midstream?

Midstream companies commonly tap the debt markets for building new projects or funding acquisitions, and debt is an important part of their capital structure. Historically, midstream companies often used 50-50 debt and equity for funding projects, though that can vary. Instead of issuing equity, midstream companies largely use retained cash flow to fund the equity component today. A strong credit rating remains important for accessing debt markets with a lower interest rate.

A credit rating of BBB or above (A, AA, AAA) is considered investment-grade, while lower ratings are considered high-yield (BB, B, CCC, etc.). As of October 17, the average yield difference between a 10-year BBB rated bond and a 10-year BB rated bond was 120 basis points (5.05% vs. 6.25%). The yield difference is notable and can impact project returns.

Besides a company’s main credit rating, there are also issue-specific ratings for debt tied to a certain asset. A recent example is the Coastal GasLink Pipeline, a joint venture owned by partners TC Energy (TRP CN), KKR, and AIMCo. The partners created a project-level entity, Coastal Gaslink Pipeline LP, which issued $7.15 billion in senior secured notes in mid-2024. This debt is secured by the pipeline itself, so its rating is tied directly to the underlying pipeline’s contracts and cash flows. This structure can also result in a stronger credit rating: While TRP’s corporate rating is BBB+, these secured project bonds received an A- rating.

Leverage Ratios Have Improved

While rating agencies consider a number of factors, investors often look at leverage ratios (measured as net debt/adjusted EBITDA) to gauge financial health. Midstream leverage ratios have come down noticeably over the last several years. A decade ago, it was common for companies to have leverage around 5x (read more), whereas 3–4x is more common today. Some companies have even lower targets.

In 2023, industry heavyweight Enterprise Products Partners (EPD) lowered its long-term leverage target range midpoint from 3.5x to 3.0x. The move, which effectively shifted the goalposts for the sector, was quickly validated when S&P upgraded EPD to an A- rating, making it the only midstream company to hold that rating. Other companies, like Plains All American (PAA/PAGP), followed suit by lowering their own targets.

Larger Midstream Players Tend to Have Strong Credit Ratings

Looking at credit ratings by index, there is a strong bias towards investment-grade names. For the Alerian Midstream Energy Index (AMNA), the broadest midstream benchmark, 20 out of 28 constituents have an investment-grade rating. AMNA constituents with high-yield debt ratings tend to be smaller, with a median market capitalization of $2.1 billion compared to the median market cap for investment-grade constituents of $28.7 billion. There is a clear correlation between the size of a company, as represented by market capitalization, and the credit rating. This is because larger companies generally have more stable cash flows, more diversified businesses, and stronger access to capital markets.

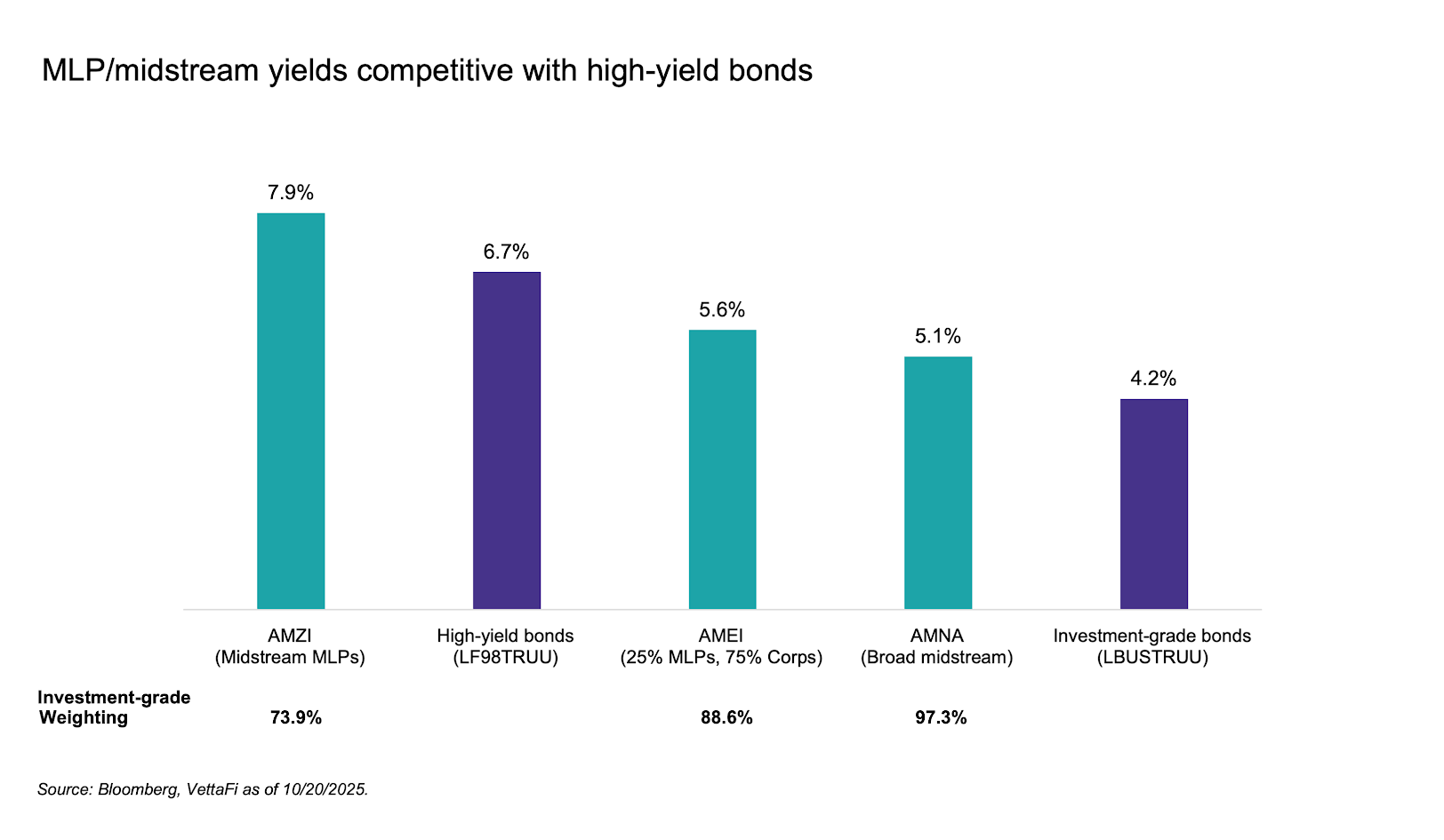

By weighting, investment-grade companies make up the vast majority of AMNA at 97.3% as of October 20. Since constituents in the index are weighted by float-adjusted market capitalization, the weighting naturally skews towards the more creditworthy companies. Similarly, investment-grade ratings make up 88.6% of the Alerian Midstream Energy Select Index (AMEI) and 73.9% of the Alerian MLP Infrastructure Index (AMZI) by weighting.

Midstream credit ratings have generally seen positive trends. C-Corp DT Midstream (DTM) achieved an investment-grade credit rating from S&P in July. For DTM, this was a long-term strategic goal established upon its spin-off in 2021. Management expects the upgrade to reduce interest expense, improve liquidity, and broaden its access to new investors and indexes.

Hess Midstream (HESM) also achieved an investment-grade rating from S&P following the completion of Chevron (CVX)’s acquisition of Hess. S&P upgraded Williams (WMB) earlier this year from BBB to BBB+ based on strong credit metrics. In its earnings results last week, Kinder Morgan highlighted an upgrade from BBB to BBB+ by Fitch in August, noting positive outlook on its ratings Moody’s and S&P.

Midstream Offers Attractive Yields From Quality Companies

The credit quality of midstream/MLP indexes can help provide important context to generous dividend yields, alongside dividend track records, free cash flow generation, and guidance for growing payouts. Higher yields typically imply lower quality and greater risk. Investors are sometimes positively surprised by the strength of midstream credit ratings considering their dividend yields. Importantly, midstream/MLP dividends are expected to grow as these companies generate significant free cash flow.

As shown below, MLPs currently offer a higher yield than high-yield bonds. This income also comes from companies with much higher credit quality than those in the high-yield bond category. It’s important to clarify, however, that midstream equities are not a fixed-income substitute. While the yields are compared to bonds for context, dividend and distribution payments are not guaranteed coupon payments and carry a different risk profile associated with equity ownership.

For additional context, these yields compare with five-year averages of 7.8% for AMZI, 6.1% for AMEI, and 5.9% for AMNA. In a falling rate environment, the income provided by midstream MLPs and C-Corps is more resilient as it doesn’t fluctuate with interest rates (read more).

Bottom Line

A strong, investment-grade rating remains desirable for midstream companies. While the sector is less leveraged than in the past, these ratings ensure access to capital for large projects or acquisitions at a lower cost of debt, which directly improves returns. The industry trend is toward continued credit improvement, as seen with recent upgrades for DTM and HESM. Credit ratings also provide additional context to the attractive yields from midstream/MLPs.

For an informative 30-minute discussion with Energy Transfer (ET), don’t miss our webcast on Wednesday, November 12, at 12:30 p.m. ET. Follow the link here to register.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research:

Breaking Down MLP Distribution Outlooks With AMZI

Falling Interest Rates Impacting Yield? Midstream/MLPs Can Help

Midstream/MLP Free Cash Flow Yields Still Strong

2Q25 MLP/Midstream Dividend Recap: MLPs Deliver Growth

Midstream/MLPs 2024 Leverage Ratios on Target

Examining Midstream/MLP Credit Ratings and Yields

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, ENFR, and ALEFX, for which it receives an index licensing fee. However, AMLP, MLPB, ENFR, and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, ENFR, and ALEFX.

For more news, information, and analysis, visit the Energy Infrastructure Content Hub.

Originally published on ETF Trends

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi