Friends Not Foes

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOften framed as rivals, private and liquid credit should instead be viewed as powerful complements for both issuers and investors. We believe these two markets are settling into a symbiotic coexistence, as the distinctions blur between the likes of direct lending and broadly syndicated loans.

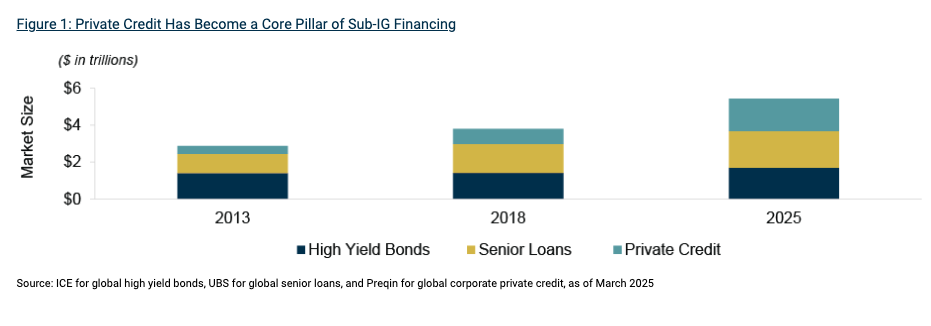

The rise of private credit has been one of the defining post-Global Financial Crisis developments. Now a mainstream asset class, corporate private debt constitutes over $1.7 trillion in assets and has become a fixture in institutional portfolios.1 This rapid growth has often been characterized as being at the expense of the more established liquid credit markets. However, the ability for borrowers to flexibly access both liquid and private credit markets should be viewed positively by investors exposed to corporate credit risk. These distinct but interlinked markets together broaden the range of available credit solutions, serving to support the financial health of issuers. (See Figure 1.)

Investors can also benefit from the nuanced propositions of these two markets, which may be increasingly converging but continue to offer differing levels of yield, credit risk, liquidity, and volatility. For sophisticated investors, the decision shouldn’t be between private or liquid credit, but instead around the most effective way to gain exposure to these complementary markets.

The Rise of Private Credit

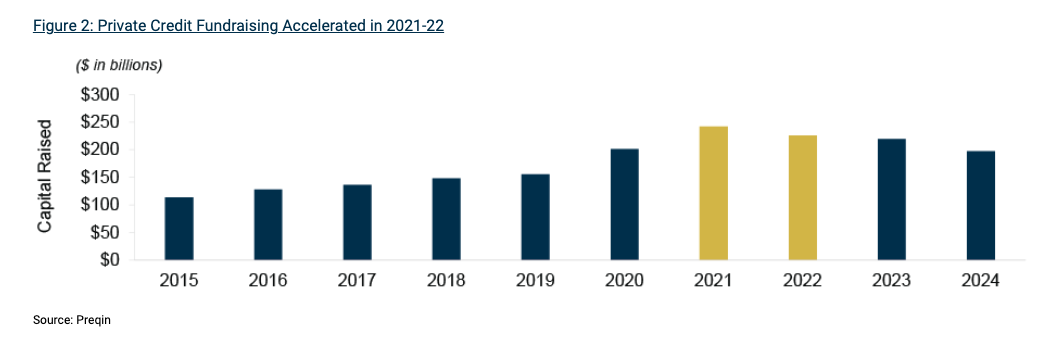

The story is now a familiar one. Banks, crippled by stringent capital regulations in the wake of the 2008 meltdown, retrenched from corporate lending. This paved the way for alternative lenders to fill the funding gap. The rise of private debt was then solidified by the Covid-19 pandemic and subsequent macroeconomic challenges. With the traditional syndicated debt markets periodically unavailable, a wide range of borrowers sought credit offering both rapid execution and enhanced flexibility. Combined with its spread premium over liquid credit during a time of low base rates, it’s no coincidence that private debt fundraising spiked during this period. (See Figure 2.)

It's worth noting that the growth of private credit has been supported by establishing a strong track record of solid performance and minimal credit losses. Like high yield bonds before it, private credit, in the form of direct lending, has transitioned from obscure to mainstream.

A More Versatile Financing Ecosystem

Large borrowers benefit from having two sets of lenders that can step in across different market conditions. The interplay of liquid and private credit has been clearly illustrated in just the last few years.

With liquid credit markets subdued in 2022, private lenders were able to provide much-needed financing. The mark-to-market volatility that spooked liquid markets wasn’t a factor for private credit, which benefits from asset prices less exposed to broader market sentiment. Importantly, private lenders can move unilaterally (or in smaller lender groups), meaning they inherently circumvent banks – which at the time were saddled with hung loans and reticent to underwrite new deals.

While this removed potential deal flow for public lenders, the injection of private debt stabilized many public borrowers at a time when liquid markets couldn’t help. This was especially true for lower-rated borrowers, for which public markets had scant appetite. These migrating issuers paid a premium to refinance in the private market but received a crucial lifeline in the form of flexible credit.

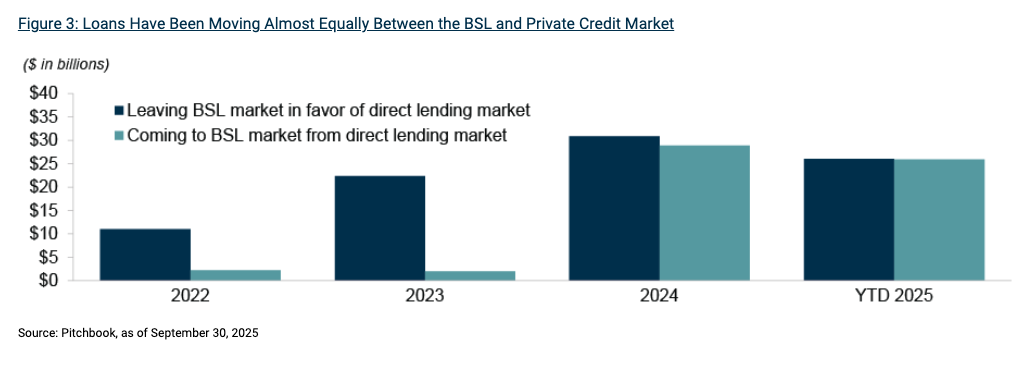

As liquid credit markets found greater stability entering 2024, with a firmer understanding of the trajectory of interest rates and more confidence in a soft landing, public financings boomed, albeit primarily driven by refinancings. With both the liquid and private credit markets now truly open again and the spread differential between the two compressing, we’ve reached parity in refinancing activity between the direct lending and broadly syndicated loan (BSL) market: roughly $25 billion of loans have gone in each direction so far this year.2 (See Figure 3.)

A Complementary Investment Proposition

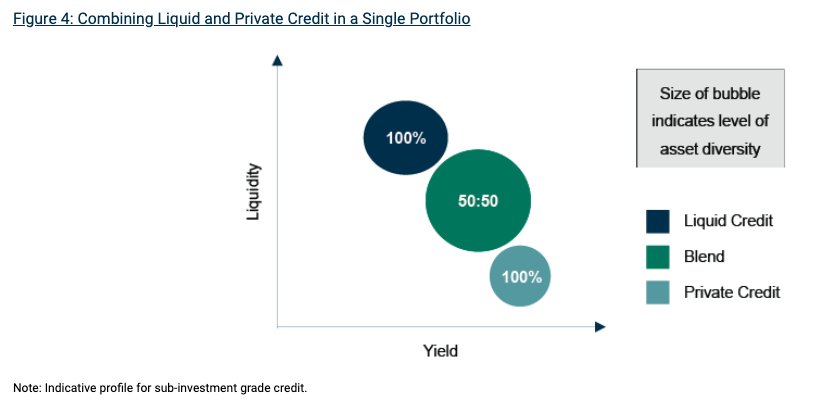

When combined, we believe the liquid and private credit markets provide an excellent solution due to the range of complementary nuances that allow investors to solve for an optimal blend of yield, liquidity, and volatility. (See Figure 4.)

First, liquid credit has a clear tradability advantage, generally benefiting from regular two-way pricing. In comparison, private loans, which lack regular market pricing, have an unclear liquidity profile: secondary markets exist but aren’t particularly developed and often require sellers to accept a chunky discount. For most private debt investors in closed-end funds, liquidity is limited to distributions and return of capital, something that limited partners can’t control.

Combining liquid and private credit in a single portfolio can present an efficient solution. The liquid portion of the portfolio can be used to promptly meet investor liquidity requirements and allow rapid deployment of new capital. The ability to invest in liquid credit can also be valuable during periods of dislocation, as managers can access discounted bonds and loans, creating pull-to-par opportunities that may enhance total returns. Meanwhile, the private portion of the portfolio dampens volatility, being marked on fundamentals rather than prevailing market psychology, and should offer an attractive yield premium, particularly if lending to businesses smaller or more levered than those in the broadly syndicated markets.

Particularly notable is the diversification benefit of blending private and liquid credit. Direct lending funds are much more concentrated than liquid credit funds, which may contain several hundred issuers. Blending the two means investors can receive exposure to a broader mixture of company size, sector, and geography.

Beyond The Core

The obvious entanglement is between direct lending and broadly syndicated loans, both of which primarily provide private equity sponsors with senior floating rate debt. But it’s important to note there’s much more to the liquid and private debt markets. We believe particularly accretive diversifiers may include:

-

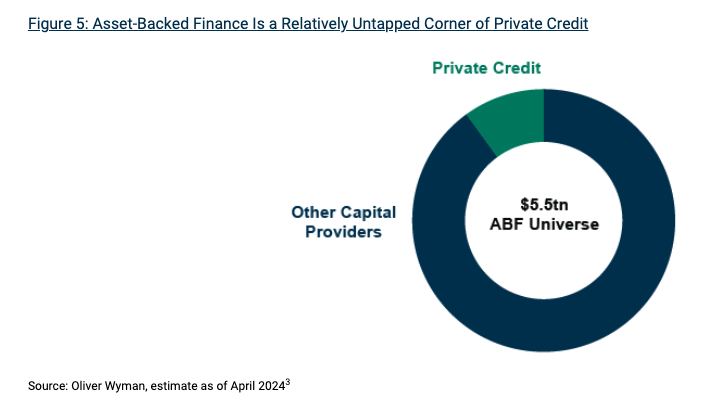

Asset-backed finance (ABF), which offers a different risk/return profile to corporate lending, being backed by pools of contractual assets and providing lenders with continuous principal repayment. ABF represents a massive addressable universe, with private lender participation still limited. (See Figure 5.)

-

Sectoral private credit niches, which involve highly tailored origination and underwriting methods, often requiring specialized knowledge, as with life sciences or infrastructure lending.

-

CLOs, which benefit from powerful structural protections and a spread premium over similarly rated corporate bonds. CLO tranches aren’t immune to mark-to-market volatility but historically have a very low impairment rate.

-

Real estate debt, in the form of direct loans or securitizations (i.e., CMBS, RMBS), which offers a different underlying risk to corporate credit and may be less exposed to potential macroeconomic headwinds.

What Next?

Private and liquid credit are set to continue this symbiotic coexistence. Financing requirements will remain high as large-cap M&A activity gradually returns and borrowers seek to refinance a looming wall of debt. We anticipate a sustained rise in capex requirements across Western economies, including data center financing, increased defense expenditure, and digital infrastructure build-out. We expect to see both liquid and private credit markets playing an important role in meeting these financing needs, including through potential collaboration on larger deals.

Investors can take advantage of this dynamic by blending private and liquid credit investments to optimize their portfolios for acceptable levels of liquidity and volatility. Beyond now-mainstream asset classes like direct lending and high yield bonds, this’ll likely include less traditional areas such as asset-backed finance and liquid structured credit. We believe the new diversification lever isn’t a static 40% investment grade corporate bond allocation but instead a dynamic portfolio of private and liquid credit.

Of course, the important caveat is the latter option requires a completely different level of due diligence. The likes of high yield bonds and senior loans offer greater reward than investment grade bonds as they also present more risk – and that must be managed. Extending to private credit, which may present even more spread in exchange for potentially lower credit quality and less liquidity, deep underwriting is as essential as ever. Get that right and investors may be able to access a diversified, income-generating portfolio without equities’ reliance on economic growth.

Credit Markets: Key Trends, Risks, and Opportunities to Monitor in 4Q2025

(1) Converts lead the way!

Convertible bonds have experienced strong growth in both performance and issuance volume in 2025 as this under-the-radar asset class has benefitted from several tailwinds.

September set a monthly record for convertible bond issuance, with nearly $30bn of new supply.4 This was supported by a notable rise in issuance in Asia and Europe, which contributed around 45% of the supply.5 Issuance for the asset class now exceeds $125bn so far this year, as sustained stock market strength and tight credit spreads have supported a surge in deals.6

Performance has been strong thus far in 2025, particularly for balanced convertibles, which benefit from participation in equity upside. AI has been a highly accretive theme for the convertibles market, with Bank of America research indicating AI-linked issuers have returned triple that of the broader market!7

(2) European credit markets are active

Europe continues to be a bright spot for sub-investment grade credit issuance.

-

The third quarter saw record European CLO activity, as robust demand for liabilities helped AAA-rated spreads compress back below 130 basis points for tier-one managers.8

-

Senior loans also finished September at record issuance levels for the year-to-date period. This was supported by a wave of repricings, but “new money” issuance has still edged higher from the lows of 2023.

-

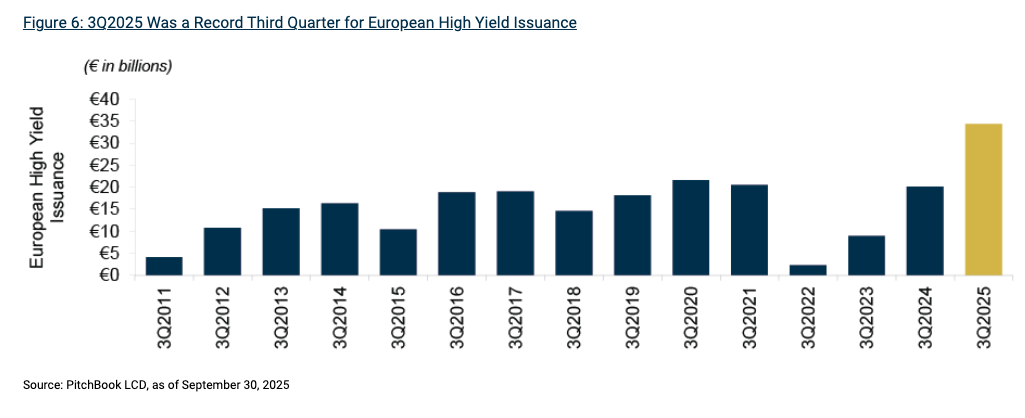

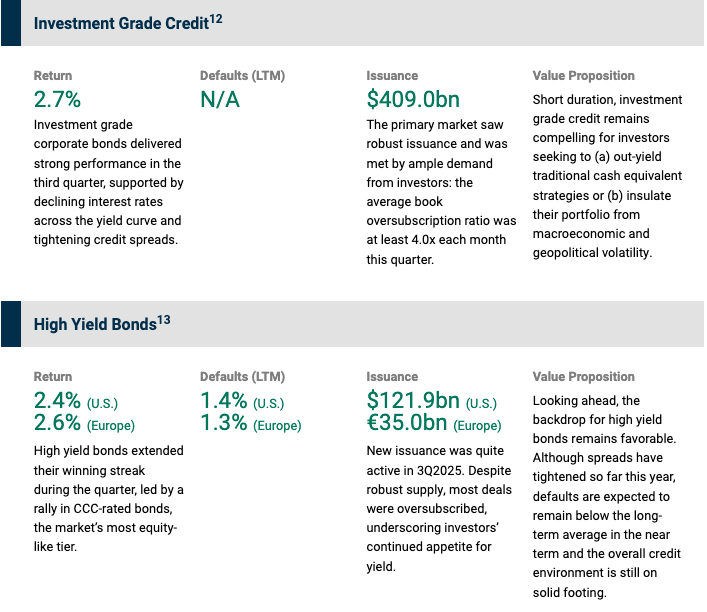

High yield bonds clocked a record third quarter, following a bumper September. (See Figure 6.) Similar to loans, this was dominated by refinancings, which made up nearly 70% of total volume.9

-

Direct lending activity has been strong, with over €30bn of volume so far this year, exceeding the level for the same period in 2024.10

We expect European credit to remain active as (a) private equity firms seek to increase exposure to the region and (b) several themes – not least increased defense and infrastructure spend – create sustained capex needs. European credit issuance has been met with ample demand from lenders, including those seeking to diversify U.S.-centric credit portfolios and access the compelling hedged yields offered by EUR-denominated bonds and loans.

(3) The credit market remains bifurcated by quality

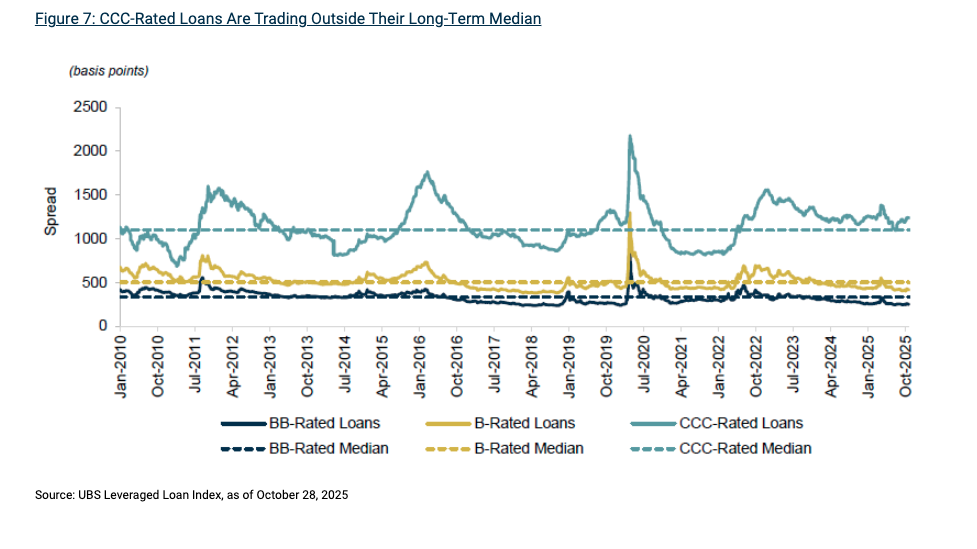

Index averages remain a somewhat misleading proxy for the state of credit markets, as quality names remain well bid but unloved ones rapidly fall through the cracks. Recent well-publicized credit problems have exacerbated this dynamic, as has a CLO buyer base with limited appetite for CCC-rated loans. Accordingly, while B- and BB-rated loans currently trade within their long-term average spread, CCC-rated loans are trading outside their historical average, with an average spread in excess of 1,200 bps.11 (See Figure 7.) When dispersion is this dramatic, fundamental, bottom-up credit selection is especially critical.

We discussed this bifurcation in depth on a recent podcast.

Strategy Focus

About Oaktree’s Credit Platform

Oaktree Capital Management is a leading global alternative investment management firm with expertise in credit strategies. Our credit platform has $156 billion in AUM and encompasses a broad array of strategy groups that invest in public and private credit instruments across the liquidity spectrum.19 All Oaktree investment activities operate according to a unifying philosophy that emphasizes key principles including the primacy of risk-control and benefits of specialization.

Armen Panossian, Co-Chief Executive Officer and Head of Performing Credit

Danielle Poli, CAIA, Managing Director and Assistant Portfolio Manager

Endnotes

1 Preqin, as of March 2025.

2 PitchBok, as of September 2025.

3 Oliver Wyman, Private Credit’s Next Act, April 2024. The $5.5 trillion figure represents the U.S. asset-backed finance market, excluding real estate.

4 BofA, Global Convertibles Chartbook, as of October 1, 2025.

5 Ibid.

6 Ibid.

7 BofA, Global Convertibles, as of October 20, 2025.

8 PitchBook.

9 Ibid.

10 PitchBook, as of September 30, 2025.

11 UBS Leveraged Loan Index, as of October 28, 2025.

12 ICE U.S. Corporate Index for all return data; Bank of America for all issuance data (reflects U.S. issuance).

13 ICE BofA US High Yield Constrained Index for all U.S. High Yield Bonds return data; ICE BofA Global Non-Financial High Yield European Issuer Excluding Russia Index for all European High Yield Bonds data; JP Morgan for all U.S. default rates; UBS for all European default rates (including distressed exchanges); PitchBook LCD for all U.S. and European issuance data (including refinancings).

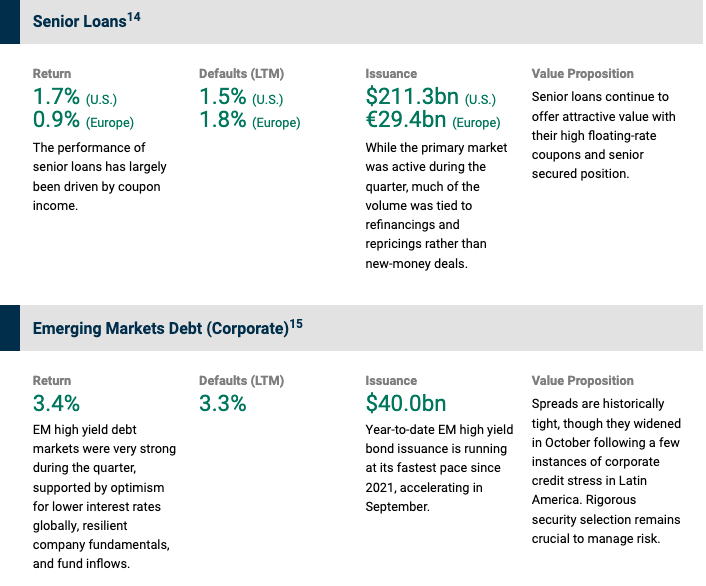

14 S&P UBS Leveraged Loan Index for all U.S. Senior Loans return data; UBS Western Europe Leveraged Loan Index for all European Senior Loans return data; JP Morgan for all U.S. default rates; UBS for all European default rates (excluding distressed exchanges); PitchBook LCD for all U.S. and European issuance data (including refinancings).

15 JP Morgan Corporate Broad CEMBI Diversified High Yield Index for all return data; JP Morgan for default rates (including distressed exchanges) and issuance (including refinancing) data.

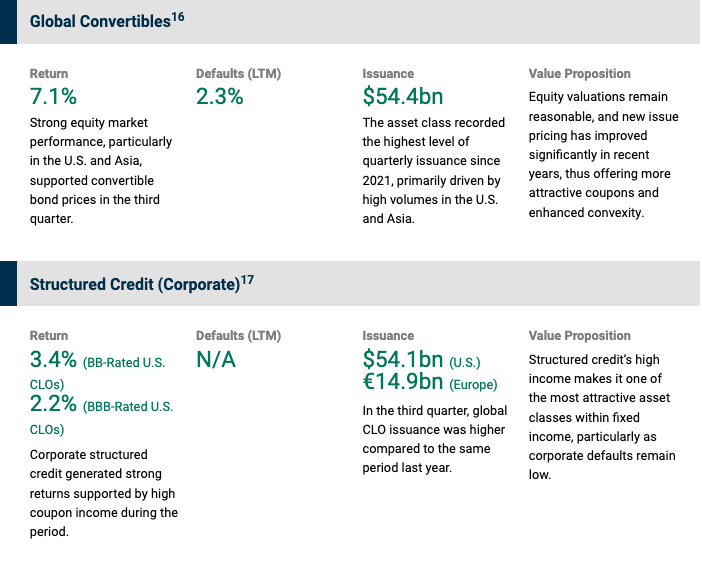

16 Refinitiv Global Focus Convertible Index for all return data; Bank of America for default rates and issuance data.

17 JP Morgan CLOIE BB Index and JP Morgan CLOIE BBB Index for all return data; JP Morgan Weekly CLO Issuance for all issuance data.

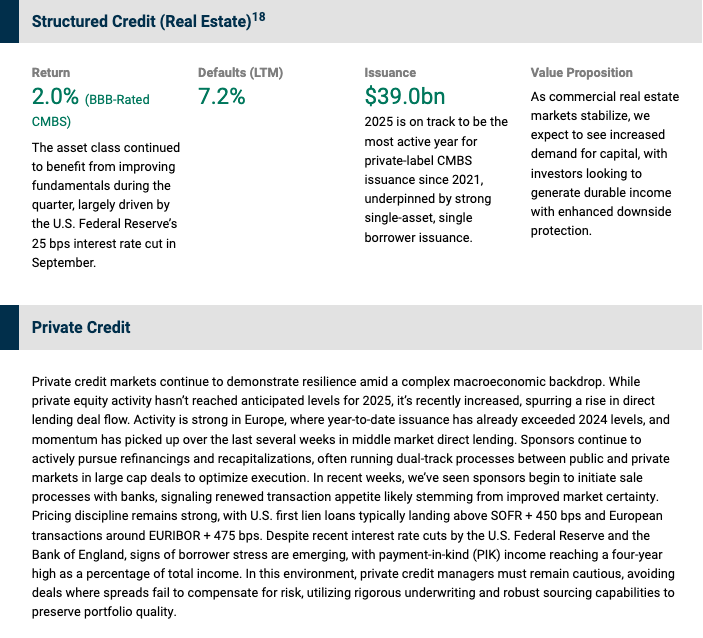

18 Bloomberg US CMBS 2.0 Baa Total Return Unhedged Index for all return data; Trepp for default rates (%, 30+ day delinquency, and REO); JP Morgan for all issuance data.

19 The AUM figure is as of September 30, 2025 and excludes Oaktree’s proportionate amount of DoubleLine Capital AUM resulting from its 20% minority interest therein. The total number of professionals includes the portfolio managers and research analysts across Oaktree’s performing credit strategies.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Notes and Disclaimers

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including broker dealer, investment adviser or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

This document, including the information contained herein may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated or disclosed, in whole or in part, to any other person in any way without the prior written consent of Oaktree Capital Management, L.P. (together with its affiliates, “Oaktree”). By accepting this document, you agree that you will comply with these restrictions and acknowledge that your compliance is a material inducement to Oaktree providing this document to you.

This document contains information and views as of the date indicated and such information and views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree believes that such information is accurate and that the sources from which it has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based. Moreover, independent third-party sources cited in these materials are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the use of such information in these materials.

© 2025 Oaktree Capital Management, L.P.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All