Wall Street excels at creating catch phrases. The latest one is the “debasement trade.” JP Morgan analysts coined the term earlier this year. Thanks to macroeconomic and geopolitical factors such as lower interest rates, rising fiscal deficits, trade policies, and global geopolitical tensions, concern is rising about the debasement or devaluation of fiat currency.

The debasement trade involves moving money out of government-issued securities like Treasuries, which have lost their appeal due to several factors. Those reasons include excessive government spending and money printing, with investors turning to hard assets with limited supply, like gold, silver, critical materials, bitcoin and cryptocurrencies to serve as a hedge against currency devaluation.

Proponents of the debasement trade thesis highlight the flow of capital into hard assets to “de-dollarize” or “de-risk” their portfolios. As seen in the chart below, the U.S. dollar index has experienced a sharp decline this year relative to gold.

The performance of the U.S. dollar against the euro and the currencies of Japan, the U.K., Canada, Sweden, and Switzerland also fell more than 10% in the first half of the year, its biggest drop since 1973.

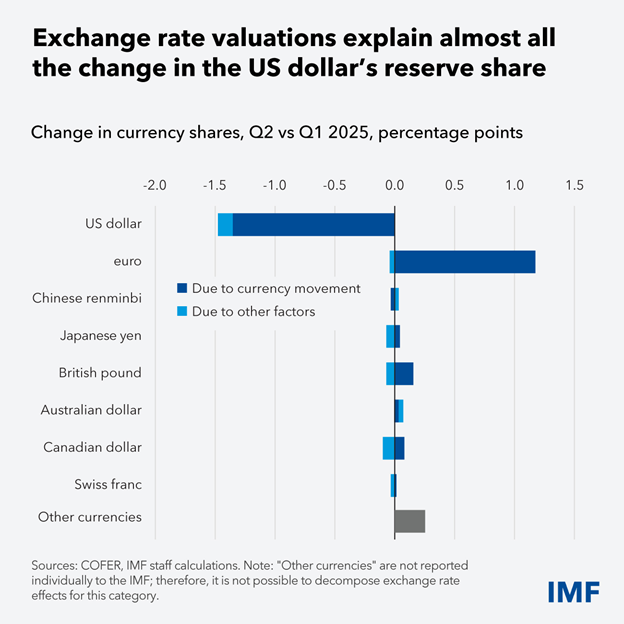

There is rising concern that the dollar’s dominance as a reserve currency is at risk, given that more foreign governments like China are reducing their dependence on the U.S. dollar. However, according to the IMF, currency movements accounted for 92% of the decline in the dollar’s share in the second quarter. That is similar to the decline in other currencies, such as the euro, which ranks just behind the U.S. dollar as a reserve currency.

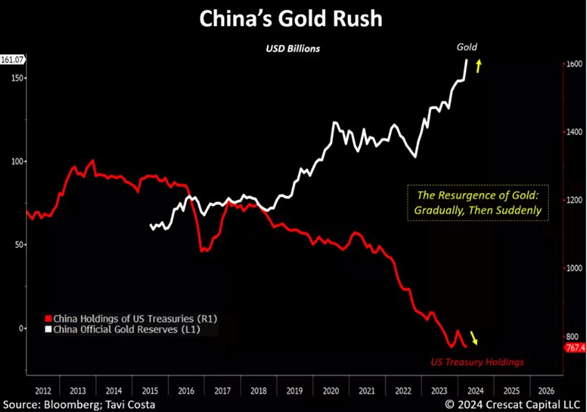

China has been reducing its U.S. Treasury exposure over the last decade, falling 42% from its peak level of $1.3 trillion. While there is no evidence in support of mass dumping or plans to weaponize currency, China’s gold share reserves are at record levels and could be even higher than what is being disclosed to the IMF. This raises the possibility of the country adopting a gold-backed yuan, while its digital currency efforts mean that a digitized version could follow.

ETFs to Play the Debasement Trade

As mentioned, hard assets with finite supply have been the main beneficiary of the debasement trade. These include precious metals, cryptocurrencies, and critical materials.

Precious Metals

When it comes to precious metals, some ETFs target the physical commodity and others focus on the miners themselves. Typically, in times of rising prices, the miners outperform, given their ability to operationally leverage prices resulting in margin expansion. For those that want leverage on leverage, at the top of the performance leaderboard is the MicroSectors Gold Miners 3X Levered ETN (GDXU), which has delivered a 450% return YTD. For unleveraged exposure, investors can consider the VanEck Gold Miners ETF (GDX) and its smaller-cap, junior miner partner, the VanEck Junior Gold Miners ETF (GDXJ).

Despite all the focus on gold, silver miners have also delivered strong YTD performance this year. For large-cap silver exposure there is the iShares MSCI Global Silver Miners ETF (SLVP) and for small-cap silver miners there is the Amplify Junior Silver Miners ETF (SILJ). Both are up in excess of 125% for the year.

Gold and silver are not the only precious metals to deliver outsized performance in 2025. Physical platinum ETFs, the Aberdeen Physical Platinum Shares (PPLT) and the GraniteShares Platinum Trust (PLTM), are each up around 75% YTD. Like gold and silver, platinum can be used for jewelry, but it also has many diverse applications for industrial use. Those applications include catalytic converters and spark plugs for autos, aerospace jet and rocket engines, and clean fuel cell technology.

Cryptocurrencies

In addition to bitcoin and Ethereum ETFs, there are a host of new spot altcoin launches that hit the market in October, with issuers taking advantage of the government shutdown to go effective without formal SEC approvals. The U.S. Securities and Exchange Commission shutdown guidance allows some filings to go effective automatically after 20 days. Crypto ETF issuers appear to have capitalized upon that loophole.

XRP (XRP): Just prior to the shutdown, XRP’s first spot ETF, the Rex-Osprey XRP ETF (XRPR) made its debut.

Solana (SOL): Rex-Osprey also launched the first Solana ETF, with the Rex-Osprey Solana Staking ETF (SSK) back in July. In October, amidst the ongoing regulatory hiatus, Bitwise rolled out its version, the Bitwise Solana Staking ETF (BSOL), on October 28. BSOL has full staking exposure to Solana, the sixth-largest token, which offers a potential yield of roughly 7%. Grayscale followed suit with the Grayscale Solana Trust ETF (GSOL), which also provides staking exposure.

Litecoin (LTC): Canary Capital launched its spot Canary Litecoin ETF (LTCC) on the Nasdaq on October 28.

Hedera (HBAR): Canary Capital also launched the spot Canary Hedera ETF (HBR) on the Nasdaq on October 28.

Spot ETFs tied to bitcoin and ether have seen success and a more favorable regulatory environment. Therefore, it is no surprise that issuers are coming out with more spot crypto ETFs. The question is: Will all of them spur much in the way of demand?

So far with Solana, SSK has gathered $385 million in assets since its debut. BSOL has over $300 million. GSOL has already raised $100 million in assets. This bodes well for the roughly two dozen other Solana filings since 2024.

Meanwhile, XRPR has over $100 million in assets, but LTCC and HBAR have yet to spark much investor interest. To quote my TMX VettaFi colleague Roxanna Islam, “The crypto ETF market is already oversaturated, which could hinder some of the smaller or more obscure crypto funds from gaining significant inflows.”

Critical Metals

Copper and other critical metals have also rallied on the debasement trade. ETF beneficiaries include the Sprott Critical Materials ETF (SETM), up 80% for the year, the VanEck Rare Earth and Strategic Metals ETF (REMX), up 78% YTD and the Global X Disruptive Materials ETF (DMAT), up 76%.

Besides the debasement trade, critical material stocks have rallied. That could be given the U.S. government’s support for domestic production and investment to counter China’s dominance in the refining and mining of strategic metals. China decisively leads the world in the production of many critical minerals. The top five critical minerals for which the country leads in production include gallium. China claims a nearly 99% market share of that mineral. Meanwhile, China also produces 95% of the world’s magnesium and almost 83% of its tungsten. Additionally, China produces a little over 69% of rare earths metals. These materials are vital for many critical applications such as clean energy, aerospace and defense, and electronics. China has also retaliated with an expanding list of critical material and rare earths export bans in response to tariffs.

Copper has also racked up strong returns as a strategic material. Copper mining ETFS such as the Global X Copper Miners ETF (COPX) have gained 65% YTD, and the Sprott Junior Copper Miners ETF(COPJ) is up 94% for the year.

When it comes to the debasement trade, all that glitters is not gold and Bitcoin.

VettaFi LLC (“VettaFi”) is the index provider for GDXU, for which it receives an index licensing fee. However, GDXU is not issued, sponsored, endorsed or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of GDXU.

Originally published on ETF Trends

For more news, information, and strategy, visit the Disruptive Technology Content Hub.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi