2025 has not been just a story of U.S. resilience. The Asia-Pacific (APAC) region has weathered storms and stayed firmly on course. The worst trade outcomes have been avoided, with tariffs settling at lower rates than threatened at the start of the year by the U.S. administration. Export momentum has held up better than expected, buoyed by strong demand for electronics and robust intra-regional trade. Inflation has settled into a steadier rhythm across much of the region.

But beneath the hood lies a complex interplay of shifting trade gears and policy recalibration. The old roadmaps of globalization no longer apply. To keep the growth engine running smoothly, the region will not only have to endure but evolve. Asia Pacific’s growth prospects will be defined by the ability of regional economies to rewire trade relationships and fine-tune policy to meet demands of new economic realities.

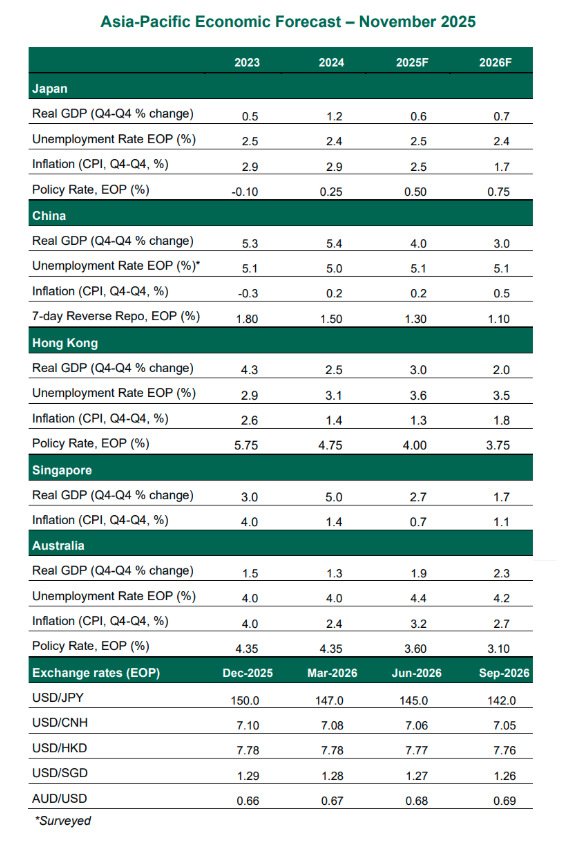

Following are our views on how major APAC markets are poised to perform.

Japan

- Growth in the second quarter was revised upward, reflecting healthier consumption and inventory investment; we have upgraded our growth outlook for this year accordingly. However, this has not changed the outlook of a slow environment for exports, leaving a challenging landscape for the business sector. Japan has been a frontrunner in its efforts to negotiate a more sophisticated deal with the United States, pledging $550 billion of future investment. However, even the most generous concessions are unlikely to restore its former terms of trade.

- Support for growth will need to come from Japanese consumers, but they will be challenged by persistent inflation and a weakened currency. Real wage growth has turned negative, eroding purchasing power. The Bank of Japan held the policy rate steady at 0.5% at the October meeting, amid uncertainty over the outlook for domestic wage gains and its largest export market, the United States. We continue to expect the next rate hike in early 2026, though risks are tilted toward an earlier move as policymakers weigh the trade-off between rising borrowing costs and the risk of further currency depreciation.

China

- Presidents Trump and Xi agreed to extend their tariff truce by one year during their talks in South Korea. The U.S agreed to a 10 percentage point reduction in tariffs on Chinese goods. In return, China agreed to suspend its recently announced rare earth export control measures and resume imports of U.S. soybeans. Both sides also committed to postponing the imposition of higher docking fees on each other’s shipping fleets. While this helped avoid another flare-up in tensions, a comprehensive deal remains elusive, with major issues still unresolved.

- China’s economy is holding steady, with gross domestic product (GDP) growing 4.8% year-on-year in the third quarter; the government’s 5% annual target is within reach. But momentum is weakening. Domestic demand is soft, weighed down by weak consumer sentiment, persistent deflation and a deepening property market slump. Government efforts to stimulate activity and stabilize the real estate sector have so far yielded limited results. The People’s Bank of China has maintained a steady policy stance, but fiscal support is waning, and the timing of any new stimulus is uncertain.

Singapore

- Real GDP growth slowed down from 4.5% year over year in the second quarter to 2.9% in the three months to September. However, the moderation was smaller than expected, as manufacturing activity helped partially offset the pullback in services and construction. Re-exports have benefitted from trade front-loading and are expected to continue gaining from one of the lowest new effective tariff rates in the United States. While growth is expected to hold steady in the near-term, America’s increasing scrutiny of transshipment activities could pose a significant risk to Singapore.

- In its October monetary policy meeting statement, the Monetary Authority of Singapore (MAS) decided to keep its policy band for the Singapore dollar unchanged. Resilient growth and the recent uptick in core inflation, if sustained, have raised the risk of the MAS maintaining its current policy stance for an extended period.