Key takeaways:

- Valuations are towards the richer end of long-term ranges across many asset classes but Europe’s levered credit markets tell a different story

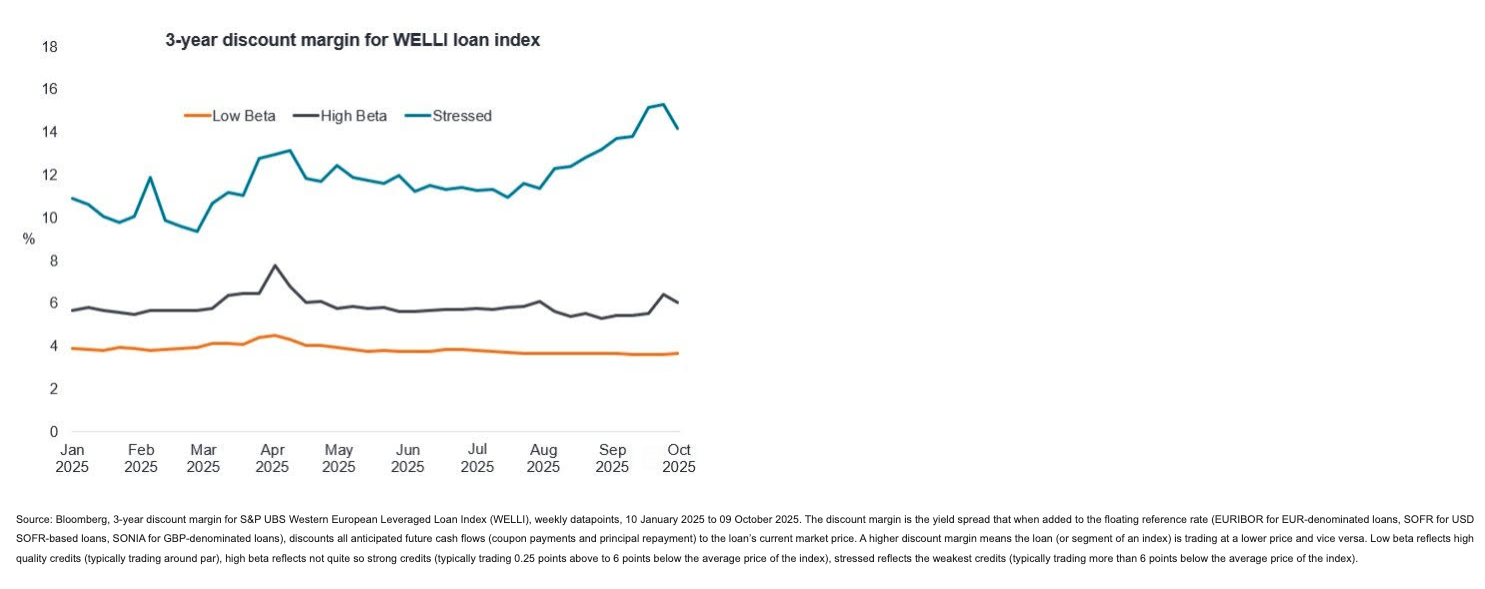

- Significant dispersion underlies the headline figures in the loan market, as reflected in the pricing of the distressed segment, which has been weakening for several months.

- Deep research and a disciplined portfolio construction process can help active managers identify risks early and avoid potential downside.

“While the overall economy is in decent shape and many financial benchmarks are near their highs, it can be easy to overlook pockets of fragility. Deep research and a disciplined portfolio construction process can help active managers identify risks early and avoid potential downside.”

– John Lloyd, Fixed Income Portfolio Manager.

While valuations in most fixed income assets are toward the richer end of long-term ranges, Europe’s levered credit markets tell a different story with the WELLI (Western Europe Leveraged Loan Index) trading closer to its long-term average.

Significant dispersion underlies the headline figures and we divide this market into three segments – low beta, high beta, and stressed – demonstrate. Trading in the low and high beta segments has been orderly. Persistent demand and repricing activity have narrowed the margin of the low beta segment this year. The high beta segment trades with more volatility but has remained rangebound outside of a brief Liberation Day spike. The stressed segment has materially underperformed its counterparts. This segment has grown as a proportion of the overall index as vulnerable credits fall into it. Weak trading, often accompanied by challenged liquidity with few natural buyers, has exacerbated price declines which show up in higher discount margins. The larger and wider stressed segment is pushing out index-level spreads.