Though we are getting limited amounts of economic data during the federal government shutdown, the official and private sector data we are receiving generally paints a positive picture for U.S. economic activity. For example, the official Consumer Price Index (CPI) numbers released in late October showed that inflation is persistent, but the monthly update came in a little lower than expected

Looking at the available jobs data, we are seeing greater stability than the headlines might suggest. State level unemployment claims continue to reflect a limited number of layoffs, some headline-generating reports of large tech companies reducing headcount notwithstanding.

Similarly, the latest private sector jobs report from ADP showed October jobs gains above expectations. Despite some large firms reducing headcount, smaller firms continue hiring. Furthermore, the economically-weighted Purchasing Manager Index measure continues to reflect overall expansion as October growth in the services sector outweighed manufacturing sector weakness.

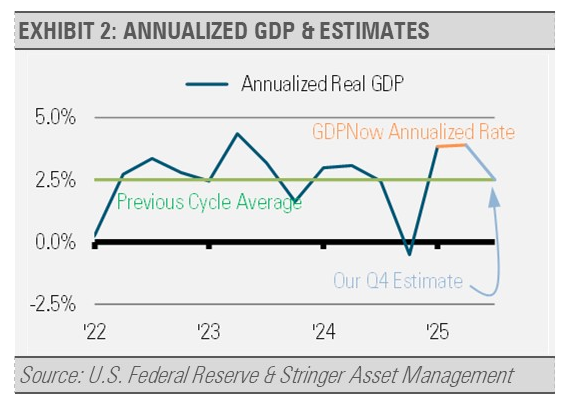

Putting this all together, it looks like the U.S. economy will grow at roughly 2.5% for calendar year 2025, despite a down quarter at the start of the year. Notably, our expectation for 2.5% GDP growth matches the previous business cycle average of 2.5% U.S. GDP growth.

Despite all the headlines around a soft start to the year for GDP growth, such as uncertainty around tariffs and geopolitical risks, the U.S. economy looks like it will continue to power ahead.

Persistent GDP growth should lead to overall higher corporate and household earnings, though there will be some weakness in lower income households. This aggregate growth can support the equity market to new highs.

INVESTMENT IMPLICATIONS

In this environment, we continue to favor domestic equities with a tilt towards quality growth. Our preferred sectors remain information technology, industrials, and financials. With attractive yields as the U.S. Federal Reserve reduces short-term interest rates, the intermediate part of the yield curve offers return potential with a buffer from equity market volatility. We are emphasizing asset-backed securities over U.S. Treasuries for their additional high-quality yield as we have leaned into the intermediate part of the yield curve.

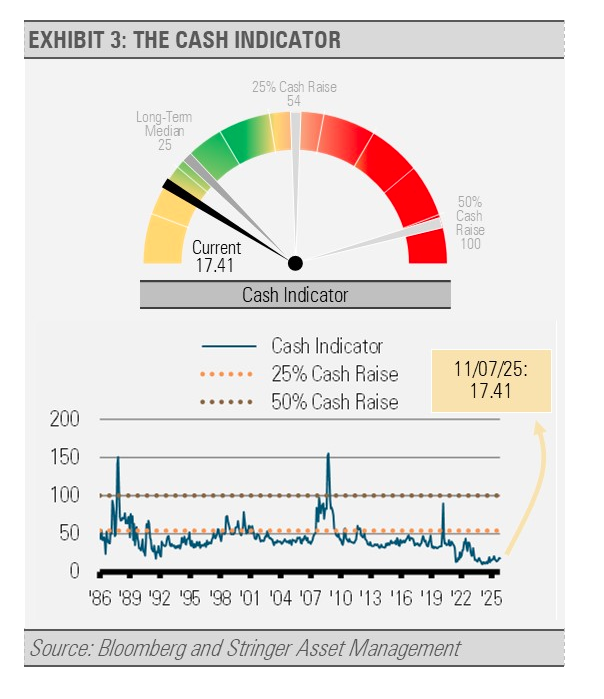

THE CASH INDICATOR

Though volatility has picked up lately, the Cash Indicator (CI) continues to reflect a healthy amount of risk being priced in the financial markets. This current volatility may persist over the coming days and weeks. However, the generally positive economic backdrop leads us to believe that market declines are buying opportunities.

Originally published at Stringer Asset Management

For more news, information, and strategy, visit the ETF Strategist Content Hub.

Originally published on ETF Trends

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

Read more commentaries by Stringer Asset Management