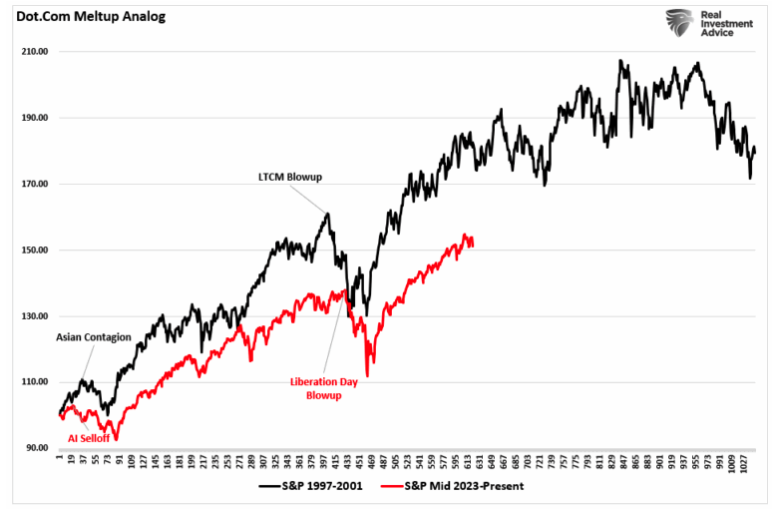

We’re hearing it everywhere: AI is in a bubble. The surge in capital, the parabolic stock charts, and the bold claims from CEOs all have a familiar rhythm. Nvidia’s valuation has soared, along with AI-related startups raising billions with little to no revenue. Investment in data centers, chips, and infrastructure is happening at a scale not seen since the internet boom of the 1990s, which immediately reminds investors of what happened next. The question isn’t whether AI is important; it’s whether the price of that importance is being inflated beyond reason. That is the nature of market bubbles.

Voices in the market are split. Some, like Jared Bernstein, former Biden CEA chairman, said:

“We point out that the share of the economy devoted to AI investment is nearly a third greater than the share of the economy devoted to internet related investments back during the dotcom bubble. So, we think there are enough analogies there to make the call.”

Others argue this is not a bubble, at least not yet.

“Macro bubbles” – asset price distortions with large economy-wide consequences – have generally involved not just overvalued asset prices but also dramatic impacts on spending and capital flows that have been both clues that a bubble is under way and forces that serve to undermine it.

The 1990s was a classic example. Alongside soaring equity prices, investment spending boomed, leverage rose, capital poured in, and profitability and balance sheet strength declined, while credit spreads and equity volatility moved higher. The macro and market imbalances that we saw then, particularly from 1998 onward, are not generally visible yet.” – Goldman Sachs

This split is normal. Every major innovation cycle creates a divide between skeptics who see overvaluation and optimists who see a new era of growth. The challenge for investors is not to take sides, but to understand what bubbles do, why they’re so hard to identify in real time, and how to benefit from them without being destroyed by them.

Yes, we may be in the second market bubble of this century. Alternatively, the market may be pricing in a shift as fundamental as the transition to either electricity or the internet. Either way, investors must think clearly, act deliberately, and avoid the kind of blind speculation that turned past booms into bloodbaths.

Market Bubbles Aren’t All Bad

Market bubbles carry a negative reputation because we witness the devastation in the aftermath of their collapse.

However, from a broader perspective, market bubbles also carry active value. During the inflation of a bubble, you see excessive optimism, capital flowing rapidly, and valuations detached from fundamentals. This is undoubtedly the case with respect to Artificial Intelligence as we currently see it.

Still, this environment often gives rise to genuine innovation. As Jeremy Grantham once argued:

“Bubbles are wonderful at generating new technologies.”

His point echoes through history.

Take the British railway mania of the 1840s. Investors poured capital into rail lines, many of which failed. However, in the end, the result was a vast transport network that transformed the economy. Or consider the late‑1990s dot‑com boom. The always wrong Paul Krugman once said:

“The Internet’s impact on the economy has been no greater than the fax machine.”

That quote was made during the height of the dot-com bubble, a period that many now consider a textbook example of financial excess. However, it also laid the foundation for the modern digital economy. The infrastructure that powers Amazon, Google, and Microsoft was created because billions of dollars flowed into companies, many of which failed. Yet their collective capital expenditures left behind fiber optic cables, server farms, and developer tools that enabled the next wave.

When capital floods into a technological frontier, many bets fail. But some win. That outcome sets a foundation for future growth.

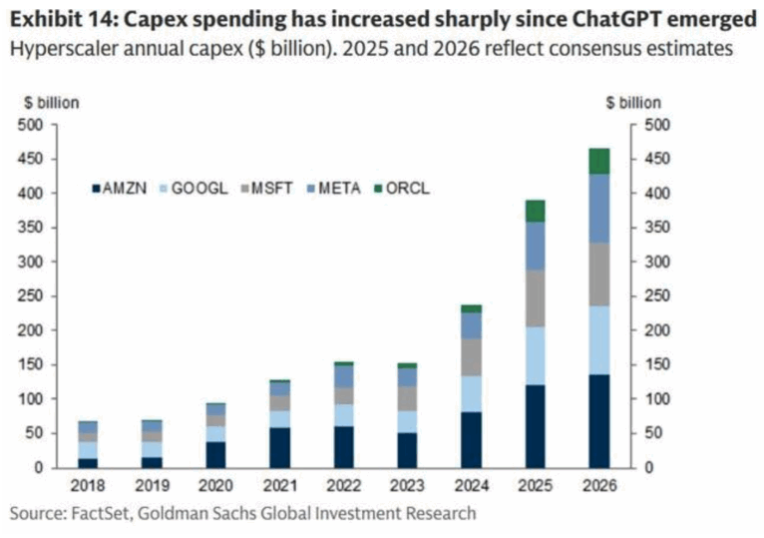

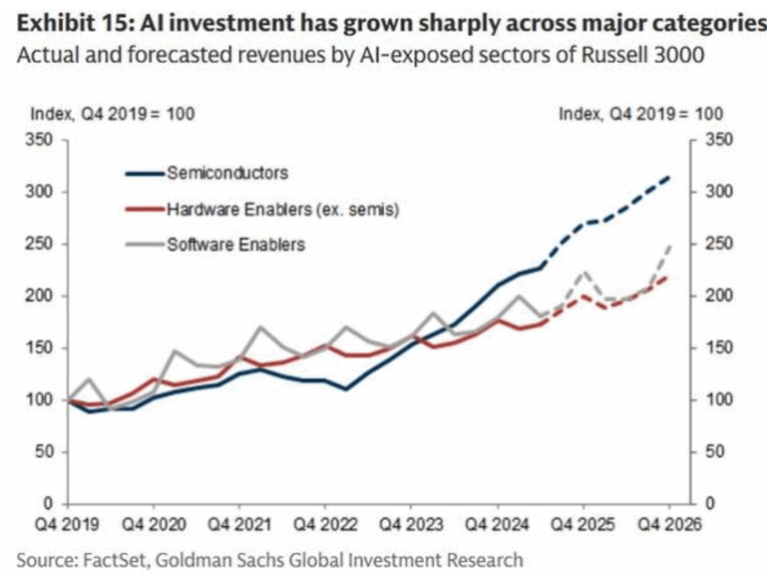

The AI boom is following a similar path. Companies are spending heavily on GPUs, data centers, and custom models. Most of them will not survive, but their investments are accelerating real capabilities. AI is being integrated into products, streamlining operations, and driving the creation of new business models. Nvidia, Microsoft, and Meta are racing to build the next layer of compute infrastructure. This isn’t abstract theory; it’s already showing up in earnings reports and productivity metrics.

Understanding that a bubble can be beneficial involves recognizing two key points.

- You don’t dismiss the boom simply because it is speculative. You acknowledge that capital is being deployed and that it will have future positive implications.

- You accept that risk is inherent during such periods. From one angle, the bubble looks reckless. However, from another, it seems like the stage where breakthroughs become possible. By appreciating the positive aspect, you gain clarity about what is happening and why it matters for investors.

You should treat a bubble not as a spectacle to be ignored, but as a phenomenon to be studied. Market bubbles are periods where capital loses discipline, but that loss of discipline funds the future. The value created during inflation often matters more than the value destroyed during the burst.

That’s why you don’t ignore market bubbles; you study them, respect them, and use them to your advantage.

Why Bubbles Are Only Obvious in Hindsight

Currently, many predict that the AI market bubble is set to burst. Every time the technology sector wobbles, the media is quick to push headlines of the end of the AI boom. However, each time, those warnings turned false and impaired investors who paid attention to them.

This doesn’t mean the warnings aren’t valid. Yes, current valuations are very high in many cases, and many of the companies either in the market today, or coming to it, likely won’t succeed. The problem is always the “timing” of the call.

For most investors, bubbles are never evident until they pop.

While rising prices may seem like evidence of irrational behavior, this may not be the case today or in the future if the future turns out as expected. Of course, there are a lot of “ifs” in that forecast. A good example was from Research Affiliates discussing Tesla (TSLA) in 2018:

“Tesla’s current price is arguably fair if most cars are powered by electricity in 10 years, if most of these cars are made by Tesla, if Tesla can make those cars with sufficient margin and quality control and can service the cars properly, and if Tesla can raise additional capital sufficient to cover a $3 billion annual cash drain and another billion to service its debt.”

As noted, there were many “ifs” in that statement. However, as we approach that 10th anniversary, TSLA is still operating and growing, but doesn’t sell MOST of the cars in America. However, for investors who bailed on Tesla in 2018, assuming it was a bubble, they have paid a price for that decision.

As noted, while the RA’s analysis was sound, that is what makes market bubbles so hard to identify. Valuations can exceed what you consider reasonable and remain elevated for longer than you anticipate.

In real-time, a bubble appears to be a trend backed by solid fundamentals. The early phases attract smart capital. The next phase brings in copycats and momentum traders. But by the time people start warning about a bubble, the narrative is fully established. Calling a market bubble too early can be just as costly as calling it too late. As Howard Marks wrote:

“Being too far ahead of your time is indistinguishable from being wrong.”

Even seasoned investors misjudge it. During the late 1990s, Warren Buffett was widely mocked for sitting out of the tech rally. His response was simple: he didn’t understand how to value the companies. He was right, eventually, but missed a massive run. Others, like Julian Robertson, tried to short the bubble and suffered enormous losses before it burst.

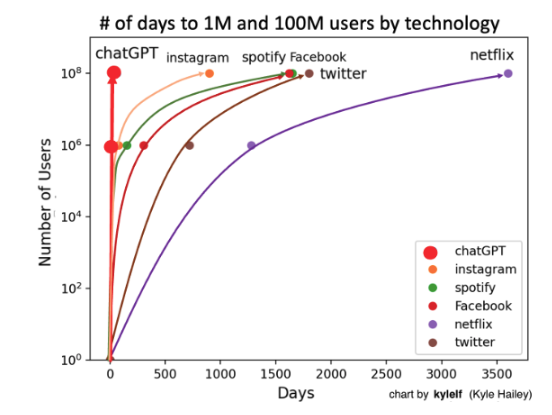

The AI surge fits the classic pattern. A legitimate breakthrough in computing power and algorithmic capability has led to rapid adoption. OpenAI’s ChatGPT reached 100 million users faster than any consumer product in history. Nvidia’s revenue tripled in a year. These facts are real. What’s unknown is how much of this growth is sustainable.

You only know it was a bubble when prices collapse and companies disappear. But by then, it’s too late to protect your capital. The Spyglass article put it well:

“You never really know it’s a bubble until the knife is already halfway through your chest.”

That’s why humility is essential.

If you think it might be a bubble, you’re already ahead of most investors. But timing it? That’s luck, not skill.

How to Participate During the Inflation and Avoid the Deflation

Participating in a bubble doesn’t mean going all in. It means allocating resources wisely, managing risk effectively, and knowing when to step back. The goal is not to call the top. It’s to avoid the worst of the collapse while capturing some of the upside.

Recognize the structural backdrop.

- AI is a genuine transformative technology. The AI surge entails substantial capital expenditures in data centers, chips, computing capacity, and cloud services. That means there is real substance beneath the hype.

- Nonetheless, the valuations and the speed of investment suggest that the market is pricing in extremely optimistic scenarios, characterized by high growth, low risk, and rapid monetization.

How you should position your investment. To participate while managing risk, you might follow these steps:

- Focus on companies with strong fundamentals and realistic business models. Since bubbles bring many “spray and pray” investments, your edge lies in filtering.

- Allocate only a portion of your portfolio to the “bubble zone,” and recognize the high-risk/high-reward nature.Do not rely on it for core returns.

-

Use this bubble to invest in infrastructure and enabling technologies rather than pure “moonshot” names. The infrastructure often survives the bust. For example, in the dot‑com era, the winners included those who built the backbone rather than the most hyped storefronts.

- Consider time‑horizon and liquidity. If you invest in bubble‐type assets, you must be prepared for high volatility and potential loss of capital if the bubble deflates.

How to avoid the consequences of the eventual deflation. Since bubbles eventually correct, you must adopt safeguards:

- Set exit rules. Define ahead of time the conditions under which you’ll reduce exposure (e.g., valuation multiple, margin of safety erosion, fundamental deterioration).

- Diversify across themes. Do not place all your bets in one bubble. If the bubble bursts, you want other anchors in your portfolio.

- Monitor fundamentals. The bubble phase often disconnects from fundamentals. When you observe that the disconnect is widening, the risk rises.

- Avoid leverage. Borrowing into a bubble makes the downside much steeper. Many historic bubble collapses were amplified by excessive debt.

- Keep long‑term winners in view. Some companies will emerge stronger post‑bubble. Try to identify them now, hold them, but be wary of paying hype‑driven valuations.

Start with this: focus on quality. In every bubble, a few companies emerge stronger. Amazon fell by over 90% during the dot-com crash but survived because it had a real business model and strong execution. The rest disappeared. Today, investors should look for companies with free cash flow, pricing power, and tangible applications of AI. Nvidia might be expensive, but it’s selling the picks and shovels in this gold rush. That’s a more sustainable model than a startup burning cash to fine-tune a chatbot.

Even using something as simple as a 40-week moving average can help you navigate both the inflation and deflation of a bubble.

No, you won’t get in at the bottom, or out at the top. But remember what is most important: participation is optional, but survival is mandatory.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Real Investment Advice

Read more commentaries by Real Investment Advice