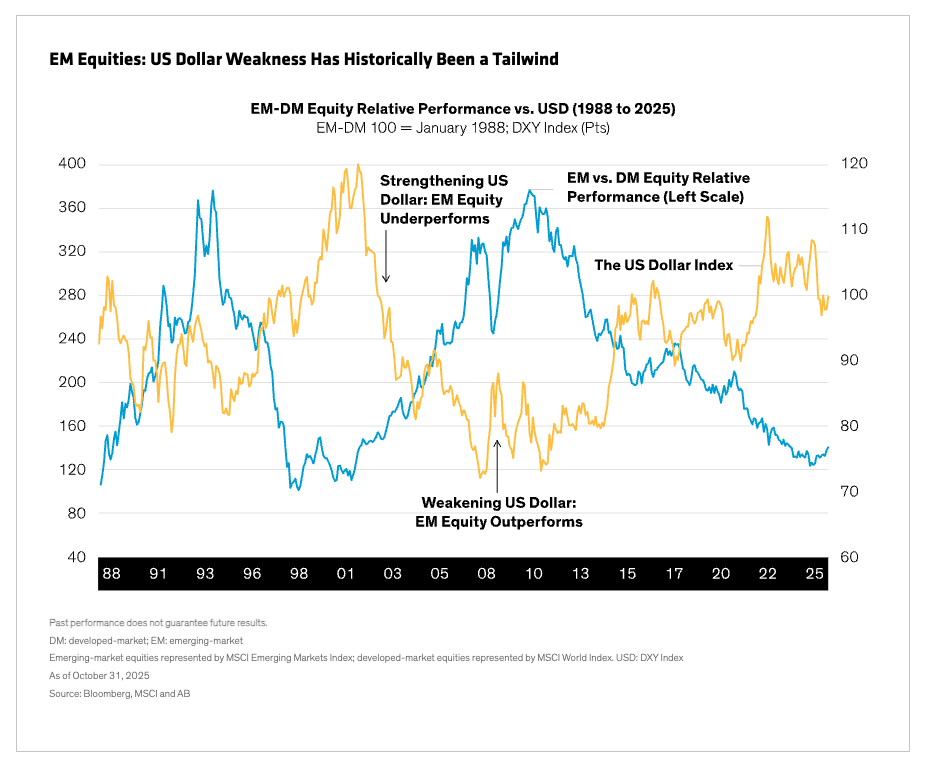

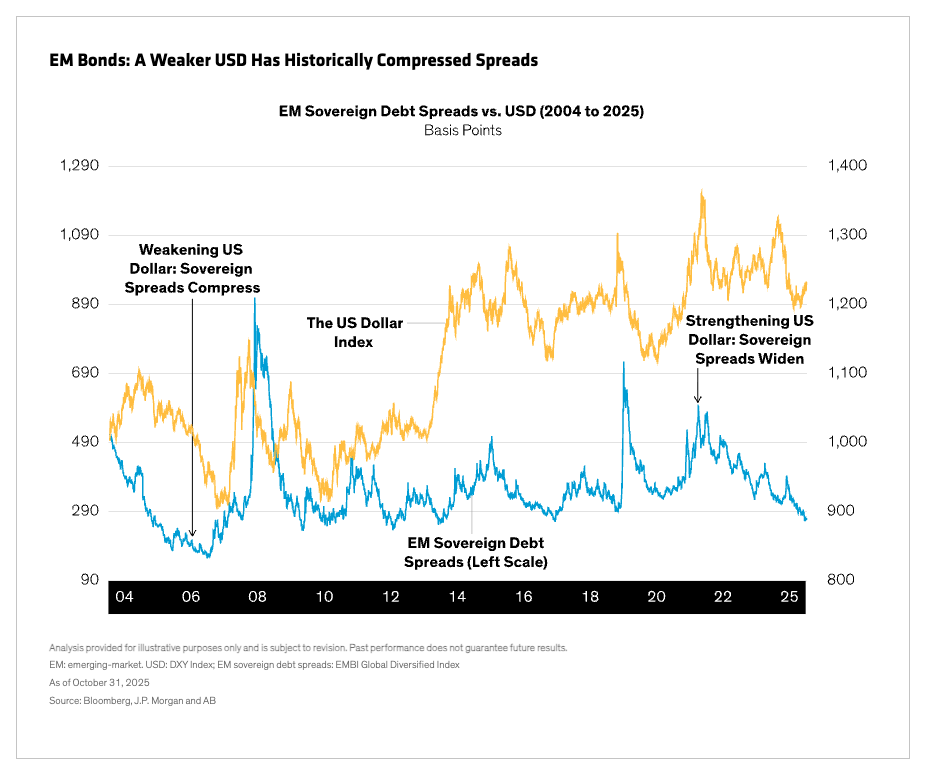

The US dollar (USD) has weakened over the last few months, fueling strong emerging-market (EM) stock and bond returns in 2025. Now, with more clarity around tariffs and the record-long US government shutdown resolved, will the greenback strengthen and flip the script on EM? We don’t think so.

Investors in EM have enjoyed a bumper year. The MSCI Emerging Markets Index surged by 33% in USD terms through October 31, nearly double the S&P 500’s return. Meanwhile, the J.P. Morgan Emerging Markets Bond Index rose 13%. After such strong gains, it’s a good time to gauge the forces affecting the dollar and their influence on EM stocks and bonds.

Six Forces Weighing on the Dollar

Several indicators suggest the USD weakness will continue.

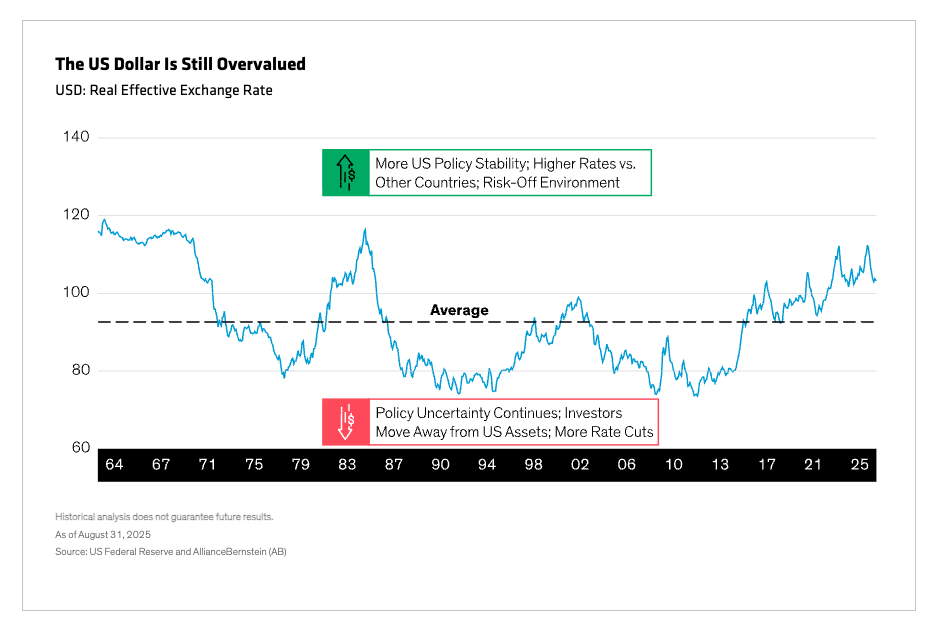

- Weak or strong, currency cycles tend to last years, not months. Since 1983, periods of dollar appreciation and depreciation alike have lasted about 10 years (Display). In this context, the USD is still relatively strong versus its long-term history, which is why we believe today’s weak cycle is likely just getting started and may last a while longer.

- Major central banks are gradually moving away from the USD to diversify reserves. For instance, China and Russia, historically among the largest USD investors, have shed considerable dollar holdings in recent years. A combination of shrinking demand, greater supply and negative market sentiment would tend to depreciate the currency over time.

- Foreign investors could be deterred by growing US deficits, which are at historical peacetime highs. Combined with America’s more internally focused policy, US debt may drive foreign investors to hold less US currency, or US assets in general, versus history.

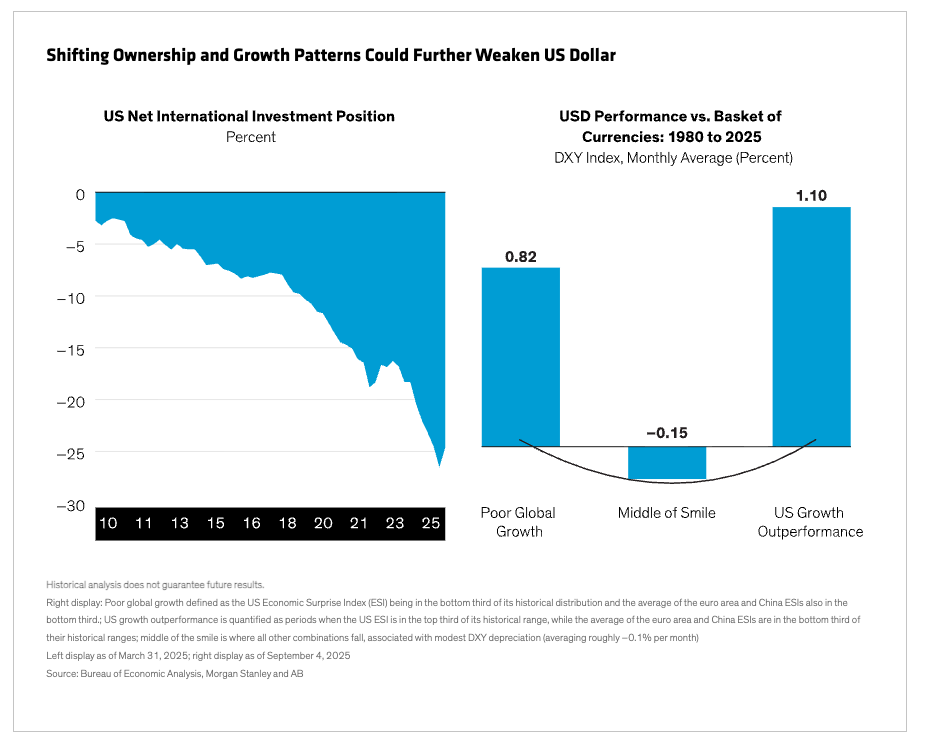

- Global investor overweight to USD-denominated assets leaves room to rebalance away from the currency. Foreign ownership of USD-denominated investments is near all-time highs. In fact, more foreigners invest in US assets than Americans invest overseas, as indicated by the –26% of GDP for the US net international investment position (Display). Since a weak USD shrinks the value of US assets in non-US currency terms, we think this may prompt more foreign investors to allocate away from US-denominated assets, potentially toward EM opportunities.

- The interest-rate differential between the US and other countries may start to narrow, which tends to weaken the USD. Historically, when interest-rate differentials widened, the dollar consistently strengthened (except briefly during April’s tariff turmoil). But with trade policy less fuzzy and the US Fed easing again, old patterns are reappearing. If the US cuts rates more than other developed markets, as we expect, the shrinking interest-rate differential should prompt further USD weakness.

- The greenback has historically softened when US growth aligns with other developed countries, which is currently the case. AB economists forecast US real GDP at a sluggish 1.7% for 2026, but relatively consistent with the 1.2% expected for other industrial countries. However, when the US outperformed or the global economic environment deteriorated, the dollar appreciated. The two upside extremes form the bookends of a so-called “dollar smile” (first advanced by Stephen Jen at Morgan Stanley), at which USD performance is currently at its smack-center weakest spot (Display, above).