Value is having its day—outside the United States. While US investors are piling into growthy companies lavishing money on artificial intelligence (AI) investments, in Europe and Japan, value has shined, with some value industries like European banks even outperforming the big US technology names in 2025.

For global investors, looking outside the United States may remain the best place for value in 2026, in our view, as the benefits of German fiscal stimulus finally come through and Japan’s new leader pushes to boost the domestic economy. US value could become resurgent should the substantial AI trade falter.

Unstoppable international value?

Even after the market runup in 2025, governmental fiscal policies, the potential benefits of monetary stimulus enacted this year, ongoing corporate governance changes and a weaker US dollar continue to make Europe and Japan appealing places to invest, in our view, despite ongoing political uncertainties.

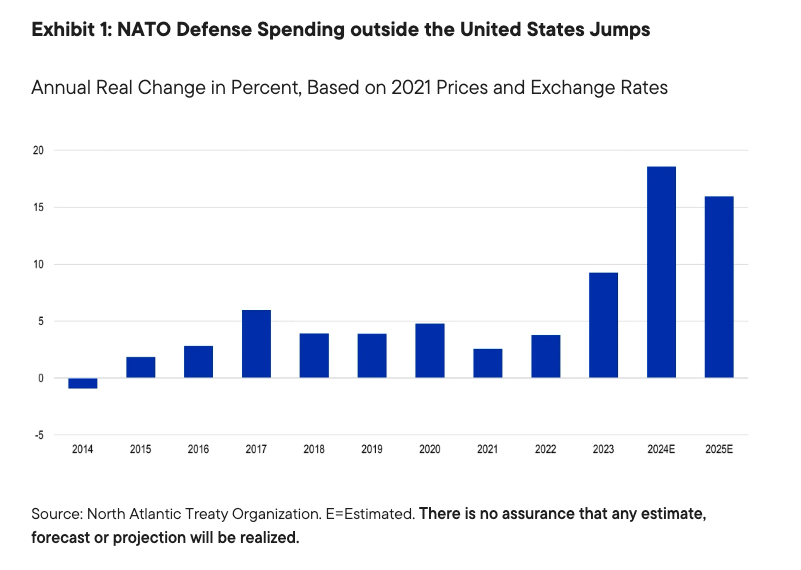

After years of sluggish economic activity, massive German fiscal stimulus should begin to feed through to the broader domestic and European economies in 2026. Not only will Germany and many other European countries be spending more on defense (see Exhibit 1), but they also have begun to invest in a wider range of civilian infrastructure, which can benefit those “old economy” value industries focused on building materials, roads, rails and the like. This German spending alone may boost broader eurozone gross domestic product growth by 0.25 percentage points from 2025 to 2027, according to the European Central Bank.1 In addition to boosting economic activity, it may also continue to propel regional stock markets higher over the coming few years.

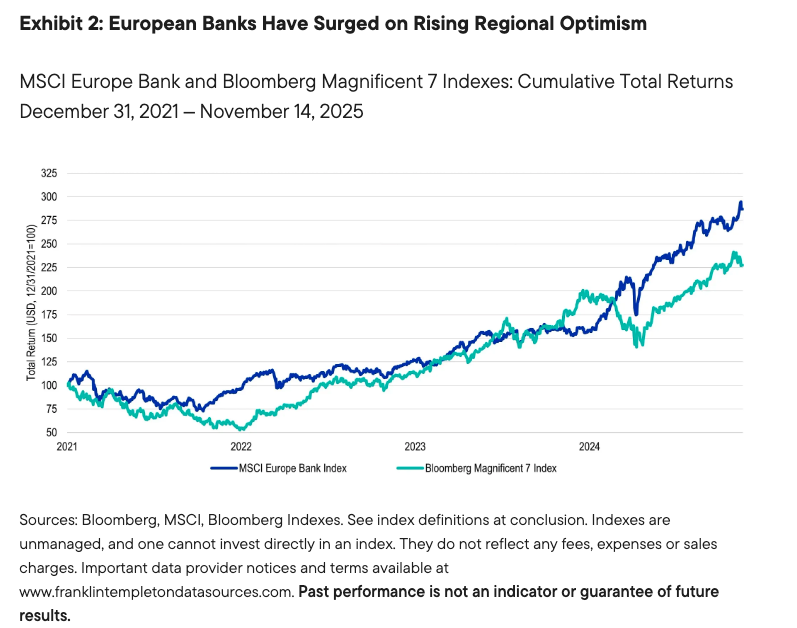

Banks may also benefit as loan demand increases. This optimism has already spilled over to bank stock prices. European banks have outperformed the US Magnificent Seven tech stocks significantly over the past year, further underscoring the strength in value investments abroad (see Exhibit 2).

Add the expected benefits from recently enacted interest-rate cuts and the slow but ongoing efforts to improve regional competitiveness, unify capital markets and pursue joint debt issuance, and European value stocks can see recurring benefits—potentially for years.

Meanwhile, in Japan, new Prime Minister Sanae Takaichi is focused on further boosting economic growth, which can also support a range of the country’s more domestically focused firms. Her policy proposals include new efforts to dampen inflation, investment in growth industries and more defense spending.

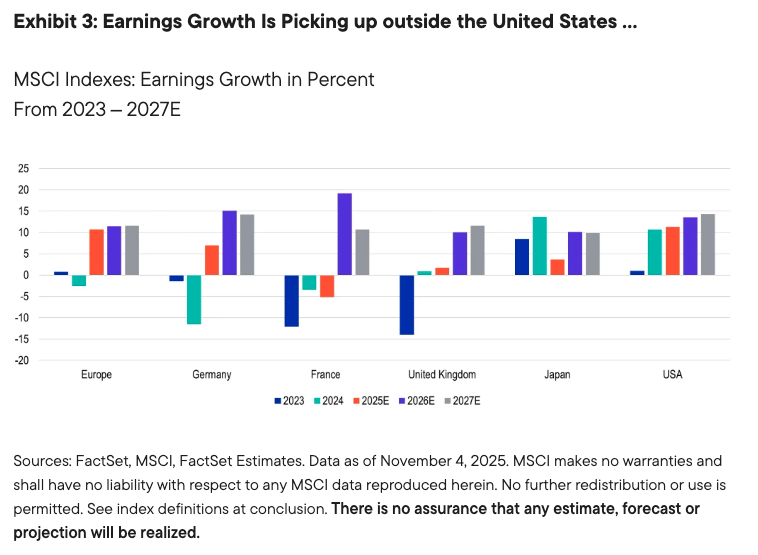

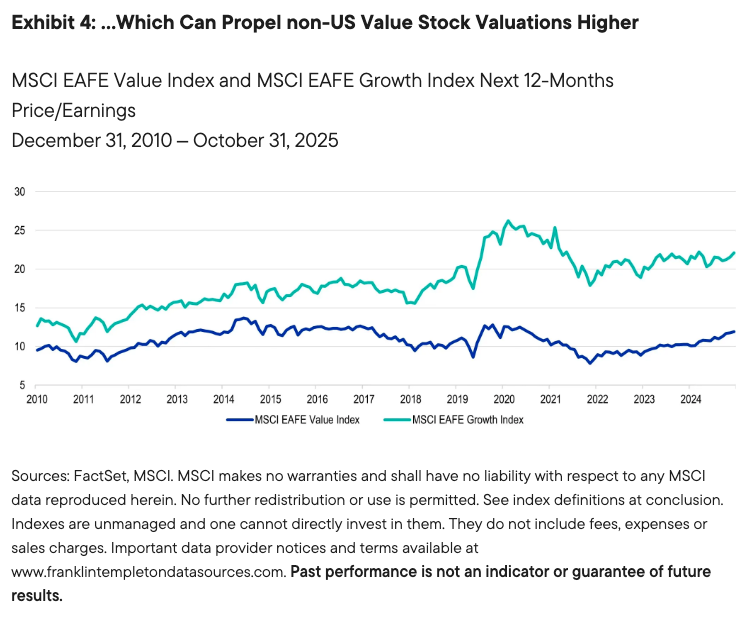

Japanese and European companies also are returning more cash to shareholders, and a possible pickup in merger activity may continue to bolster non-US stocks over time. Japanese companies are also unwinding their complicated cross-shareholdings and buying back stock—positives for investors. And with earnings likely to improve (see Exhibit 3), the appealing valuations for international stocks could climb and narrow the gap between both international growth and US stocks (see Exhibit 4).

Spottier US value opportunities

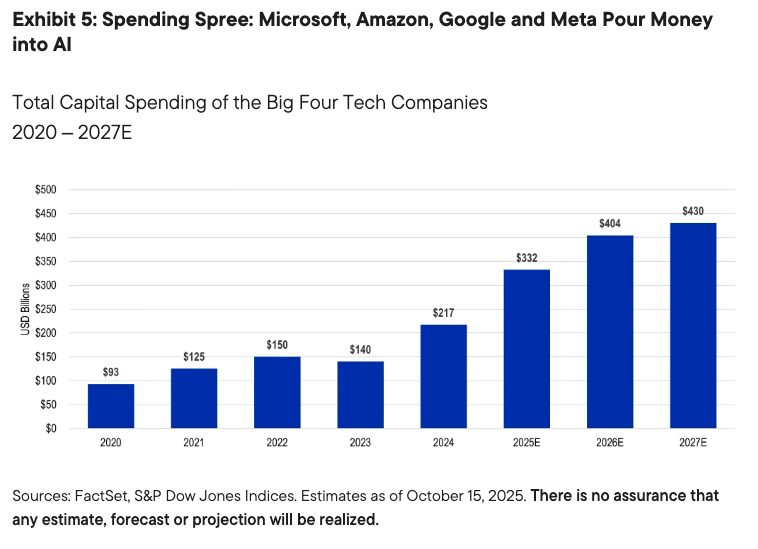

Unlike international markets, the US market may remain a challenging place for value investing in 2026, particularly should the enthusiasm for AI continue unabated. Massive AI capital spending (see Exhibit 5) has been propelling US economic growth, and the wealth effect has been driving increased consumer spending. On the other hand, should investment returns on these sizable spending plans not materialize or should they disappoint, any resulting market correction, given the extreme market concentration, could bring value stocks back to the fore.

In the meantime, we expect to find individual value opportunities across the US market in 2026. We have seen companies that do not have AI narrative support succumb to serious corrections following disappointing earnings, helping to create interesting places to find value. Unloved companies in stable economic areas are also attractive value opportunities, in our view, as we have found select consumer staples stocks with solid balance sheets trading at lower valuations than they have historically.

Taking a broader view of value also may help uncover attractive individual opportunities. We don’t believe a low price/earnings ratio necessarily makes for a value stock. We advocate looking for companies that offer growth but where the stock price is trading at a discount attractive enough to provide appealing upside as the market gradually begins to recognize that growth over time.

And with US value stocks trading at a substantial discount to their growth peers—a 21 price/earnings ratio versus nearly 44 for growth stocks at the end of October, according to FactSet data—there may be ample opportunities for individual US value stocks to rerate over time, in our view.

The current US administration also is likely to foster a more robust merger environment. Not only should merger arbitrage opportunities proliferate if spreads between the offer price and the spot stock price widens, but we may also see greater deal activity among small and mid-sized companies, a potential catalyst for smaller-cap US stocks. We expect lower US interest rates, along with better earnings and a more favorable regulatory backdrop, to further help smaller value companies deliver strong long-term risk-adjusted returns.

Riskier business

Although we are broadly optimistic about the outlook for value, we are cognizant of the potential risks as we enter 2026. We have seen recent trouble in the private credit market, following the bankruptcy of a subprime auto company, an auto parts supplier and other apparently one-off issues, but the trends bear watching.

Additionally, US interest rates are forecast to fall, which has stoked market gains in late 2025, but higher rates because of the potential inflationary pressures from tariffs could mean rates may need to rise in 2026, potentially upending current market thinking. Economic challenges arising from any downturn in the AI spending boom pose risks too.

While investors should closely watch these potential hazards in 2026, we remain bullish on value more broadly. Bottom-up stock selection remains crucial, in our view, to finding those attractive stocks trading at sizable valuation discounts while simultaneously offering catalysts that can allow the market to realize this value over time. We think international markets remain the first place to look for them.

Endnote

1. Source: “Eurosystem staff macroeconomic projections for the euro area.” European Central Bank. June 2025.

INDEXES

Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Important data provider notices and terms available at www.franklintempletondatasources.com.

The Bloomberg Magnificent 7 Total Return Index is an equal-dollar-weighted equity benchmark consisting of a fixed basket of seven widely traded companies classified in the United States. It includes Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla.

The MSCI EAFE Growth Index captures large- and mid-cap securities exhibiting overall growth style characteristics across developed markets countries around the world, excluding the United States and Canada.

The MSCI EAFE Value Index captures large- and mid-cap securities exhibiting overall value style characteristics across developed markets countries around the world, excluding the United States and Canada.

The MSCI Europe Index captures large- and mid-cap representation across Developed Markets (DM) countries in Europe.

The MSCI Europe Banks Index is composed of large- and mid-cap stocks across developed markets and countries in Europe.

The MSCI France Index is designed to measure the performance of the large- and mid-cap segments of the French market.

The MSCI Germany Index is designed to measure the performance of the large- and mid-cap segments of the German market.

The MSCI Japan Index is designed to measure the performance of the large- and mid-cap segments of the Japanese market.

The MSCI United Kingdom Index is designed to measure the performance of the large- and mid-cap segments of the UK market.

The MSCI USA Index is designed to measure the performance of the large- and mid-cap segments of the US market.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

To the extent the strategy invests in companies in a specific country or region, it may experience greater volatility than a strategy that is more broadly diversified geographically.

Diversification does not guarantee a profit or protect against a loss.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Investments in companies in a specific country or region may experience greater volatility than those that are more broadly diversified geographically.

The investment style may become out of favor, which may have a negative impact on performance. Large-capitalization companies may fall out of favor with investors based on market and economic conditions

Investments in companies engaged in mergers, reorganizations or liquidations also involve special risks as pending deals may not be completed on time or on favorable terms.

Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

WF: 7594609

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.