As investors enter the distribution phase of their financial lives, the priorities of portfolio construction shift dramatically. Liquidity becomes essential, diversification grows more important, and the ability to meet income needs – sometimes by tapping into principal – must be balanced against risk and market volatility. Fixed income typically becomes a larger share of the overall allocation as time horizons shorten and risk tolerance declines. While individual bonds and bond mutual funds have historically been the primary vehicles for fixed income exposure, each can present meaningful challenges for retirees and near-retirees. In contrast, bond ETFs can offer a blend of flexibility, liquidity, transparency, and tax efficiency that make them particularly well-suited for distribution-phase portfolios. This article explores the limitations of individual bonds, the drawbacks of traditional bond funds, and why ETFs often provide the most practical solution.

Part 1: The Challenge With Buying Individual Bonds

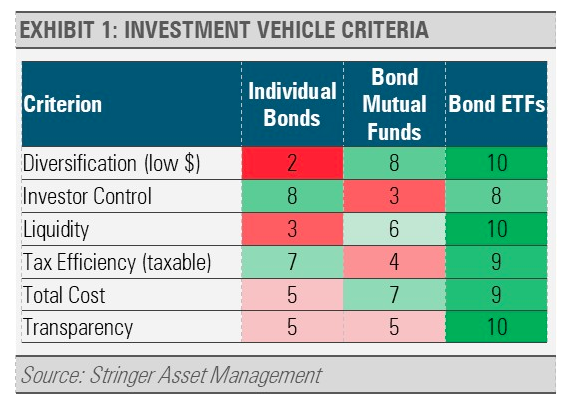

On the surface, individual bonds appear to offer simplicity and predictability – fixed coupons, stated maturities, and the ability to plan cash flows with precision. However, for most investors in the distribution phase, building and maintaining a portfolio of individual bonds is far more complex and often impractical. A major issue is diversification and properly diversifying across issuers, maturities, and credit qualities. An investor generally needs at least $500,000 dedicated specifically to fixed income to diversify with individual bonds, implying a total portfolio size of roughly $1 million if the target allocation is 50% bonds. Below this level, investors may concentrate too heavily in too few positions, increasing the risk that any single issuer or sector could negatively affect their income or liquidity needs.

Even for larger portfolios, liquidity can remain a significant challenge. Individual bonds trade over the counter, meaning pricing is less transparent and spreads can be wide, particularly during periods of market stress. It is not uncommon for liquidity to dry up entirely when volatility spikes, leaving retirees with the unwelcome choice of holding bonds they would prefer to sell or accepting unfavorable pricing to raise cash. This is especially problematic for distribution-phase investors who may need to generate funds unexpectedly, or whose withdrawal schedules cannot be easily altered.

Additionally, while holding individual bonds to maturity can eliminate mark-to-market concerns, it introduces reinvestment risk as shorter maturities roll off. When that happens, a retiree may be forced to reinvest proceeds into an interest-rate environment that is less favorable than before. Managing ladders across a wide range of maturities requires ongoing attention, and longer-term bonds – often purchased for higher yields – increase exposure to duration risk. For those without large portfolios or the ability to withstand illiquidity, the complexity and cost of managing individual bonds often outweigh the perceived benefits.

Part 2: The Challenge With Buying Bond Mutual Funds

Bond mutual funds remain a staple in many retirement portfolios, but they come with notable drawbacks, particularly when held in taxable accounts. The most persistent challenge is tax inefficiency. The interest paid by most bonds held in mutual funds is taxed as ordinary income, typically the highest rate an investor pays. More importantly, mutual funds are required to distribute capital gains annually, even when those gains result from the manager selling underlying bonds for portfolio management reasons rather than investor-driven redemptions. Investors cannot control when these gains are realized, which makes tax planning more difficult and less predictable.

This lack of control extends to portfolio activity more broadly. A retiree may prefer to delay realizing gains or offset them with losses in other parts of the portfolio, but a mutual fund’s internal trading activity may trigger taxable events regardless of the investor’s intentions. Funds with high turnover ratios can generate a stream of taxable distributions, even for shareholders who have only recently purchased shares. For retirees in the distribution phase – who often seek consistency, predictability, and precise tax management – these unpredictable distributions can be disruptive.

Transparency is another issue. Unlike ETFs, which generally publish complete holdings daily, many mutual funds report holdings monthly or quarterly, often with a lag. This can leave investors uncertain about the duration risk, credit quality, or sector exposure they currently hold. For individuals who rely on their fixed income allocation to provide stability and meet ongoing income needs, the limited visibility and tax complexities of mutual funds can make them less than ideal.

Part 3: The Solution — Bond ETFs

Bond ETFs address many of the challenges posed by both individual bonds and mutual funds, making them particularly attractive for investors in the distribution phase. One of the most compelling advantages is liquidity. ETFs trade intraday on exchanges, allowing investors to buy or sell at transparent prices whenever needed. During periods of market volatility – when liquidity in the individual bond market often collapses – ETFs have historically maintained more consistent trading activity, providing retirees with the ability to raise cash without undue stress or price uncertainty.

Beyond liquidity, ETFs offer instant diversification with low minimums. Even small portfolios can access hundreds or thousands of bonds through a single ETF, achieving a level of diversification that would be impractical or impossible through direct bond purchases. Daily transparency into holdings allows investors and advisors to monitor duration, credit quality, and overall exposure with precision.

ETFs also stand out for their tax efficiency. Unlike mutual funds, which must distribute capital gains annually, ETFs generally avoid these distributions thanks to their in-kind creation and redemption process. This makes them particularly effective for retirees managing taxable accounts, as they retain far greater control over when and how gains are realized. Combined with typically lower expense ratios and minimal transaction costs compared to individual bonds or mutual funds, ETFs provide a flexible, transparent, and cost-effective solution that aligns well with the needs of investors drawing down assets over time.

In recent years, an important evolution in the marketplace has further strengthened the case for using ETFs during the distribution phase: the rise of fixed income managers who build professionally managed portfolios exclusively using ETFs. These managers deliver all the structural advantages of ETFs, such as liquidity, diversification, transparency, and tax efficiency, while adding a layer of active oversight and expertise that was once available only through institutional separate accounts or expensive custom bond ladders. In periods of changing interest rates, yield-curve instability, or market uncertainty, having a skilled manager who can tactically adjust duration, credit exposure, and sector weightings can be incredibly valuable.

This development represents a major advancement in the industry. High-caliber, actively managed fixed income strategies, once accessible only to large institutional accounts or high-net-worth investors, are now available to more modest retail investors through ETF-based portfolio management. It democratizes professional bond management in a way that was not possible in years past, providing everyday investors with sophisticated tools to navigate a complex and ever-evolving fixed income landscape.

Conclusion

For investors in the distribution phase, selecting the right fixed income approach is critical to meeting cash-flow needs, managing risk, and preserving long-term portfolio sustainability. While individual bonds offer predictability, they demand large portfolios and sacrifice liquidity. Bond mutual funds provide professional management but introduce tax inefficiency, limited transparency, and a lack of control over gains. Bond ETFs, by contrast, combine liquidity, diversification, transparency, flexibility, and tax efficiency in a way that directly addresses the challenges retirees face. For most investors seeking a resilient and adaptable fixed income solution in retirement, ETFs offer the most balanced and practical approach.

Originally published on ETF Trends

For more news, information, and strategy, visit the ETF Strategist Content Hub.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

Read more commentaries by Stringer Asset Management