Emerging market (EM) equities are thriving following more than a decade of underperformance.

Valuations remain attractive, the macroeconomic backdrop is supportive, and we believe increased positive market sentiment should drive the asset class forward.

Structural market drivers remain, with technology surging on strong earnings, China recovering and India offering long term opportunities.

The year 2025 had lined up to be a challenging one for emerging market (EM) equities. We witnessed growing global trade tensions following the US Liberation Day tariff announcements but then the economic backdrop took a sharp turnaround for the better. A de-escalation of trade wars, a falling US dollar and macroeconomic stabilization of China all marked positive news for EM equities, resulting in a strong year for the asset class as investors have been rewarded with impressive returns of over 30% through mid-November.

Following over a decade of underperformance, the tides seem to have now turned, and we believe the EM market recovery is at an early stage. Valuations look appealing to us, global macroeconomic drivers are supportive and local structural and company-level opportunities all point toward significant upside potential for the asset class.

However, as we look forward to 2026, we think job creation could pick up to 80,000 or 90,000 per month on the back of Federal Reserve interest-rate cuts, the peak fiscal impulse of the Trump Administration's "One Big Beautiful Bill" and more visibility on the tariff front once we get the US Supreme Court’s decision on the legality of the International Emergency Economic Powers Act (IEEPA) tariffs. Although this is lower than the past several years, we believe it is certainly enough to keep this expansion moving forward.

Macro tailwinds powering the EM recovery

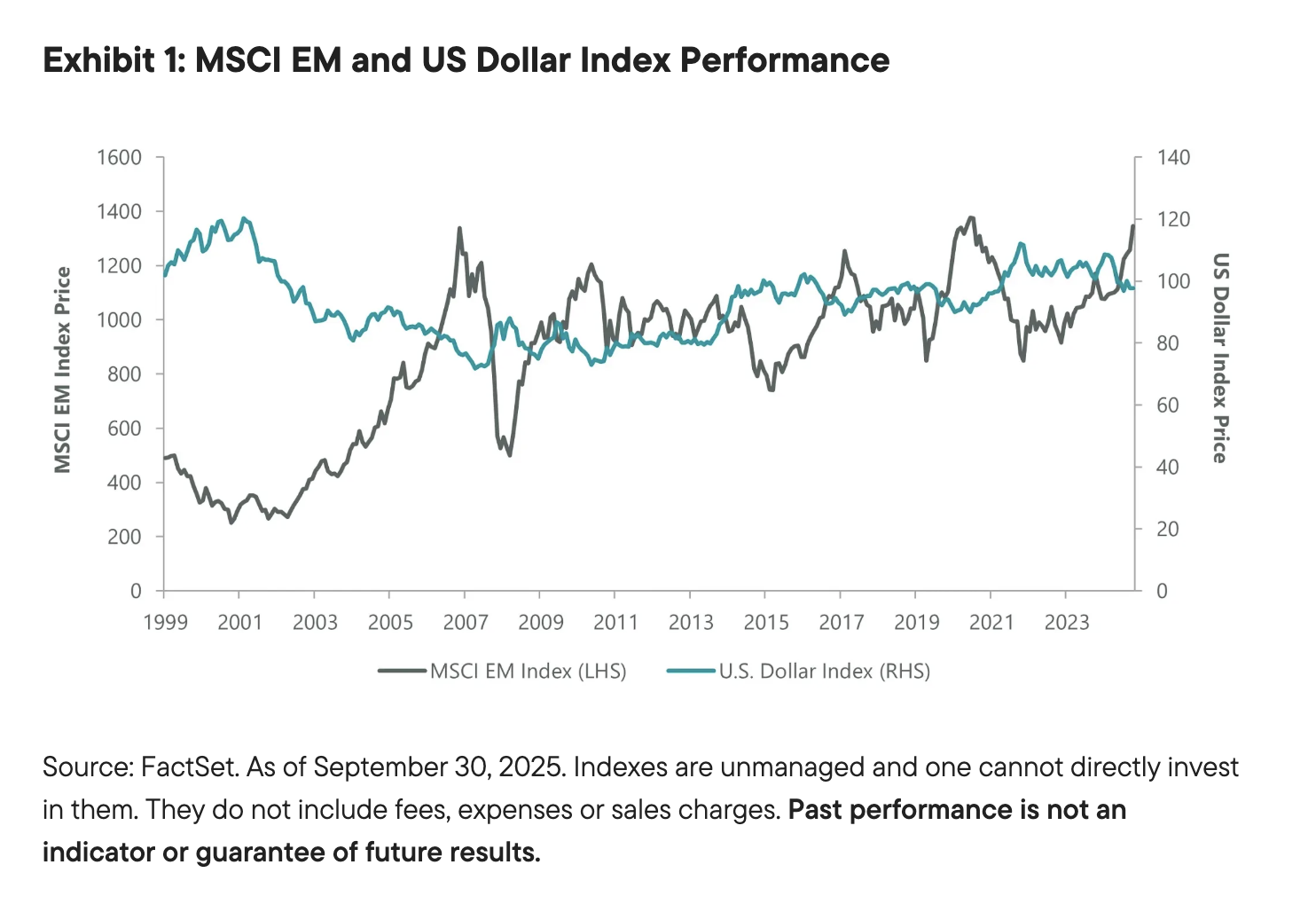

EMs—a collection of individual countries, with differing economic, political and corporate backdrops—have one thing in common: their reliance on the US economy. In 2025, we say yet another reminder of this as the United States demonstrated steady positive economic performance, combined with a weaker US dollar and rate cuts in the second half, creating ideal conditions for EM equity performance.

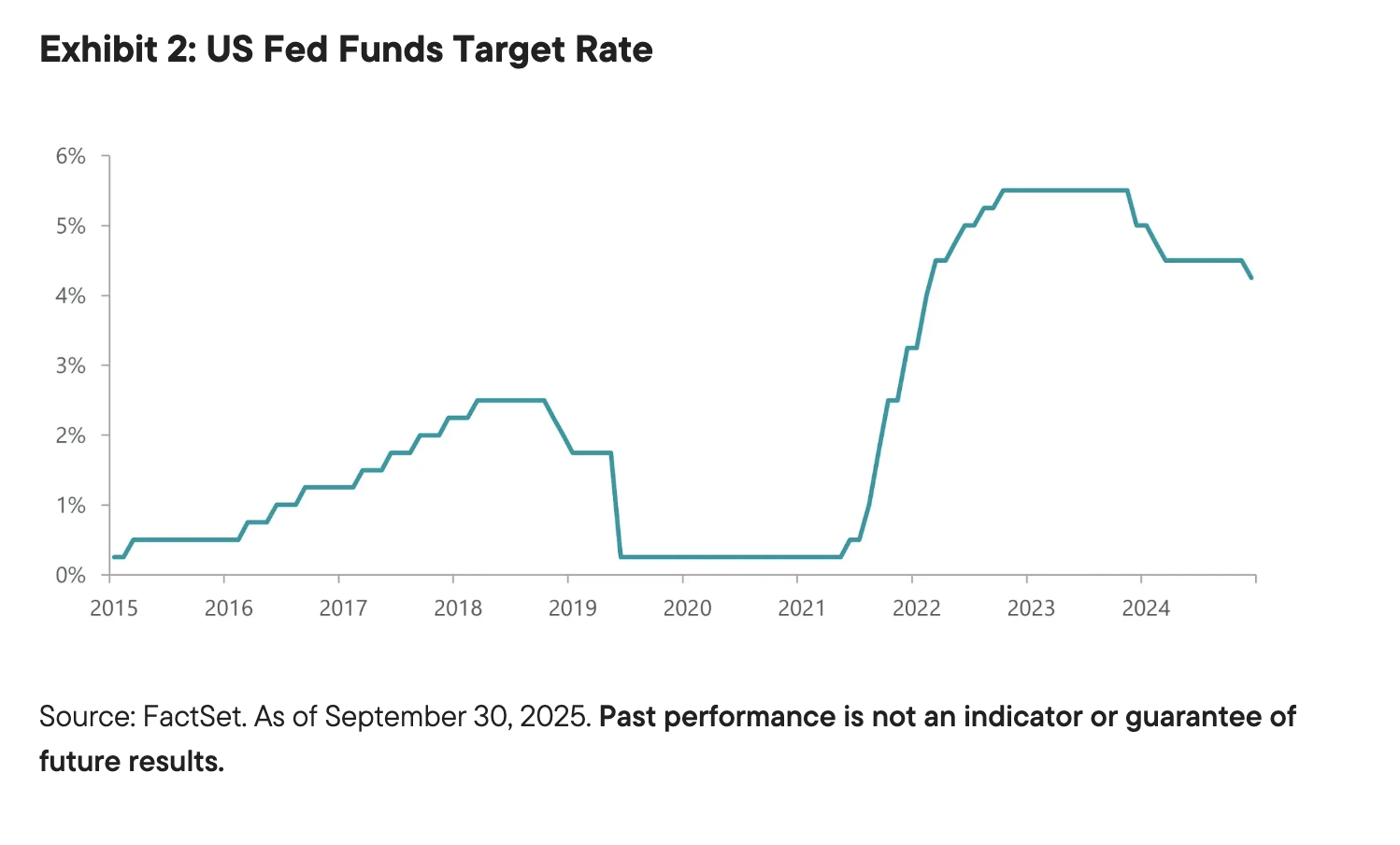

EM equities typically benefit from a stable or depreciating US dollar (Exhibit 1) because of lower US-denominated debt servicing costs, commodity exporter tailwinds and increased monetary policy flexibility, which can facilitate lowering rates and supporting economic growth. All indications suggest to us this supportive dollar environment will likely remain in 2026. The Federal Reserve is forecast to continue cutting rates (Exhibit 2), suggesting the environment will become even more supportive of EM equities.

International asset flows are also critical in driving prices for EM markets. The opportunity offered by lower valuations, combined with stronger economic growth and improving investor sentiment, creates a virtuous cycle attracting increased foreign capital flows. In turn, this further enhances potential investment performance. We’re still at an early stage in this process and anticipate increased foreign investments into EM equities over the coming years. In the meantime, we are bullish on three major themes in the year ahead: China, technology and India.

China: Quality and growth at a discount

The Chinese economy has begun to demonstrate increased stability, with trade tensions easing, exports remaining strong and a generally more optimistic outlook emerging. Our earlier belief that China wouldn’t separate much from the global economy has proven true, as relationships have improved and investors have regained confidence.

China’s policy pivot from a focus on deleveraging toward targeting growth has been gentler than anticipated, and the government has implemented mild stimulus measures focused on stabilizing the property sector to avoid overstimulating the broader economy. As a result, we are seeing a divergence in economic performance, with exporters and the industrial sectors booming and consumer demand and the property market subdued and drifting lower, respectively. While we don’t anticipate major economic stimulus, we do expect a continuation of targeted policy adjustments. The real opportunity lies in those pockets of the economy that are still thriving, particularly within technology, innovation and export-oriented businesses.

The recent strong performance of Chinese equities has not eliminated the significant valuation upside for high-quality, high-growth businesses. While the broader Chinese market has rebounded, many Chinese stocks remain near five-year valuation lows, suggesting substantial re-rating potential. We believe active equity managers are well-suited to thrive in this current market environment.

Technology: Undervalued EM tech poised for catch-up

While the United States is the first place many investors think of for tech investment, EM also offers the opportunity to invest in world-class companies with cutting-edge technological innovation. Many are benefiting from substantial investment in research and development and intellectual property creation. EM tech is best known for providing exposure to key global supply-chain components for tech hardware. However, its growing reputation for world-leading innovation was further bolstered in 2025 with the launch of China’s DeepSeek chatbot, which sent shockwaves around the world as it shone a light on Chinese advancement in cutting-edge artificial intelligence (AI).

Technology investment in emerging markets can be found across industries; we see opportunities in areas such as industrial automation, e-commerce and fintech, as well as technological advancement driving increased global power demand amid the electrification of transport, heating and industry. This increased demand is further accelerating with the increasing energy demand from AI data centers. However, the old power networks are not ready or capable of meeting these increased electricity needs, meaning critical infrastructure investments are required.

As we look forward to 2026, the US technology sector is currently trading at 31x forward price/earnings (P/E), providing concerns to many market participants. This contrasts starkly with EM technology stocks, which trade at only 18x. These same EM tech stocks have forecast earnings that are expected to outpace their US counterparts over the next three years.

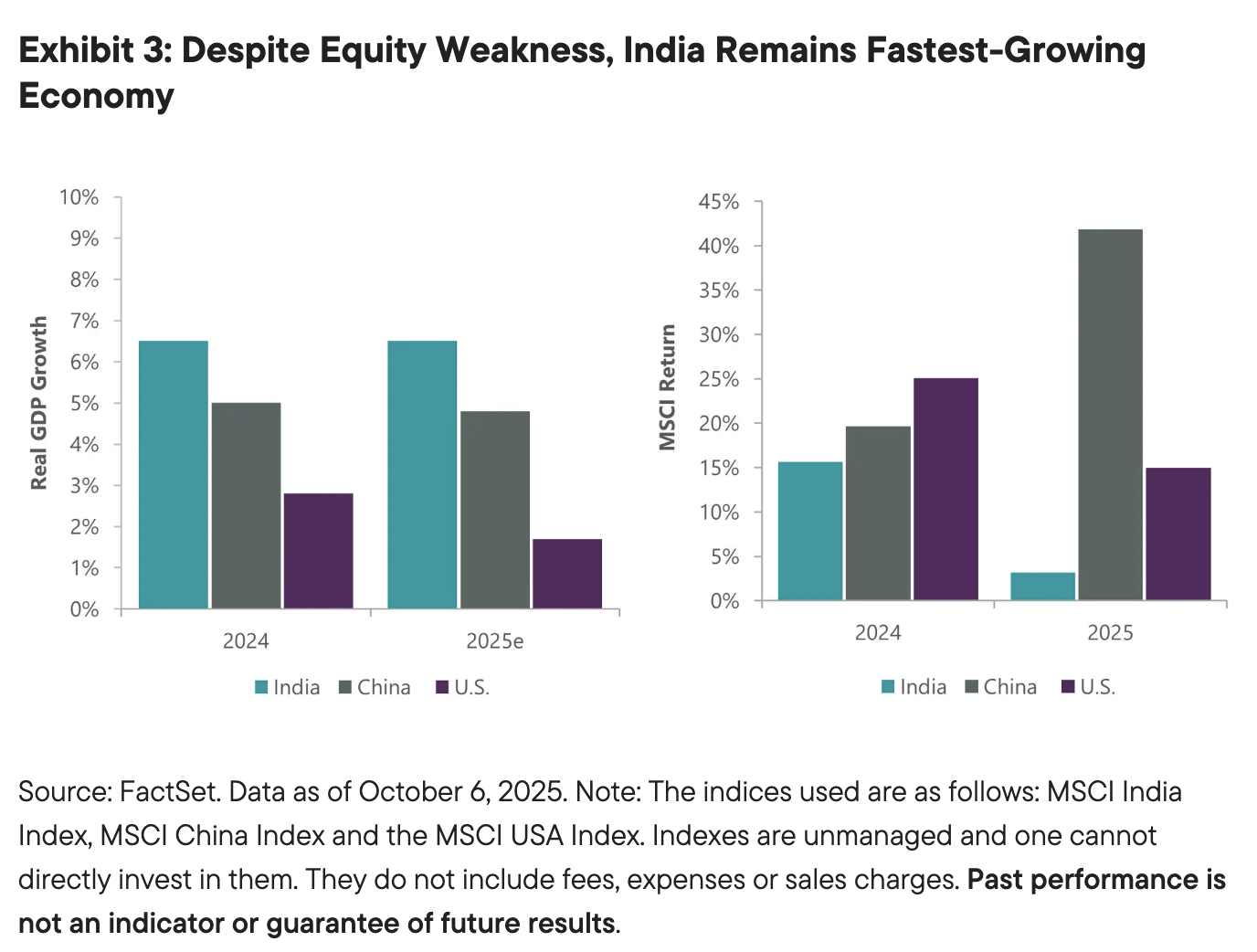

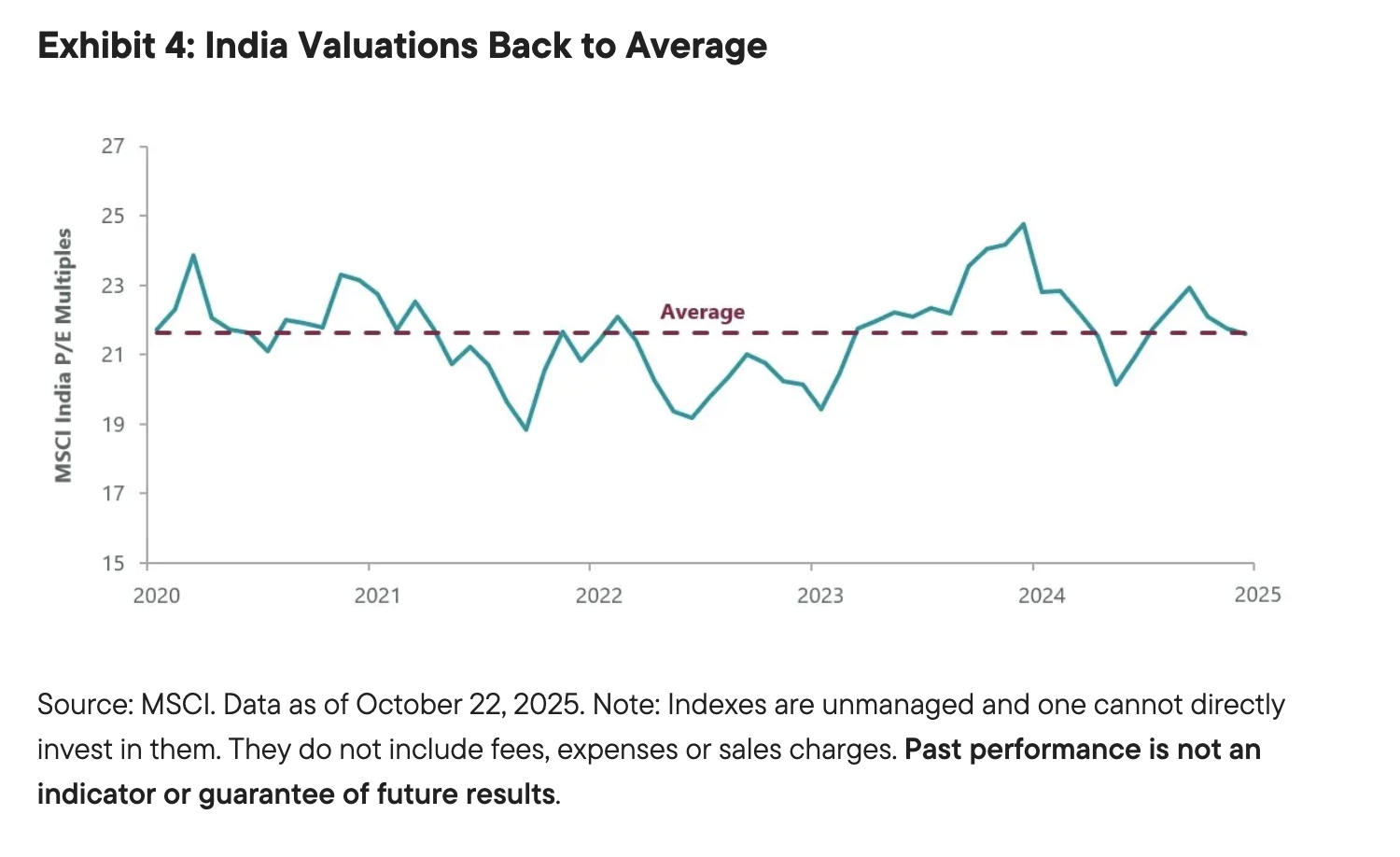

Following the 2024 election, 2025 has been a challenging year for Indian equities, with negative economic growth revisions and consumer softness. However, the long-term investment case remains robust. We believe India's equity market offers great upside potential as it benefits from a large and young population, and it remains the fastest-growing major global economy, with real gross domestic product (GDP) growth of 6.6% compared to 4.2% for EM overall (Exhibit 3). Indian valuations have seen a correction back to long-term levels (Exhibit 4), reinforcing the importance of active management to gain exposure to company-level opportunities. We see long-term opportunities in Indian banks, consumer discretionary stocks as well as the IT services industry, which is beginning to exhibit signs of stabilization from negative sentiment around AI risks.

Conclusion

Investments in emerging markets equities aren’t simply a play on global macroeconomic factors and international asset flows. They also provide exposure to many countries offering economic growth rates faster than most developed nations and long-term structural trends such as an expanding middle class consumer and favorable demographics in select markets that can help drive company returns.

We believe EM equities have turned a corner, showing strong performance after years of lagging returns. As the environment remains favorable, we believe the outlook for the asset class looks positive, with further growth and re-rating potential on the horizon for investors willing to take a selective, stock-driven approach.

DEFINITIONS

The MSCI Emerging Markets Index captures large and mid-cap representation across 23 emerging markets (EM) countries. With 835 constituents, the index covers approximately 85% of the free float adjusted market capitalization in each country.

The US Dollar Index indicates the general international value of the US dollar and is calculated with a weighted average of the exchange rates between the dollar and six major world currencies. The InterContinental Exchange computes the index using rates supplied by 500 banks.

The MSCI India Index is designed to measure the performance of the large and mid-cap segments of the Indian market. With 64 constituents, the index covers approximately 85% of the Indian equity universe.

The MSCI China Index captures large and mid-cap representation across China H shares, B shares, Red chips and P chips. With 140 constituents, the index covers about 85% of this China equity universe.

The price-to-earnings (P/E) ratio is a stock's (or index’s) price divided by its earnings per share (or index earnings). The forward P/E ratio is a stock’s (or index’s) current price divided by its estimated earnings per share (or estimated index earnings), usually one-year ahead.

The One Big Beautiful Bill Act, or the Big Beautiful Bill (OBBB), is a US federal statute passed by the 119th United States Congress containing tax and spending policies that form the core of President Donald Trump's second-term agenda. The bill was signed into law by President Trump on July 4, 2025.

The International Emergency Economic Powers Act (IEEPA) provides the President broad authority to regulate a variety of economic transactions following a declaration of national emergency.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Equity securities are subject to price fluctuation and possible loss of principal. Large-capitalization companies may fall out of favor with investors based on market and economic conditions. Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

US Treasuries are direct debt obligations issued and backed by the “full faith and credit” of the US government. The US government guarantees the principal and interest payments on US Treasuries when the securities are held to maturity. Unlike US Treasuries, debt securities issued by the federal agencies and instrumentalities and related investments may or may not be backed by the full faith and credit of the US government. Even when the US government guarantees principal and interest payments on securities, this guarantee does not apply to losses resulting from declines in the market value of these securities.

Active management does not ensure gains or protect against market declines.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Investments in companies in a specific country or region may experience greater volatility than those that are more broadly diversified geographically. The government’s participation in the economy is still high and, therefore, investments in China will be subject to larger regulatory risk levels compared to many other countries.

WF: 7662712

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.