AI Data Centers Could Consume Half a Million Tons of Copper Annually by 2030

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsA conventional data center uses between 5,000 and 15,000 tons of copper. A hyperscale data center, on the other hand—the kind being built to run artificial intelligence (AI)—can require up to 50,000 tons of copper per facility, according to the Copper Development Association.

Think about that for a second. A single AI data center that uses more copper than three conventional facilities combined.

That’s why I think the AI story is about much more than just raw compute power. It also involves electrical infrastructure at a scale we’ve never seen before. And these massive facilities have an insatiable appetite for copper.

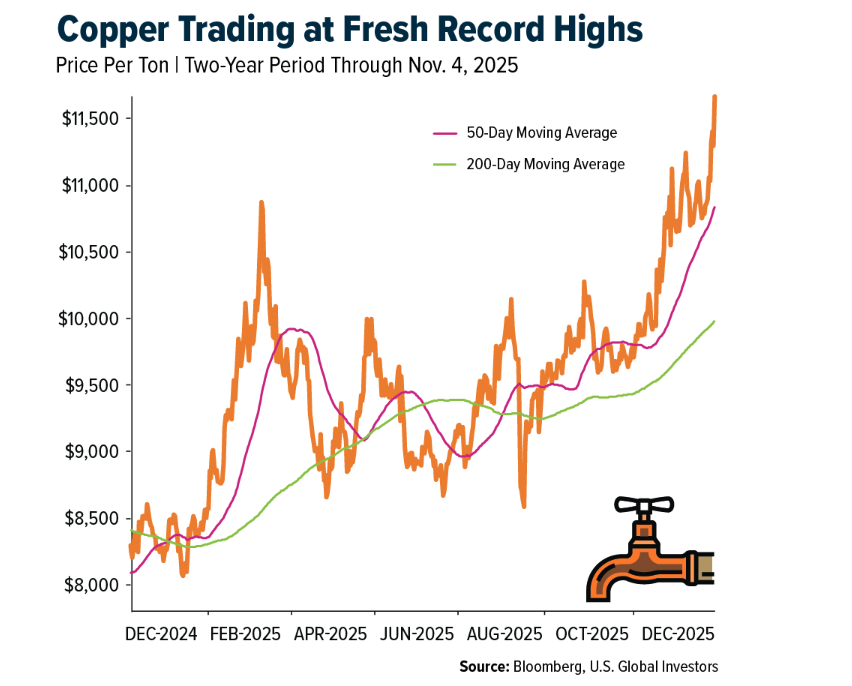

It’s not hard to see why the red metal has been on fire in 2025. Just this week, it hit a fresh record high, surging past $11,705 per metric ton on the London Metal Exchange (LME), an increase of 32% from the start of the year. (And if you think that’s impressive, consider that gold, silver and copper are all reaching new all-time highs together for the first time in 45 years.)

Investment banks are bullish. JPMorgan expects copper to reach $12,500 per ton in the second quarter of 2026, averaging around $12,075 for the full year. UBS is even more optimistic, projecting $13,000 by the end of next year.

Why Rising Copper Prices Won’t Slow AI Buildout

Data centers currently consume about 1.5% of global electricity supply, roughly the same amount as the entire U.K., according to the International Energy Agency (IEA). The organization believes that, by 2030, demand will more than double, with AI responsible for much of the increase. That means data centers could be consuming more than half a million metric tons of copper annually by the end of the decade.

As executive chairman of HIVE Digital Technologies, I’ve watched this transformation firsthand. The infrastructure needed to power this new digital economy—whether it’s Bitcoin mining, AI training or cloud computing—is staggering. And it all runs on copper.

But here’s the thing: unlike other sectors where high input costs might take a bite out of demand, data center developers are largely indifferent to copper prices. According to Wood Mackenzie (WoodMac), the metal accounts for less than 0.50% of total project costs, which is little more than a rounding error.

Demand, then, is relatively price-inelastic. Data centers will be built whether copper is trading at $10,000 or $20,000.

A 30% Supply Deficit Could Be Coming by 2035

Here’s where I think investors should pay close attention. While demand is accelerating at a breakneck speed, supply is facing structural constraints that can’t be solved with a simple turn of the spigot.

Analysts are sounding the alarm. At a recent conference on critical minerals, the IEA warned attendees that copper is heading toward a supply deficit that could reach as high as 30% by 2035, making it one of the most vulnerable metals in global supply chains.

WoodMac, meanwhile, expects global copper demand to surge 24% by 2035, reaching nearly 43 million tons per year. To meet that demand, the industry will need 8 million tons of new mining capacity, requiring investment exceeding $210 billion.

To put that into context, total capital investment in copper mining over the past six years was only around $76 billion, WoodMac says.

Solving the Mining Bottleneck

To be clear, we’re nowhere close to running out of copper. The U.S. Geological Survey (USGS) estimates 48 million tons of identified copper resources domestically, more than enough to supply the country for decades.

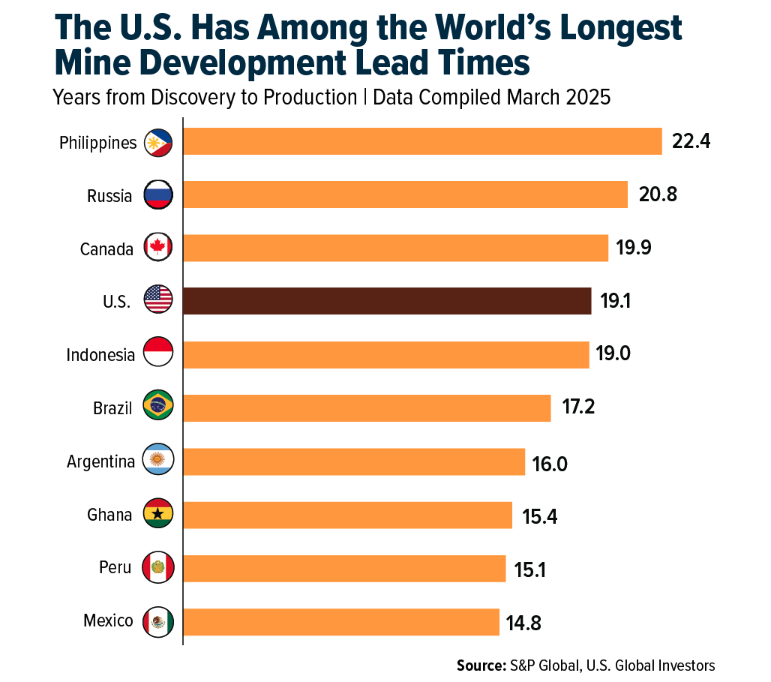

The challenge is converting the raw ore into usable metal at speed and scale. Even if we wanted to rapidly develop new supply, we couldn’t. The time required to bring a new copper mine online in the U.S. averages 19 years. That’s one of the longest in the world.

S&P Global’s research shows that, between 2019 and 2023, only four copper discoveries were made around the globe, amounting to only around 4.2 million tons. Large, high-grade deposits are becoming rarer, and when they’re discovered, getting them into production takes longer than ever.

Consider Arizona’s $10 billion Resolution copper project. Discovered decades ago, it’s now targeting 2030 for production, a 35-year timeline from discovery to first pour.

Every Major Growth Trend Is Copper-Intensive

The fundamentals supporting copper’s ongoing rally are about as solid as I’ve seen in my 40+ years in capital markets. Every major trend driving global growth right now—AI, renewable energy, electric vehicles, grid modernization—is copper-intensive.

When you have multiple banks projecting copper above $12,000 a ton, when the IEA is warning of 30% supply deficits, and when a single AI data center can consumer as much copper as three conventional facilities, it’s time to pay attention.

As I’ve said during previous copper cycles, we may need a telescope to see where prices are headed. This time, with AI adding fuel to an already tight market, that telescope might need to be pointed even higher.

Airlines and Shipping

Strengths

- JetBlue and Delta noted that fourth-quarter demand has remained healthy and that bookings have been trending in line with expectations, except during the FAA emergency order that temporarily reduced flight operations due to the government shutdown, according to Raymond James.

- One China Global Airways notes that e-commerce continues to dominate cargo flows, with major platforms (Amazon, Pinduoduo) shipping aggressively for Black Friday and Christmas, while the removal of the European €150 de minimis rule is unlikely in the near term given strong opposition.

- The Sunday after Thanksgiving set a record as the busiest air-travel day ever for the third year in a row. According to TSA passenger-throughput data, more than 17.7 million passengers were screened this past week (Monday, November 24–Sunday, November 30), which was 2.6% higher than last year’s Thanksgiving travel week, reports Morgan Stanley.

Weaknesses

- Bank of America notes that China–Japan routes have seen 40–45% of passenger bookings canceled after November 15 in the opened booking window. Flight cancellations are tracking at 30–35% in November–December, with most cancellations involving lower-tier cities in China and Japan. Approximately 30–40% of travelers have opted for domestic trips, while 10–15% have shifted to Southeast Asia, another 10–15% to Korea, and around 5% to Russia.

- West Coast port volumes declined 11% in October, as volume decreases reflect tariff pull-forward effects and difficult comparisons given a late ocean peak last year. Ocean rates from Asia to both the East and West Coasts fell sharply during the first three weeks of November, declining 18% and 11%, respectively, according to TD.

- According to J.P. Morgan, Airbus confirmed that a batch of fuselage panels contained flaws. The panels are located at the front of the aircraft, positioned behind the cockpit and alongside the two front doors.

Opportunities

- Wizz considers itself a “genuine first mover in the Ukrainian market.” In line with EASA’s guidance from February, Wizz plans to restart 30 inbound routes to Ukraine within six weeks of any ceasefire, according to Bank of America.

- Israeli business daily Globes reported that Hapag-Lloyd has submitted a bid for ZIM. According to the same article, MSC and Maersk have also expressed interest.

- According to Bank of America, new aircraft deliveries are expected to return to “normal” starting in 2026, with deliveries reaching +8% of the fleet in 2026 and another +9% in 2027. GTF engine issues are expected to persist through 2025 but could begin to improve in 2026–27, supporting narrowbody supply.

Threats

- According to RBC, Airbus indicated that 85% of the impacted aircraft (5,100 aircraft) will require only a simple software fix. However, 900 older A320 aircraft will need a hardware replacement to accommodate the software upgrade. The timing of their return to service remains uncertain. If these aircraft are grounded for an average of one month while the ELAC systems are replaced, the disruption could result in a EUR 300 million earnings impact from compensation to airlines.

- The return of traffic through the Red Sea appears imminent. Maersk is assessing a potential return but has not provided a specific timeline, while ZIM stated it is “waiting for the insurance company to approve our return into the Red Sea.” Maersk has since added that any resumption will depend on the security situation. Reopening could further exacerbate declines in ocean rates in 2026, as it would add 7% to effective capacity, according to Bank of America.

- According to JP Morgan, Airbus has lowered its 2025 aircraft-delivery guidance to “around 790,” down from “around 820,” due to the unexpected discovery of quality issues in some A320 fuselage panels supplied by a vendor.

Luxury Goods and International Markets

Strengths

- Inditex (ITX), best known for its brand Zara, rallied on Wednesday and reached a record high after delivering quarterly results that exceeded market expectations. The retailer reported solid sales growth, improved profitability, and a strong start to the winter season, with November sales up by double digits.

- Service PMIs in China, the U.S., and Europe all remained above the key 50 level, signaling continued expansion across the global services sector. In China, solid service activity helped offset weakness in manufacturing, supported by improving consumer spending. In the U.S., demand remained resilient in areas such as healthcare, leisure, and business services. Europe also saw service-sector growth hold above the contraction line, driven by steady tourism and professional services activity.

- Cettire, an Australian online luxury fashion marketplace that sells discounted designer apparel and accessories to global customers, was the best-performing stock in the luxury index this week. Shares jumped on renewed investor optimism around improving operations and early signs of stabilizing cash flow, further boosted by strong trading volume from short-term momentum buyers.

Weaknesses

- China’s manufacturing PMIs dipped below the key 50 level, signaling a contraction in factory activity after months of uneven recovery. A reading under 50 indicates shrinking output, weaker demand, and ongoing pressure on industrial momentum. The decline highlights lingering challenges in China’s manufacturing sector, including soft export orders and cautious domestic spending, and raises concerns about the strength and sustainability of the country’s broader economic rebound.

- U.S. private payrolls posted their biggest drop in more than two and a half years in November as small businesses shed jobs. Private employment decreased by 32,000 last month, the largest decline since March 2023, after an upwardly revised increase of 47,000 in October, according to the ADP report.

- Signet Jewelers was the worst-performing stock in the S&P Global Luxury Index this week, as its shares fell despite beating earnings expectations. Investors reacted negatively to the company’s cautious outlook for the crucial holiday shopping season, raising concerns about softer consumer demand. Additional selling pressure from large investors trimming positions pushed the stock lower despite otherwise solid results.

Opportunities

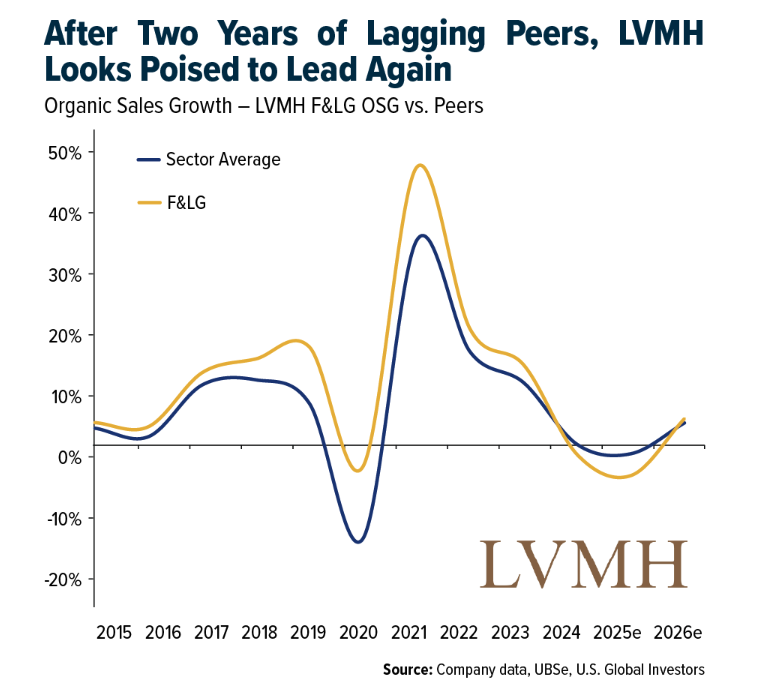

- After remaining cautious on LVMH for the past two years, UBS has upgraded the stock to Buy, citing the first signs of a recovery in EPS momentum. The Fashion and Leather Goods segment, the company’s largest division and a notable underperformer over the past two years, is now positioned for a rebound.

- Prada’s move to finalize the purchase of Versace represents a major strategic opportunity for the group. By bringing Versace under its umbrella, Prada gains access to one of the most globally recognized luxury fashion houses, strengthening its position in high-end apparel and accessories. The acquisition broadens Prada’s brand portfolio, adds a powerful growth engine in the U.S. and Asia, and creates meaningful potential for scale benefits across design, production, and retail.

- European carmakers could benefit from the U.S. rolling back strict fuel-efficiency rules, as it would reduce regulatory pressure and compliance costs for all automakers selling in America. With fewer penalties tied to efficiency targets, European brands such as BMW, Mercedes-Benz, and Volkswagen would have greater flexibility in their U.S. lineups and could focus more on higher-margin SUVs and performance vehicles, boosting profitability.

Threats

- Signet Jewelers’ shares fell despite reporting an earnings beat, reflecting investor concerns about the company’s near-term outlook. While profitability exceeded expectations, management offered a cautious forecast for the rest of the year, citing softer discretionary spending and ongoing volatility in the jewelry market. The gap between strong results and a guarded outlook weighed on sentiment, signaling that investors remain focused on the potential for slowing sales and margin pressure ahead.

- This week, workers at Moët Hennessy, the wine and spirits arm of LVMH, went on strike across major brands including Hennessy and Veuve Clicquot, protesting the cancellation of annual bonuses and demanding fair compensation. This rare move in the luxury sector highlights deep employee dissatisfaction and poses a serious threat to the prestige, output stability, and profit margins of LVMH’s spirits division, potentially undermining consumer confidence and disrupting the high-end drinks market.

- Italian authorities ordered 13 luxury companies to hand over internal documents as part of an investigation into possible labor abuses in their supply chains. This development poses a significant risk to the luxury sector, as it could damage brand reputations, lead to fines or legal action, and increase pressure for stricter oversight of luxury-goods production.

Energy and Natural Resources

Strengths

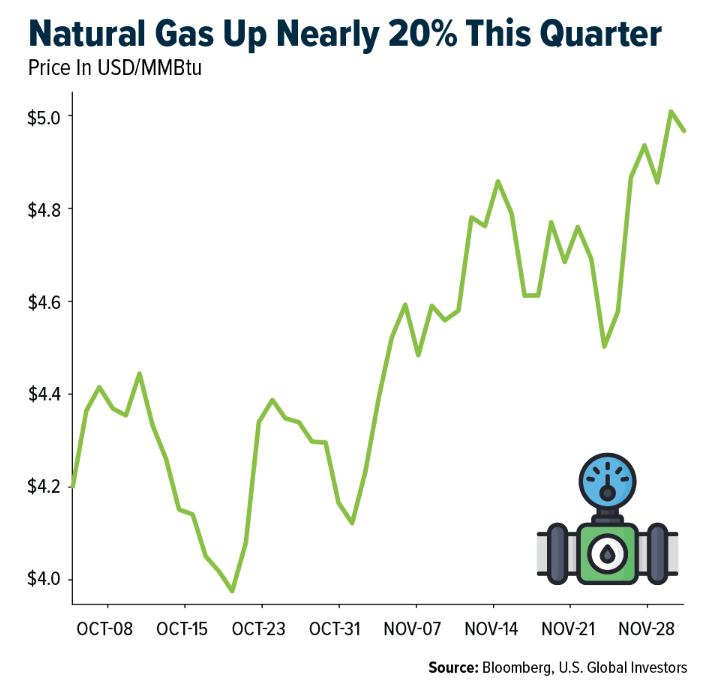

- For the week ending December 5, 2025, natural gas was the top-performing commodity, rising as much as 10%, while copper and crude oil also showed gains. Princeton’s ZERO Lab research highlights that data centers with onsite power, particularly natural gas turbines, can become operational up to five years faster than those waiting for grid connections, offering a key advantage for AI clusters. Meanwhile, Bloomberg reports that shipping rates for crude and LNG have surged up to 467%, underscoring strong global demand and reinforcing natural gas as a critical fuel for power generation and international trade.

- Osisko Metals secured C$32.5 million in strategic capital from top-tier industry players, Hudbay, Agnico Eagle, and Franco-Nevada, demonstrating strong institutional confidence in the long-term potential of the Gaspé Copper project. The placement validates Osisko’s asset base as one of the largest undeveloped copper systems in eastern North America and brings in partners with deep technical, financial, and operational expertise to accelerate development.

- Ivanhoe’s Robert Friedland attending the signing of the Rwanda–DRC Washington Accords highlights how major mining leaders are closely tied to emerging US-backed critical-minerals diplomacy. The deal aims to stabilize one of the world’s most mineral-rich regions, including cobalt, copper, and tin, and signals potential opportunities for Western investment and supply-chain partnerships if the peace framework holds.

Weaknesses

- Lumber was the worst-performing commodity for the week, falling more than 11%. Bloomberg reports that Weyerhaeuser has dropped over 20% this year as new-home construction and renovations slow due to low consumer confidence. Even expected interest-rate cuts next week have not supported lumber prices, and Weyerhaeuser now trades below the value of its timber assets.

- RBC’s 2026 energy outlook highlights sector weaknesses, including an ongoing oil supply glut that limits pricing power and gas assets that appear fairly valued, constraining rerating potential. Heightened geopolitical uncertainty adds downside risk for refining and LNG businesses, reinforcing the need for a selective approach rather than broad-based exposure.

- China’s oil demand outlook remains weak, with Hengli warning that consumption will stay sluggish until at least mid-2026 as economic softness, trade tensions, and rapid EV adoption weigh on crude use. This slowdown from the world’s largest importer threatens broader market demand unless Beijing implements significant policy stimulus.

Opportunities

- Copper’s breakout to fresh record highs, now approaching $12,000 per ton, signals accelerating tightness ahead of a structural deficit, with Citi projecting $13,000 per ton by the second quarter as U.S. stockpiling drains global inventories. This deepening supply imbalance, reinforced by major traders like Mercuria pulling hundreds of millions worth of copper from LME warehouses, creates a powerful multi-year tailwind for producers leveraged to rising copper prices.

- India’s move to expand nuclear cooperation with Russia, potentially adding a second multi-reactor VVER plant, comes as the country accelerates efforts to secure long-term uranium supply, including its recently approved deal allowing Cameco to export Canadian uranium directly into India for the first time in a decade. With India targeting a massive nuclear build-out through 2047, easing liability laws, and seeking diversified fuel chains, global uranium suppliers and nuclear-technology partners are well-positioned to benefit from one of the fastest-growing nuclear markets in the world.

- Tesla securing the largest allocation of advanced energy project tax credits, $240.3 million per Bloomberg Law, underscores a major opportunity as the program accelerates investment in clean-energy manufacturing and critical-materials processing. The 48C credit can cover up to 30% of qualified project costs, giving Tesla a significant cost advantage as it scales next-generation EV and battery production.

Threats

- Rio’s decision to cut costs, sell assets, and scale back lithium represents a clear threat, signaling the company may fall behind peers aggressively expanding into energy-transition metals. By lowering copper production expectations and slowing its only major battery-materials growth avenue, Rio risks ceding long-term strategic ground to competitors positioning for the next commodity cycle.

- Goldman warns that copper’s surge above $11,000 poses a threat to the bull narrative, arguing the rally is driven by expectations rather than fundamentals, with global supply still more than sufficient to meet demand. Their view that no true shortage emerges until 2029 and that prices could be capped between $10,000 and $11,000 in 2026 introduces downside risk for producers priced for a tighter market.

- Trump’s push to accelerate AI data-center buildouts while simultaneously hindering renewable energy development creates a structural threat, risking a slowdown in the power buildout needed to sustain AI growth, tightening supply, and driving electricity prices higher. This policy mismatch could choke off the cheapest, fastest-to-build power sources just as data-center demand triples, undermining U.S. competitiveness in the global AI race.

Bitcoin and Digital Assets

Strengths

- XRP ETFs continue to post record inflows, signaling rising institutional adoption. U.S. spot XRP ETFs have logged 13 straight days of inflows, adding $50.27 million on December 3 and bringing cumulative net inflows to $874 million, on pace to reach $1 billion in under a month. This momentum places XRP ETFs among the fastest-growing digital-asset vehicles and aligns with strong demand for other crypto ETFs, including spot Bitcoin and Ether funds, which have attracted $58 billion and $13 billion, respectively.

- The CFTC’s approval of spot crypto trading on federally regulated U.S. exchanges marks a major step forward for market legitimacy and investor protection. Moving spot Bitcoin and other digital assets onto CFTC-registered venues—long considered the gold standard for market integrity—boosts institutional confidence, enhances transparency, reduces counterparty risk, and shifts activity from offshore platforms to U.S. oversight. It represents one of the strongest structural tailwinds the industry has seen in years.

- Twenty One Capital’s upcoming NYSE debut, backed by Cantor Fitzgerald, Tether, Bitfinex, and SoftBank, underscores accelerating institutional adoption of Bitcoin. With 43,500 BTC (about $4 billion), it will become the third-largest corporate holder, adding scale and credibility to the Bitcoin-treasury landscape. Despite recent volatility, the rise of publicly traded BTC-treasury firms signals sustained demand and expanding institutional market infrastructure.

Weaknesses

- Politically linked crypto firms are experiencing severe volatility and reputational risk. American Bitcoin fell more than 50% within minutes after its lockup expired, adding to steep declines in other Trump-associated projects such as WLFI (-51%) and Alt5 Sigma (-70%). These drawdowns highlight how political ties can magnify market fragility and undermine investor confidence during broader crypto stress.

- Meta’s potential 30% budget cut to Reality Labs—after more than $70 billion in losses—signals a structural slowdown in metaverse adoption. Crypto metaverse tokens have collapsed from over $500 billion to under $3.4 billion in 2025, underscoring weak real-world demand, limited user traction, and narrative fatigue. The contraction reflects the vulnerability of non-Bitcoin digital-asset sectors as institutional focus shifts from Web3 to AI.

- According to CoinMarketCap, among the top 100 crypto assets, the largest seven-day declines came from Aerodrome Finance (AERO) at –19.09%, followed by Canton (CC) at –14.79% and Decred (DCR) at –11.96%.

Opportunities

- JPMorgan sees significant upside for Bitcoin if it is valued similarly to gold. Analyst Nikolaos Panigirtzoglou argues Bitcoin could reach $170,000 under a gold-parity framework, noting that BTC has rebounded 12% from its November lows and is back in positive territory for the year. With production costs near $90,000 providing a soft floor and a favorable MSCI decision possible in January, both Bitcoin and Strategy could benefit from asymmetric upside as futures-market deleveraging winds down.

- The new Base–Solana bridge, secured by Chainlink’s CCIP, enables direct movement of SOL and SPL tokens into Base applications, expanding liquidity and cross-chain activity. This interoperability milestone allows developers to support Solana assets natively while advancing institutional-grade security, accelerating the creation of integrated, always-on digital markets across the crypto ecosystem.

- Drift’s launch of v3 on Solana delivers a major performance improvement—10x faster execution, with 85% of market orders filling in under 0.5 seconds and slippage reduced to about 0.02%. These upgrades make on-chain trading feel comparable to centralized exchanges, lowering friction for both retail and institutional users and positioning Solana to capture broader liquidity in on-chain derivatives.

Threats

- Malaysia has deployed a joint air-and-ground task force, using drones and thermal scanners, to shut down nearly 14,000 illegal Bitcoin-mining rigs that have siphoned $1.1 billion in electricity since 2020. Authorities warn that these operations threaten national infrastructure, highlighting growing scrutiny of mining practices globally. With electricity theft up 300% since 2018 and thousands of sites already dismantled, the crackdown signals rising regulatory and enforcement risks for Bitcoin mining across emerging markets.

- The SEC’s approval of a 2x leveraged SUI ETF, just weeks after the largest leverage-driven wipeout in crypto history, raises systemic-risk concerns across digital assets. Leveraged products amplify volatility and liquidation cascades, which contributed to October’s $19 billion meltdown and Bitcoin’s drop from $126,000 to below $80,000. The decision underscores fears that excessive leverage remains a structural vulnerability in the crypto market.

- The IMF’s call for stronger institutions and coordinated global oversight signals increasing regulatory pressure on stablecoins, which could slow innovation and raise compliance costs. The fund warns that fragmented frameworks and limited blockchain interoperability pose systemic risks, prompting tighter controls that may restrict cross-border liquidity and create uncertainty for digital-asset markets.

Defense and Cybersecurity

Strengths

- Global defense procurement continues to accelerate, with arms sales reaching a record approximately $679 billion among the top 100 manufacturers. This confirms a multi-year upcycle in defense production, strengthening the fundamentals for major primes such as Lockheed Martin, RTX, Rheinmetall, and BAE Systems.

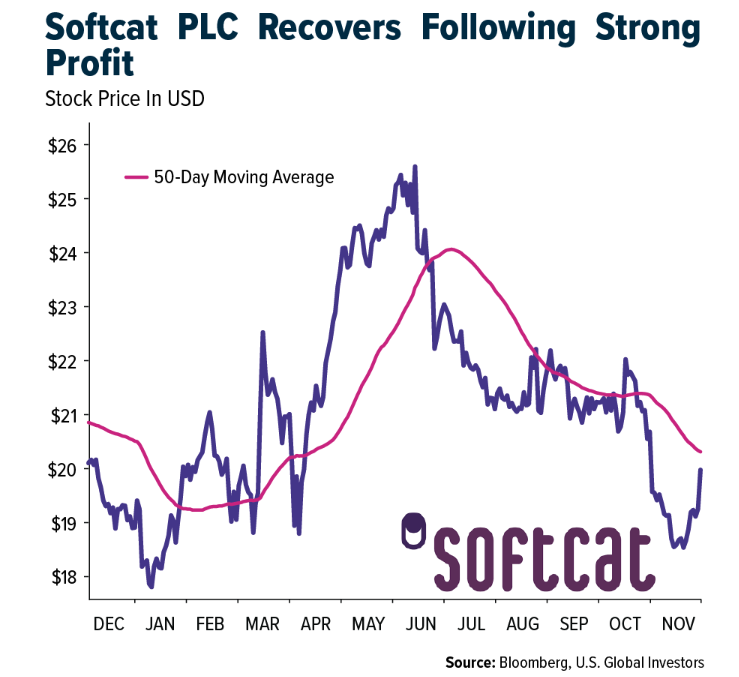

- Softcat reported broad-based, double-digit growth in gross profit and underlying operating profit in its first quarter, with leadership noting that ongoing strategic investments are positioning the company to meet complex customer needs and capture future growth opportunities despite a slight dip in its share price.

- Lockheed Martin is expanding deeper into hypersonic weapons with a new 17,000-sq-ft integration lab in Huntsville, part of a $700 million investment. This positions the company as a central player in one of the Pentagon’s highest-priority modernization domains.

Weaknesses

- Multiple drone crashes during U.S. Air Force testing have raised concerns about Anduril’s ability to translate rapid development into reliable field performance. Public exposure of these failures increases pressure across the autonomous-systems ecosystem and could slow adoption of newer platforms.

- Micron’s exit from the consumer RAM and SSD market underscores the economic weakness of low-margin memory segments. With only Samsung and SK Hynix remaining as major suppliers, industry concentration heightens pricing volatility and reduces competitive pressure.

- Amazon withdrew from the Project Blue data-center initiative in Tucson following strong local opposition over water and power usage. The move highlights the growing political and community resistance to hyperscale infrastructure, which can threaten project timelines and increase regulatory friction for cloud providers across the U.S.

Opportunities

- The new multicloud networking service, launched jointly by Amazon and Google, reduces Azure’s lock-in advantage and supports more open, flexible infrastructure architectures. AI developers and data-center operators gain significant benefits in cost optimization and workload distribution.

- Pratt & Whitney’s $1.6 billion F135 sustainment award, along with RTX’s expanded role as the sole F-35 engine sustainment provider, provides stable, long-term revenue visibility. Service-driven programs like these strengthen the reliability and readiness of U.S. and allied air fleets.

- The rapid rise of alternative AI-compute ecosystems, including Vultr’s $1 billion deployment of 24,000 AMD MI355X GPUs, creates market opportunities for non-NVIDIA vendors. This trend accelerates competitive dynamics, reduces supply-chain dependence, and enables architectural diversification.

Threats

- Telegram’s decentralized AI platform Cocoon introduces a structurally disruptive model that bypasses centralized data centers by using thousands of voluntarily connected GPU devices. If widely adopted, it could exert downward pressure on cloud-compute pricing and challenge AWS and Azure business models.

- The U.S. approval of a $1 billion helicopter support package for Saudi Arabia, along with Riyadh’s renewed push for F-35s, is likely to face heavy congressional scrutiny. Political friction could delay deals, disrupt timelines, and add uncertainty to U.S. defense-export pipelines.

- China’s Cambricon plans to more than triple AI-chip production by 2026, aiming to replace NVIDIA in the domestic market. This intensifies geopolitical competition and threatens NVIDIA’s long-term presence in one of the world’s most strategically significant regions.

Gold Market

This week gold futures closed essentially flat, despite fluctuations during the week. Gold stocks, as measured by the NYSE Arca Gold Miners Index, were off about three-quarters of a percent. The S&P/TSX Venture Index gained the most, up over 80 basis points. The U.S. Trade-Weighted Dollar fell about a half of a percent by the close of the week.

Strengths

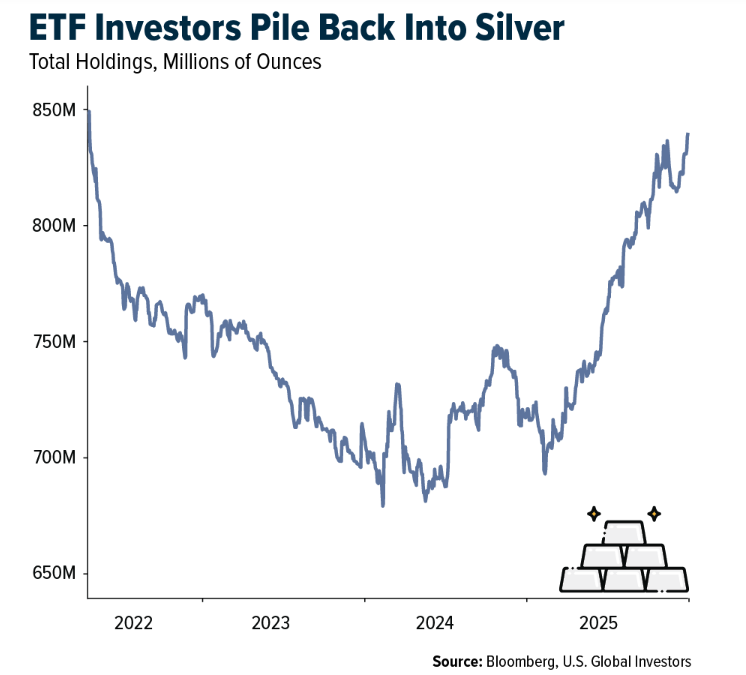

- The best performing precious metal for the week was silver, up about 3.6%. Silver reached a record high on Monday, retreated for three days and set another record on Friday. The metal has gained nearly 22% in the past month, previously hitting $50 an ounce in 1980 and 2011.

- Gold holdings in exchange-traded funds (ETFs) hit 3,932 tons at November’s end, marking six months of growth. This reflects continued investor interest, with gold set for its strongest year since 1979 as investors shift from bonds and currencies to alternative assets.

- Sibanye Stillwater reached a three-year wage agreement with the representative unions at its South African gold operations, with the estimated average three-year basic wage increase for the total bargaining-unit wage bill, including all benefits, at approximately 5.4% per annum, according to a statement.

Weaknesses

- The worst performing precious metal for the week was platinum, down about 1.3%, perhaps on factor activity shrinking in the U.S. by the most in four months as reported this week. The Bank of Thailand intends to enforce more rigorous reporting rules for gold transactions. Officials have noticed that approximately 10% to 20% of these transactions are related to fluctuations in the baht. They plan to further investigate how this impacts the currency’s volatility and consider possible solutions.

- According to UBS, streaming companies have not performed as well as expected despite rising gold prices in 2025. This is because new deals are getting more costly and competitive, and miners are delivering stronger results, which makes the streaming and royalty model less appealing.

- Bank of America notes that, in the past year, gold’s rally has shown a lower correlation with other asset classes than it did throughout the entire post-COVID period. Its connection to Treasuries has also decreased. Additionally, although commodities typically gain when the dollar weakens, this trend has diminished in the current year. For example, crude oil prices have dropped year-to-date, mainly due to decisions by OPEC and geopolitical factors.

Opportunities

- Mithril Silver and Gold Ltd. has secured a Purchase Option for the La Dura gold-silver property near its Copalquin site in Durango, Mexico. La Dura includes several historic mines, notably a four-level gold-silver mine with a 60-tonne-per-day facility and holds extensive mining data from the 1990s to 2018. The mine last operated in 2013. Mithril has an exclusive four-year option to buy 100% of the concessions for US$4 million.

- RBC reports that Barrick has announced its intention to evaluate an initial public offering (IPO) for its North American portfolio assets, including Nevada Gold Mines, Pueblo Viejo and Fourmile. RBC notes that this proposed spin-out could potentially generate significant value for Barrick shareholders, estimating an additional relative upside of 15–20% compared to the company’s current share price.

- Perseus Mining Ltd. has made a bid to acquire Predictive Discovery Ltd., outbidding a Canadian competitor, Robex Resources Inc., for gold assets in Africa. The offer values Predictive at A$2.1 billion ($1.4 billion), with Perseus proposing A$0.778 per share—a 24.5% premium over Predictive Discovery’s Dec. 2 closing price.

Threats

- Caledonia Mining Corp. said a proposal by Zimbabwe’s government to double the royalty on gold producers would curb its profits. “If implemented, it would be expected to result in a lower level of profitability and cash generation relative to current market expectations,” the company said Monday in an emailed statement.

- First Majestic is offering $300 million in unsecured convertible senior notes due 2031, with an option for initial purchasers to buy up to an additional $45 million in notes. The company plans to use proceeds to repurchase a portion of an existing 2027 convertible notes and for general corporate purposes, according to Bloomberg.

- Italy was urged by the European Central Bank to rethink a push to declare its gold reserves the property of its people, a move critics say could open the door to the government selling off bullion. In a legal opinion dated Tuesday, the Governing Council asked Premier Giorgia Meloni’s government to review the proposal following a request from Rome for officials in Frankfurt to study the matter, according to Bloomberg.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2025):

JetBlue Airways

Delta Air Lines

Airbus SE

Wizz Air Holdings Plc

AP Moeller Maersk

Micron Technology Inc.

Osisko

Hudbay Minerals

Agnico Eagle Mines Ltd.

Franco-Nevada Corp.

Ivanhoe Mines Ltd.

Cameco Corp.

Tesla Inc.

Inditex

Signet Jewelers

LVMH

Prada

Sibanye Stillwater

Mithril Silve and Gold

Barrick Mining

Perseus Mining

Calendonia Mining

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting our prospectus page or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Read additional important information. +

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All