Key takeaways

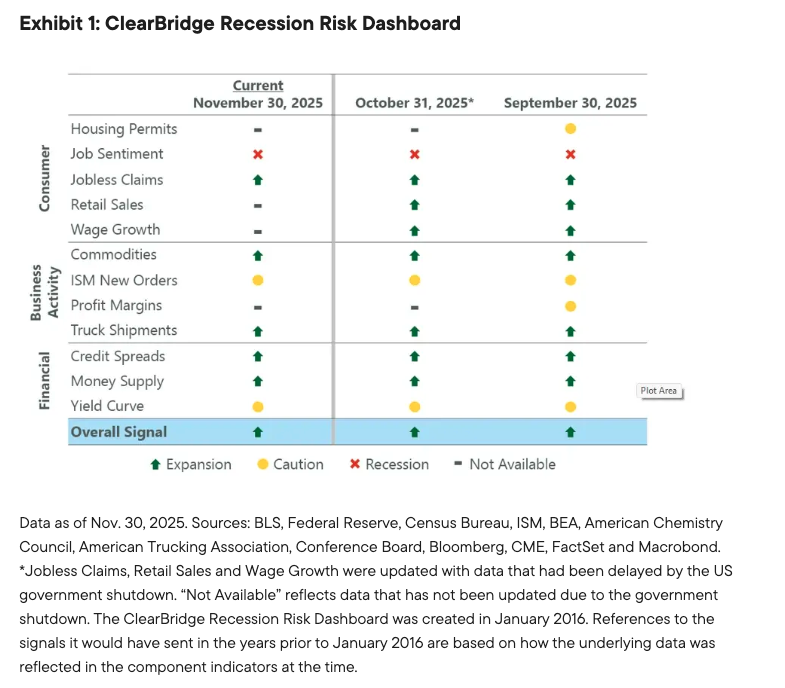

- The ClearBridge Recession Risk Dashboard saw no signal changes this month and alternative data sources for indicators still on pause suggest a continuation of trends consistent with no signal changes; the overall dashboard remains firmly in green expansionary territory.

- While AI is popularly being linked to labor weakness, the latter has been most evident in industries that have the lowest AI adoption rates, suggesting that other dynamics are playing a larger role in slowing the pace of job creation.

- While AI labor fears could lead to higher market volatility, the dual tailwinds of fiscal and monetary policy support should power the US economy and corporate earnings in 2026; we remain firmly in the “buy the dip” camp.

AI less of a labor headwind than believed

The S&P 500 Index saw its first 5% pullback in six months during November, only to recover late in the month and ultimately eke out a +0.2% gain. The benchmark now sits within 1% of its all-time high. This volatility was not entirely unexpected; in recent months, discussion of a market bubble has dominated investor conversations. In our view, the initial November slump appears to have been primarily driven by retail investors de-risking as high-momentum darlings bore the brunt of the selloff. Moving into the new year, we continue to believe that a solid earnings backdrop and upside revisions to EPS estimates should drive markets higher despite the S&P 500 Index trading at a lofty 22.4x forward earnings multiple.

From a fundamental perspective, little appears to have changed in the last month. Although the government shutdown has ended, the flow of government data remains interrupted as various agencies work through backlogs. Since our last update, October data has been released for three of the five missing dashboard indicators—Jobless Claims, Retail Sales and Wage Growth—none of which saw changes from their September readings. However, only Jobless Claims has November data available today, meaning four indicators are still not up to date. Crucially, the rest of the dashboard saw no signal changes this month and alternative data sources suggest a continuation of trends consistent with no individual signal changes. As a result, the overall dashboard signal remains firmly in green expansionary territory (Exhibit 1).

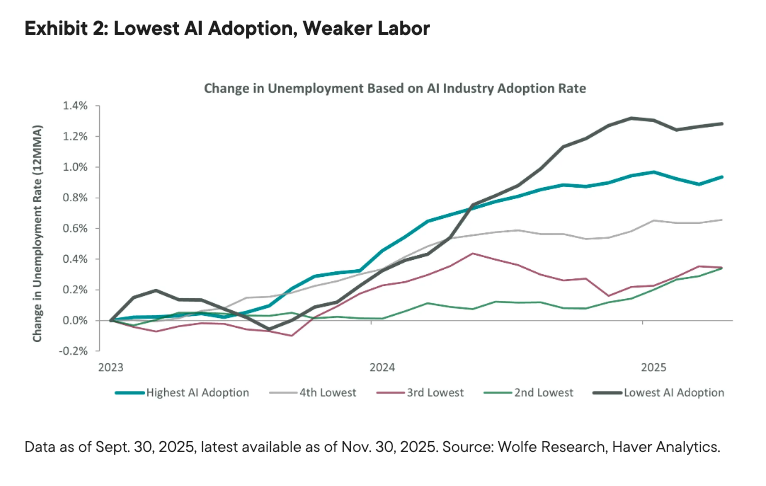

With underlying economic activity and corporate earnings holding up, many investors are left questioning what sparked the mid-November stock market pullback. One fear that has come up frequently when talking with clients is the concern that more widespread adoption of artificial intelligence (AI) is weighing on job creation. The proponents of this narrative point to younger workers, whose more limited experience and narrower skillset in theory allows for easier substitution of capital (AI) for labor. The pickup in the unemployment rate for the youngest Americans (16–24 years old) to 10.4% from a low of 6.6% in April 2023 has helped bolster this storyline.

A deeper review of labor data shows that while AI is impacting the jobs market, its influence is much less than is commonly perceived. Pockets of AI-induced labor market weakness do exist in specific industries such as software development and call centers. However, when evaluating job creation and AI adoption by industry, labor weakness has been most evident in industries with the lowest AI adoption rates (Exhibit 2). This suggests that other dynamics—changes in immigration and trade policy, the continued aging of the US population and DOGE-related efforts to shrink the Federal workforce—are playing a larger role than AI in slowing the pace of job creation.

Although AI may not be the leading cause of softer job creation so far, many investors fear the potential for larger AI-induced job cuts in the years to come. While this is certainly possible, job losses stemming from technological progress are typically a feature, not a bug, of the US economy. In fact, this year’s Nobel Prize in Economics was awarded for research into the concept of creative destruction: the process where new innovations replace and make obsolete older ones and how this can drive sustained growth through technological progress. This dynamic is always playing out in the US economy, just to a greater or lesser degree depending on the business cycle.

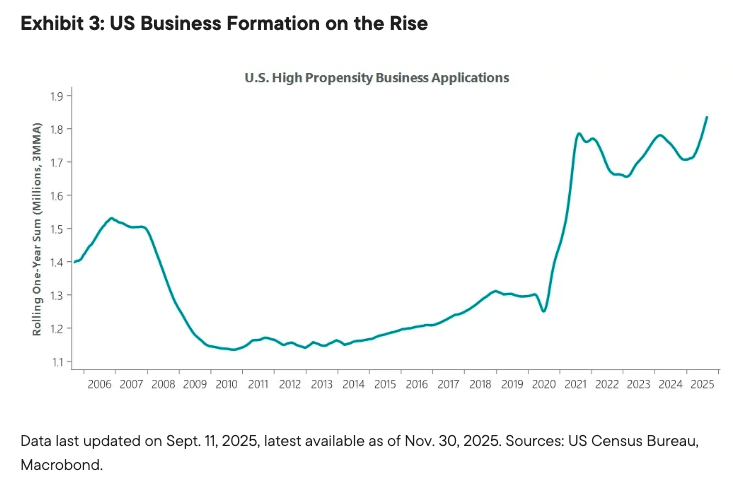

While this time could be different—AI could be more disruptive than past technological innovations—we believe the evidence thus far points to more fear than fact. Further, job losses from AI are only half the story: the creative destruction process also entails job creation as new businesses and whole industries sprout from the seeds of technological progress. The surge in business formation over the past few years (2025 in particular) suggests that some of tomorrow’s leading corporations may already be in their infancy today (Exhibit 3).

Ultimately, the timing and magnitude of disruption will determine how troublesome AI becomes to the economy. Corporate boards will certainly welcome the prospect of efficiency gains and higher profits, and how quickly new businesses can scale their AI adoption will be key in how seamlessly workers transition to new roles and workflows.

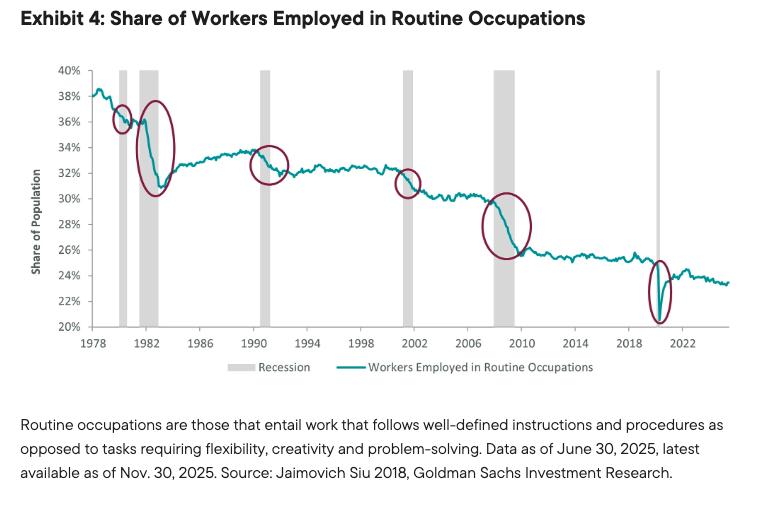

However, this pattern has played out with past technological shifts dating back to the steam engine, and history shows that most job losses in areas impacted by technological developments occur during recessions, not expansions. In times of economic strength, there tends to be more of a slow bleed in routine jobs where technology can more easily substitute for workers. The big shifts have come during broader bouts of economic weakness when harder choices must be made, resulting in more pronounced layoff cycles. The “jobless recovery” of the early/mid 2000s following the tech bubble could be a good parallel for what lies ahead when the current economic cycle eventually culminates (Exhibit 4).

Importantly, with the ClearBridge Recession Risk Dashboard continuing to signal expansion in the year ahead, this scenario is not a pressing concern, in our view. Given economic strength and scant evidence of AI driving widespread job losses, we believe that fears of substantial further downside to labor from AI are currently misplaced. While AI labor fears could lead to higher market volatility, the dual tailwinds of fiscal and monetary policy support should power the US economy and corporate earnings in 2026. As a result, we remain firmly in the “buy the dip” camp.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Equity securities are subject to price fluctuation and possible loss of principal. Large-capitalization companies may fall out of favor with investors based on market and economic conditions. Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

US Treasuries are direct debt obligations issued and backed by the “full faith and credit” of the US government. The US government guarantees the principal and interest payments on US Treasuries when the securities are held to maturity. Unlike US Treasuries, debt securities issued by the federal agencies and instrumentalities and related investments may or may not be backed by the full faith and credit of the US government. Even when the US government guarantees principal and interest payments on securities, this guarantee does not apply to losses resulting from declines in the market value of these securities.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

© ClearBridge Investments

Read more commentaries by ClearBridge Investments